Paze is going to take longer than expected to launch.

The ecommerce-only digital wallet — backed by the same big bank consortium responsible for Zelle — was expected to be widely available this fall, in time for the 2023 holiday shopping season. Officials say the launch is coming, just later than initially announced.

Paze first came on the payment industry’s radar in January 2023. By spring, the Early Warning Services consortium had laid out an ambitious schedule. While doing the technical work required to make the wallet operate, it also set out to line up the critical tripod of payments: merchant acceptance, consumer interest and willingness, and the participation of banks and credit unions across the country.

James Anderson, managing director at Early Warning Services and the top official for Paze, says the company decided to adjust its original plan as it brought its concept to the merchant and card issuer markets.

“We decided on more of a phased ramp-up,” says Anderson in an exclusive interview with The Financial Brand. The intent is “to get a little experience testing the system at scale” and build a more substantial merchant footprint.

“That feels like a more prudent approach than the original plan. So that’s where we’ve landed,” he adds.

Now, the national launch is expected to occur over the course of the first quarter 2024.

Phase One Will Be Testing Paze with Select Merchants

Between now and the national launch some merchants will become Paze “early adopters.” The first, announced in early September, is Omaha Steaks. The news release about it articulates one of the key selling points of Paze: “Say goodbye to cumbersome manual entries and hello to a seamless journey where 16-digit card numbers and additional usernames and passwords are a thing of the past.”

Anderson says a test with just the employees of one of the banks in the consortium is coming. This will be followed by a test making Paze available to all eligible consumers in a single state.

The absence of publicly visible pilots had prompted a lot of speculation about what might be happening with Paze, and many in banking and payments will be watching to see if the launch happens in the first quarter as planned.

By Anderson’s account, there’s been a lot of behind-the-scenes activity. “We’ve been, not in the market, but working on it,” he says.

Asked what Paze would be doing in a year — by September 2024 — Anderson says that “we’ll be live and we’ll be going into the holiday shopping season at full bore.” By then he expects to not only have the seven banks that own Early Warning running on Paze but also thousands of other banks and credit unions.

In the interview, Anderson goes into more detail about what’s been done so far and what’s coming up for Paze, including some lessons learned along the way.

Read more: How to Unleash the Full Potential of Digital Wallets

Building the Consumer Base for Paze

Without merchants that have signed up for Paze, you have nowhere for consumers to use the digital wallet. And without consumers, you can’t convince merchants that accepting a new payment method is going to be worth the time, effort and expense.

Which do you focus on first, then? From the beginning, Paze has been stressing merchant signups.

That’s partly because the seven banks that own Early Warning Services have a total of at least 150 million credit and debit cards that can be loaded into the Paze system.

“In my mind, that’s at least critical mass,” says Anderson, a veteran in payments who spent more than 14 years at Mastercard. “Even just the seven owners give us a very compelling constituency.” This same point of view is reflected in feedback received from merchants, he says.

The owner banks are Bank of America, Capital One, JPMorgan Chase, PNC Financial Services, Truist, U.S. Bancorp (along with its Elan credit card processing subsidiary) and Wells Fargo.

Consumer adoption is a hurdle for any new payment method.

“I’ve learned over time that changing consumer behavior around payments is always time-consuming. It takes a while, and you need to come up with a value proposition that makes sense.

— James Anderson, Paze

But the Paze digital wallet enjoys an advantage with consumers that other digital wallets don’t: it will be coming to them from their banks and credit unions.

“We are from the people who brought you the card. We’re from the people who take your paycheck every two weeks. We’re from the people who lend you money,” says Anderson.

This is “a point of differentiation for us, which is clearly what we’re going to be dialing up in our marketing messaging” to consumers, he adds.

There’s been little of that so far, with the emphasis having been on merchant recruitment.

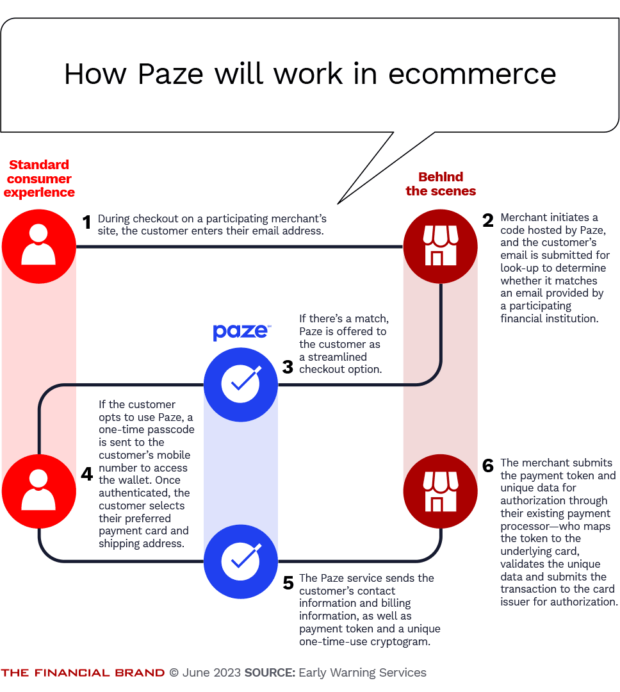

The Mechanics of Paze

Paze contends it has less of a hurdle with consumers than other digital wallets because of the way it works.Unlike Apple Pay or Google Pay, Paze wasn’t meant to reside in an app on consumers’ smartphones. So there’s nothing that consumers have to download.

