Years ago in a TV commercial for Wittnauer fine watches, a young woman approaches a jewelry counter and says, “I want a Wittnauer.” A dimwitted sales rep insists on showing her other items. She continues murmuring, “I want a Wittnauer.” He doesn’t catch on. Finally she shouts her request: “I want a Wittnauer!” Finally it sinks in, and the sales rep gets the sale… despite doing everything possible to undermine the experience by ignoring even the most obvious buying cues.

Are financial institutions listening any better to the voice of the consumer? Not really.

In a BAI webinar, “Trends In Marketing & Customer Acquisition,” serious questions were raised about banking providers’ ability to give consumers what they want, how they want it, when they want it.

Understanding (and Addressing) Consumers’ Pain Points

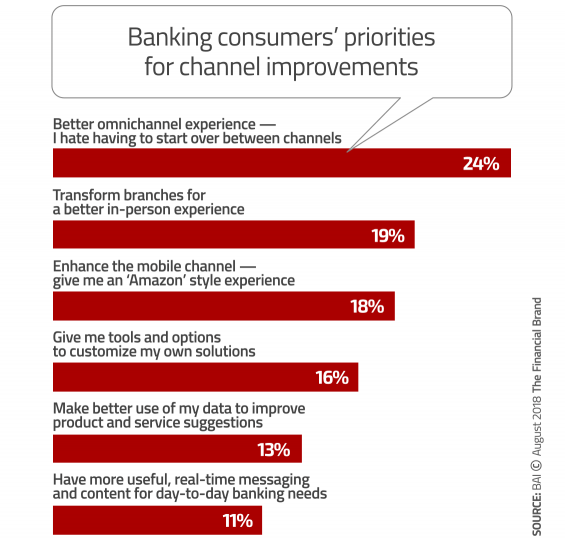

BAI research among financial institutions conducted concurrently with a separate consumer study revealed a major misalignment between the two groups. When asked how their primary financial institution could improve their customer experience, consumers most often requested a better omnichannel experience.

“They’re saying, ‘Remember who I am, and make my experience more seamless’,” explains Byron Marshall, Director/Research at BAI.

But when BAI asked banking executives what their priorities for improving their retail banking results are, a stunning gap emerged. Not one said that “improving the omnichannel experience” was on their radar. Neither was “personalization/customization” or “improving marketing data analytics.”

Banking executives’ instead are placing greater importance on cross-selling and brand awareness. Nearly half (44%) said that “new customer acquisition and onboarding” was their top priority, followed by “increasing brand equity and awareness” (32%), and “deepening relationships with existing customers” (21%). A mere 3% felt that “using data to make more relevant offers” was important.

This suggests that many institutions have been completely ignoring the major pain point for consumers: Making omnichannel work so they don’t have to repeat steps and give information each time they switch channels. Anyone who has called a credit card company and had to input their yard-long account number multiple times ought to get that.

Why the big disconnect? One reason may be that only one in ten banking providers map out their various “customer journeys,” tracing how someone’s interest eventually becomes a new account, loan or other financial product/service. Just as important, financial marketers need to understand why, when and where people decide against doing business with you.

Read More: Why The Customer Journey In Banking Will Never Be ‘Digital Only’

Consumers Prefer Certain Channels for Communications

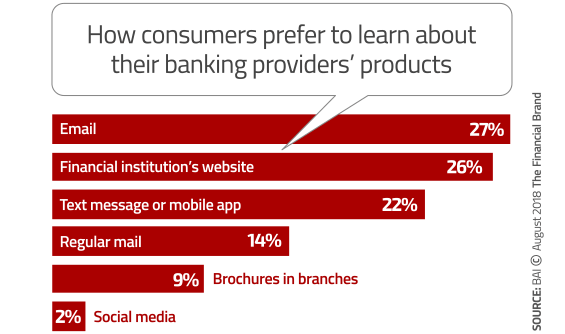

Consumers were asked to indicate how they most preferred to learn about their banking providers’ products and services. Email is their first choice, social media their least favorite option. Surprisingly, text messages and/or mobile app alerts scored highly. One out of seven consumers still like good old fashioned snail mail.

What’s particularly noteworthy about the lack of interest in social media communications is that Millennials were heavily represented in BAI’s study. This strongly reinforces the idea that social media the wrong channel for financial brands to explicitly sell or promote its services. Some financial institutions are almost certainly investing a disproportionate amount of money on social media and allocating more time and resources to it than BAI’s research suggests is appropriate.

BAI’s study also revealed that traditional media — print, outdoor advertising, TV, and radio — are receiving a falling portion of the marketing budget. Money is clearly shifting to digital channels, including online advertising, paid search, social media, email marketing, marketing technologies, and content marketing.

