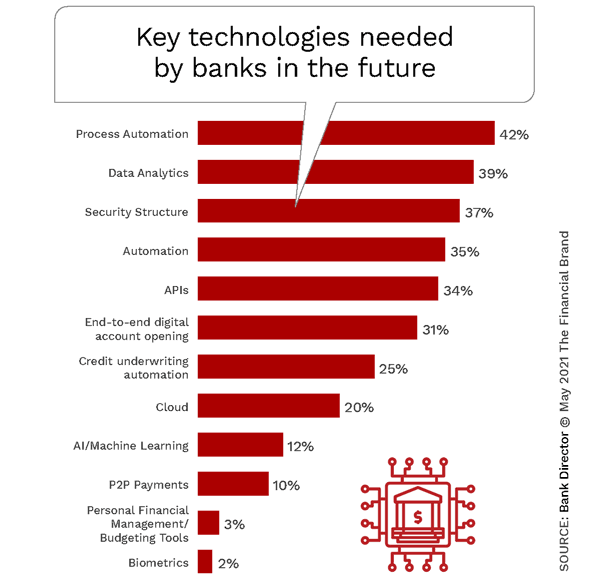

The pandemic highlighted the need for digital banking transformation more than ever, as transactions moved out of branches, work was conducted remotely, and customers expected increasingly personalized experiences. In the past, financial institutions were able to gain a competitive advantage with broader distribution footprints and better pricing. Today, leading banks and credit unions differentiate by leveraging data, artificial intelligence (AI), applied analytics, and the power of cloud computing to innovate and deliver personalized engagements in real time.

This more intelligent way of applying technology allows financial institutions to learn and react to changes in the marketplace or in the behavior of customers in a manner that can benefit both the financial organization and the customer. Combined with the potential of Fifth Generation (5G) cellular, the result is an enhanced customer experience that provides a competitive advantage far greater than geographic location, transforming the financial services industry.

Intelligent banking organizations will need to be built with cloud-computing infrastructures that allow for the combination of data assets and the use of AI algorithms to deliver better quality, improved efficiency, seamless delivery of services, proactive recommendations and enhanced risk mitigation. While most organizations will begin with internal data, the real power will be the integration of external data and insights, including those from open banking APIs.

In addition to increasing efficiency and improving decision making, using AI and applied analytics in combination with advanced technologies will enable current staff to assume higher level roles within the organization. By humanizing digital banking transformation, banks and credit unions will be able to develop the digital expertise across the organization, thereby accelerating employee transformation.

Data is the Foundation of Intelligent Digital Transformation

The ability to collect and analyze both internal and external data to gain real time insights is at the core of most digital banking transformation efforts. Insights derived from big data analytics can be used to improve decision making, increase efficiency, enhance experiences and mitigate risks. Beyond simply using data and insights for reporting and process improvement, the real power is when entire business models are changed and opportunities for both the organization and the customer can be delivered proactively.

As the number of mobile devices, transactions and interactions increase, so does the amount of data they generate. This can either enable more powerful decision making or overwhelm organizations. While many believe more data is better, it must be remembered that data, on its own, is useless without a well thought out plan for how the data will be ultimately used. For most organizations, that means that it may be best to start with data readily available and to improve the use of this data first for improved processes, decision making and personalization.

Managing the collection and use of data requires a strong data governance program, quality data and an understanding of both the owners and users of the data. Without confidence across the organization around the quality of the data being used, any digital banking transformation process is at risk. Investing time and effort up-front around data governance, advanced analytics and machine learning will have a significant pay-off, including increased efficiency, improved customer experiences and greater revenues.

Applying AI to Digital Banking Transformation

Until recently, AI was used primarily for risk mitigation and fraud detection by financial institutions. From a marketing or customer experience enhancement perspective, AI was in the discovery stage, at best, at most banks and credit unions. In both traditional and new applications of AI and machine learning, analysts were trying to determine how these tools could be used to recognize patterns and make predictions.

For many organizations, we are entering the implementation phase with advanced analytics, applying the findings from analysis towards improved operations and enhanced customer experiences. According to Salesforce, 52% of consumers and 65% of business buyers are likely to switch brands if a business doesn’t understand their needs and personalize their communications accordingly. Customers also do not want to provide information that is already available within an organization or have to repeat themselves when transferred across an organization.

There is still a challenge using data for improved results. According to Forrester, the biggest challenge faced by 53% of respondents is in gathering and integrating big data, while 52% struggle to build a predictive analytics platform. Both challenges are linked to the lack of data strategy. This data strategy needs to focus on scaling insights to generate results in areas where there are the biggest gaps, and where there is data readily available to deploy against these opportunities.

Read More:

- Internal Data Unlocks Improved Consumer Banking Experiences

- Already Drowning in Data, Financial Marketers Ask for More

Importance of Cloud Technology for Banking Transformation

According to IBM, the majority of financial services organizations have yet to deploy core systems to the cloud. The reasons include the perceived amount of complexity and concerns over security, risk, governance and control. In fact, while 91% of financial institutions are actively using cloud services today or plan to in the next nine months, on average only 9% of their mission-critical regulated banking workloads have shifted to a public cloud environment. In other words, while banks and credit unions of all sizes recognize the need to transition to the cloud, a majority haven’t started this process.

One of the primary reasons for leveraging cloud computing is the ability to facilitate the use of big data analytics. With the increasing amount of both structured and unstructured data available to banks and credit unions, cloud technology allows organizations to harness the benefit of applied analytics faster than ever before. For instance, a financial institution can extract insights from transaction patterns to target recommendations that improve the financial outcomes for customers.

With a hybrid cloud environment, organizations can mix both public and private cloud resources allowing the flexibility of selecting the optimal cloud configuration for a specific application or workload. There is also the ability to move between the two clouds for research and development, product or operational testing, data back-up, or additional cloud capacity.

5G Changes Everything for Banking Transformation

The majority of daily banking transactions are now being processed on a mobile device – from checking balances, to transferring funds, to making payments. Each of these engagements need to be handled as quickly and simply as possible. And each engagement creates insight for future interactions.

5G technology will not only make all interactions faster, but it will also enable faster identification of engagement opportunities and the more seamless deployment of solutions by processing higher volumes of data with minimal delay. This puts the pressure on traditional financial institutions who must keep pace with fintech and big tech firms that are already leveraging cloud computing and are prepared for the upcoming 5G revolution.

Despite many improvements to the digital banking experience made by financial institutions during the pandemic, many mobile banking applications still do not result in good digital experiences, due to slowness of response, friction and the inability to leverage biometric identification. With 5G, financial institutions will have the opportunity to leverage the speed and data capacity of the new networks to deliver better experiences.

Finally, 5G provides the foundation to improve fraud prevention in real time. According to ComputerWeekly, “Processing data, verifying the nature of transactions, confirming transaction amounts and funds availability, consulting multiple data instances in real time, coupled with customer geolocation and merchant ID, will reduce fraud detection errors and false positives, thereby protecting consumers and the bank’s bottom line.”