Consumers also wouldn’t have to enroll, nor load it with their credit or debit card information.

Paze is designed to appear as a payment option on the checkout screens of participating ecommerce merchants. If consumers share their email address with the merchant and the address is on file with a participating financial institution, they will see an option to use Paze on screen when they get to the checkout.

If they click on that option, all cards they have with all institutions taking part in Paze would be present in the wallet (with all of the information pre-loaded by the participating banks and credit unions).

At that point, consumers would choose their default card and the purchase would go on that credit or debit card. But it’s a choice they can override when using the Paze digital wallet for any future online purchase, should consumers want to pay with a card other than their default.

Read more about Paze:

Getting Merchants to Offer Paze as a Payment Option

Anderson says a series of announcements about merchant acceptance is in the offing. These include early adopters like Omaha Steaks.

A key target, according to Anderson, are “tier one” merchants, which the payments industry defines as a merchant that processes over 6 million card transactions annually. Omaha Steaks is one such company and Anderson says that “we’re into double digits on those signed” and that more will be signed soon. This avenue potentially adds big chunks of opportunity to Paze with each signup.

At the other end of the spectrum are smaller merchants with an online presence. Paze is pursuing them in bulk, not onesie twosie. It does this by courting payment service providers and payment facilitators, known in the industry as “payfacs.” The former handle payment processing for merchants that have their own merchant accounts, while the latter handle processing and also essentially “rent out” access to their own master merchant account.

Here is the operative point: “They’re typically bringing in tens of thousands of merchants in one go,” says Anderson.

Building volume will take not only major merchants — “strong brands that consumers recognize” — but also a multitude of smaller ones. Anderson says the partnerships described will help Paze create ubiquity, though he acknowledges this will take time.

“We want to get to every single card-accepting merchant,” he adds.

Read more: Is CFPB’s Mobile Payments Salvo at Apple & Google Good for the Industry?

Eliminating Pain Points for Merchants

One of merchants’ main worries in ecommerce is the abandoned shopping cart. So any factor that can cause confusion or irritation is something to be removed or avoided. One such factor is the “NASCAR checkout page.” That phrase refers to a payments screen covered with logos for various payment options to the point where it resembles a NASCAR racing car plastered with sponsor logos.

One of the pluses that Anderson sees for Paze is the way it will typically come up. It is triggered by the purchaser’s email address being entered.

“So we’re not taking any real estate” — that is, putting the Paze “sticker” on the checkout page, says Anderson. And that also means not creating a click-through situation where people whose card issuers are not part of Paze would find themselves in an annoying dead end.

“We’re not looking to build Paze wallets off the backs of merchants,” says Anderson. “There is no way to get a Paze wallet other than through a participating financial institution. We only want Paze invoked where we can add value and help the checkout experience.”

A new idea has come along as Paze has been talking to larger merchants with ecommerce longevity, according to Anderson. Many of them have repeat customers whose cards have expired. He says Paze has worked out a way to refresh card information for customers who are eligible for Paze. This requires having the merchant trade the payment token initially issued for a “card on file” token, he explains. Paze continues to work on this potential feature to build appeal to this group of merchants.

The “third front” for Paze — beyond consumers and merchants — is adding more banks and credit unions.

Anderson says announcements are coming on that too. While there will be individual deals with non-owner financial institutions, this is also an area where Paze is pursuing institutions through the organizations that facilitate offering their cards. (An example would be banking trade associations with card affiliates that work with member institutions.)

“We’re in deep conversations with these players and they’re seeing a lot of interest among their customers,” says Anderson.

Read more: ‘Real-Time Payments’ Expert Pivots to ‘Chuck,’ a P2P Platform for Community Banks

Questions for the Future as Paze Gears Up to Launch

A good deal has to jell for Paze to achieve the outcome described by Anderson. There are issues that participants from the merchant side and the banking side will be weighing — use of data, compensation for access to customer information, and competitive concerns among financial institutions taking part (big versus small, for example).

The launch in the first quarter, to reverse-paraphrase Winston Churchill, would be only “the beginning of the beginning.”

All of these developments at Paze are also happening at a point when Early Warning Services, the parent company of both Zelle and Paze, will be undergoing a leadership transition. Al Ko, its chief executive since May 2019 left for another job in May. A new CEO, Cameron Fowler, most recently chief strategy and operations officer at BMO Financial Group, starts Oct. 2.