The United States is becoming an even greater melting pot than ever before.

The inflow of diverse racial and ethnic groups combined with the recent home-buying boom has changed the demographic composition of neighborhoods across the country. Executives should now consider how they will develop relationships with their new neighbors.

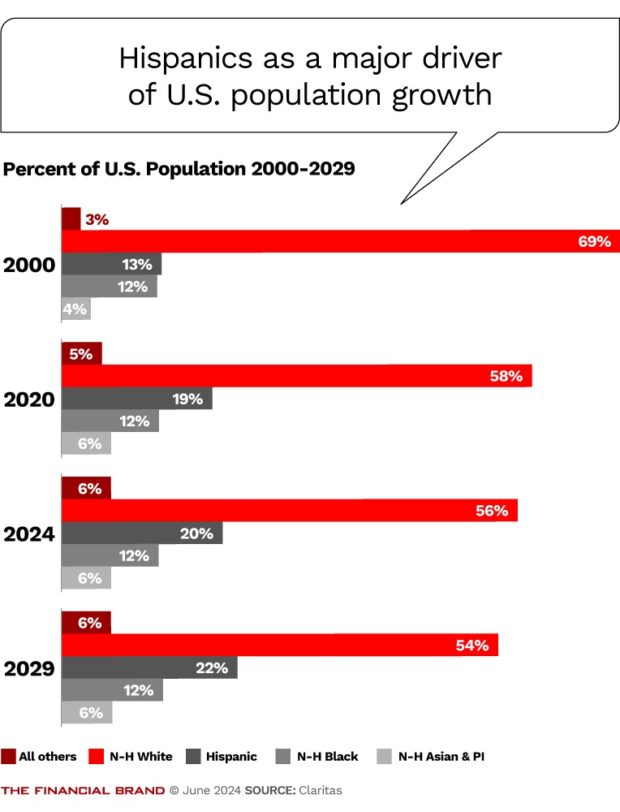

Who are these new diverse segments? According to a report from Claritas, the mainstay is Hispanic immigrants from Mexico, Cuba, Puerto Rico, and other Spanish-speaking countries. They now contribute 67 million to the U.S. population, up from 35 million in 2000. And they’re only one piece of the growing diversification of the United States. Asians, as well as millions from other nations around the world, now pursue the American dream in a new home near banking branches.

Attracting these new audiences can be as simple as providing them options and information in their native language, especially when other institutions are not. That language arbitrage may be the largest competitive branding opportunity of this decade.

The Demographic Melting (and Mixing) Pot

Before the pandemic, the U.S. population spoke more than 350 languages. Aside from English, Spanish has been the primary (if not the only) focus for banks and credit unions because Spanish speakers comprise 20% of the U.S. population.

Today, nearly a quarter (23%) of Millennials are Hispanic, and about 58% of the U.S. population growth over the next five years also will come from the Hispanic segment. By 2029, Claritas analysis forecasts the Hispanic population will grow (by 10%) to 74 million.

“The growth rate of the U.S. Hispanic population [is so significant] that in the time it takes the average person to read this report, over 150 Hispanics have joined the U.S. population,” says Ron Cohen, senior vice president at Claritas. “All the growth now and into the foreseeable future will emanate from multicultural race or ethnic groups.”

Other racial groups have also grown significantly since 2000 and will add millions more this decade. The Asian population has doubled, reaching 20 million, and will reach 22 million by 2029. According to data published by Claritas, the number of people who are not Asian, Hispanic, or White will nearly triple to over 21 million by 2029, from 7.5 million in 2000.

The melting pot became a tossed salad when Americans began moving in 2020. Data suggests that more than 23 million Americans (nearly 7% of the U.S. population) have changed their state of residence since the pandemic. Many more people did not move out of state but changed county, city, or neighborhood – 27 million in 2021, 28.2 million in 2022, and 25.6 million in 2023.

Whether new to the country, recently moved or just building their life, when these consumers are looking for a place to bank, language arbitrage could put institutions on a fast track to stand out.

Read more:

- Bridging Generational Gaps: How Banks Can Tackle Communication Challenges

- To Fight Waning Consumer Loyalty, Here’s How Marketers Can Shift Focus

- How to Define the Generations: The Ultimate Guide for Marketers

Winning Top of Memory Among Non-English Customers

Speaking to someone in their home language is a nice touch for a financial brand. Language, however, has another more influential role in banking: Helping people understand financial decisions.

A significant challenge for many consumers — native-English speakers or not — is not feeling as though they understand finance. Yet, making good financial requires comprehension, especially for when their consequences can reach years into the future. Providing people with information on financial decisions in their native language becomes a compelling way to ensure they understand and make good decisions faster. That experience translates to their first impression and can instill trust.

There is no better play for a brand than occupying a primary spot in consumers’ memory, Don Carli, senior analyst at Branding Business, tells The Financial Brand. “Without it, you have to try to inject yourself into consideration with performance marketing – that means ramp up the ad spending.”

The challenge is to connect the brand with demand in an institution’s addressable market. “Even if a credit union has 300,000 individuals that, in terms of demographically, psychographics, investable assets and income, they are ideal customers, how many are in the market at any given time?” Carli asks.

If a consumer has moved or just started a business, they receive direct mail with offers to open an account. They “don’t tend to open them; they go in the trash or get piled somewhere until there’s a trigger event that puts them in the market,” Carli says. “Then, when they are in the market, they will search their memory before they go to online search, sift through that stack of mailers, or even ask friends for a referral. The top two or three brands in consumers’ memory receive about 80% of the decisions.”

Data is becoming essential to winning top-of-mind consideration through language and cultural preference. “There needs to be that ‘they get me element,'” Carli says. “It needs to be ‘that credit union not only speaks my language, but they also speak it correctly. They know that I’m Dominican and not Venezuelan. They know that I’m acculturated and not first-generation. They know that I own a home and that I’m proud to be the first in my family to own a home.’ That’s the goal of generating brand affinity.”

When branding is the best way for institutions to earn first consideration, how can they deliver personalization correctly – in line with language and culture – and instill brand affinity before consumers are in the market?

Data as a Compass to Deliver Brand to Demand

Take Florida as an example. On the surface, there should be a lot of banking growth in those markets. There are many empty nesters with disposable incomes in their retirement years, and housing can be relatively cheap.

“Institutions can be searching for growth in markets like Florida, though,” Jeff Stevens, senior vice president of strategic partnerships at Claritas, tells The Financial Brand. “Even though the market seems opportune, and the community can be vibrant and growing, deposit growth can be flat, and loan growth can be slow.”

Then, data will reveal new people missed by the institution’s messaging who are therefore not influenced by its brand. “In some areas, data can show 80% of the population is now Hispanic, and 30% prefer the Spanish language. They can be highly unacculturated and need a more tailored engagement approach,” Stevens says.

Florida, though, is an obvious candidate for Hispanic population growth. What about the rest of the country? “There are parts of the country growing rapidly in their multicultural populations, areas executives might not necessarily think would have so many new cultural or linguistic segments,” Stevens says. “Once they have the data to superimpose on their market, such as where their branches are, which areas near branches have the greatest opportunity, and which ones don’t, it becomes a compass for allocating resources and choosing which segments to engage.”

Language is becoming a hot-button issue. “Yes, institutions have benchmarked how they serve the populations in their community for a long time,” Stevens observes. “Now it’s becoming a compelling way to grow.”