“Marketers are going to have to beef up the digital talent they have.”

— Mark Riddle, BAI

“Marketers are going to have to beef up the digital talent they have,” said Mark Riddle, Director/Research and Content Delivery at BAI.

But the likelihood that financial institutions take this advice seems low, considering the lukewarm attitude banking executives have towards marketing:

- “Senior management is totally committed to superior marketing as a competitive differentiator.” (44%)

- “Senior management is convinced of the ROI for state-of-the-art marketing.” (43%)

- “The role and influence of marketing at senior levels at the bank has increased in the past 1-24 months.”(41%)

- “Marketing is expected to drive tangible ROI for the organization.”(33%)

- “We have effective internal social branding and marketing skills and capabilities.”(28%)

Are You Handling Digital Transformation Intelligently?

Clearly, more banking transactions will move to digital channels; there is little debate about that. However, there is a disconnect between what banking executives believe and consumers say.

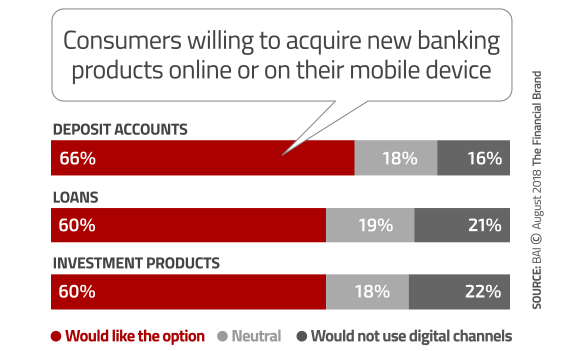

Online account opening provides a clear example. Only a quarter (26%) of banking professionals believe “most accounts will be opened online in ten years”. Consumers aren’t willing to wait that long. They want the ability to acquire any financial product or service digitally now… today.

BAI also asked consumers to rank the “easiness score” for initiating 13 types of relationships, from savings accounts and retirement accounts to home equity lines and mutual funds. On a scale of 1 to 10, with 10 being easiest, not one product scored over 6.5.

The split between those institutions that permit people to open their first account digitally and those that don’t is about even. BAI researchers said that those financial institutions that don’t currently provide digital account opening need to reconsider their position… and fast.

Read More: Even The Best Banks Have Room to Improve Digital Experiences

Leveraging the ‘Main Bank Advantage’

In an annual banking study, three quarters of the 70,000+ consumers surveyed said they were highly satisfied with their primary financial institution. The figure for credit unions specifically was 96% compared to 80% for the top three national banks.

BAI found that the “main bank” used most by consumers shook out this way:

- 58% – Large national bank

- 21% – Regional bank

- 11% – Credit union

- 8% – Smaller local bank

- 11% – Other

BAI says being the “main bank” provides a considerable “home team advantage.” About half of consumers surveyed opened an additional new account at their primary financial institution over the last year, including 78% who opened a new checking account.

The vast majority of Millennials and younger consumers open CDs at their “main bank.” By contrast, Baby Boomers and other older customers are much more likely to go elsewhere; only 36% open CDs at their primary financial institution.

However, the research shows that while there is still inertia in providers’ favor, and that customers clearly concentrate new deposits at their main bank, “no account is really safe” Marshall says because digital tools make it extremely easy for consumers to shop around. One in three consumers surveyed, for example, hit Google searching for specific account features.

Being someone’s “main bank” often gives a bank or credit union a leg up for mortgages, home equity credit, and credit cards, according to BAI’s research. But for auto loans and other types of consumer credit, competitors can more easily snap up business from competitors.

Winning the War of Attrition

Many financial institutions dream of very broad relationships with consumers. However, Marshall said that “most people feel that spreading their business around multiple institutions is fine. They see no particular incentive to consolidate.”

“Most people feel that spreading their business around multiple institutions is fine. They see no particular incentive to consolidate.”

—Byron Marshall, BAI

About a third of consumers have deposit relationships with three or more banks or credit unions, for example.

BAI’s survey found that about a quarter of new account openers said they expect to switch their main banking relationship over the next two years. Why would they choose to leave? BAI asked them to give their two top reasons for moving to another main institution. Ranked from high to low, they are:

- Convenient branch network (35%)

- Cash incentives and rewards (32%)

- Best products and rates (30%)

- Large ATM network (22%)

- Superior customer experience (22%)

- Positive reputation (21%)

- Lowest fees (17%)

- Superior digital capabilities (13%)

- Recommendation from friend or family (7%)

BAI’s study is yet another in the endless chain of research projects proving that branches continue to be one of the most critical — if not the most important — factor driving consumers’ decisions about which banking provider they use.