As the world moves from the initial shock of the pandemic into a more steady state of altered reality, financial institutions are finally finding the breathing room to shift from reacting to crises to adapting their business to new realities. In fact, many banks and credit unions are recognizing that the current situation gives them a unique opportunity to attract new customers and grow their business.

Most financial institutions already know that new-customer onboarding programs are where the rubber really meets the road in customer acquisition strategies — where a new account is transformed into a loyal customer. Here are five things that growth-minded FIs are doing to step up their onboarding programs to meet the evolving customer expectations and operational realities of the “new normal”:

1. Enabling End-to-End Digital Account Opening

Online account opening rates at community financial institutions shot up nearly 15% when social distancing policies went into effect. Digital account opening (DAO) has remained at significantly higher levels in the months since. Yet most banks and credit unions still do not offer true, end-to-end DAO.

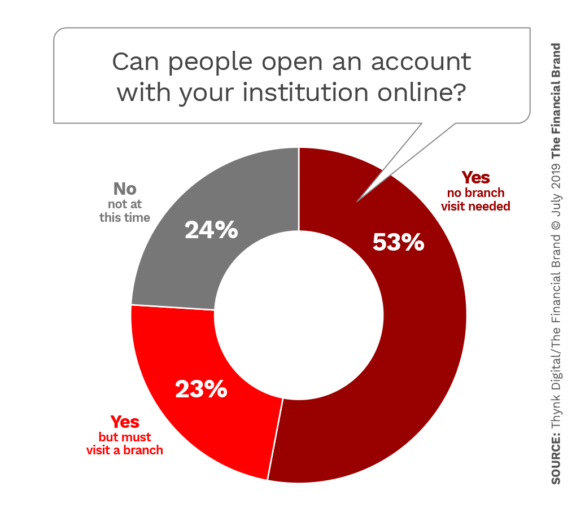

A 2019 survey found that more than half (53%) of institutions said they offered DAO. But when customers who had opened an account online were polled, half of them reported having to visit the branch to complete the process — signing documents, verifying identification, etc.

Making an honest assessment to identify gaps in your DAO process is the first step toward enabling an end-to-end DAO process that can not only dramatically reduce abandonment rates but give you a truly stand-out position in the market.

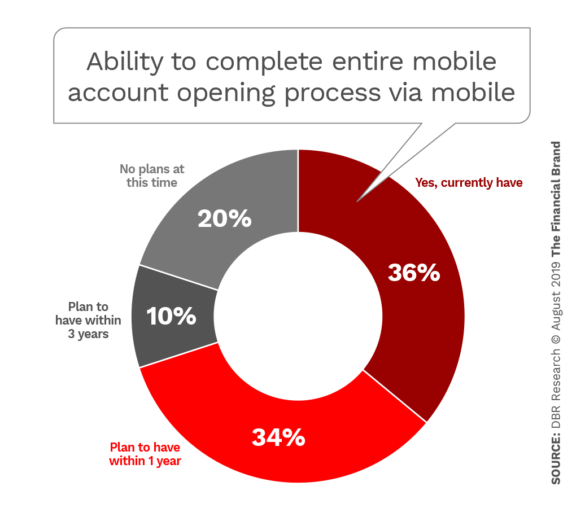

Insider tip: Enable mobile account opening. Now is the time to develop a mobile account opening experience. As smartphones become the medium for so many transactions in everyday life, one in three consumers say they would switch financial providers for a better mobile experience. But just 8% of the typical institution’s account opening activities can be done via mobile, and just 36% of them say they can open a basic checking account via mobile.

2. Pursuing All Abandonment Leads Produces Rich Stream of Business

If a customer walks into a branch with the intent to open an account, the in-person interaction helps address obstacles or concerns for the customer during the account opening process. But according to the Digital Banking Report, prior to the pandemic, one in five consumers were abandoning the online account opening process. That number was more than likely much higher, because many financial institutions’ DAO platforms don’t even save initial customer information (name and email) until the customer completes all initial required fields (i.e., hits the “Save” or “Next” button).

If you can capture all of this contact information — and develop a strategic nurturing program to re-connect with them — you can steer these hot leads back to your institution.

Insider tip: Use the right marketing automation tools. Sophisticated lead-gen tools have traditionally been costly and complicated to use. However, the new generation of marketing automation tools are simpler and intuitive to use, and can be rolled out cost-effectively, thanks to their software-as-a-service, pay-for-what-you-use structure.

Best-in-class marketing automation tools have ready-built solutions for the early-abandonment problem, making it easy to build intermediary landing pages or gateway pages between marketing communications or website calls to action and application forms, where you can capture basic customer contact info for effective nurture.

3. Enhancing Availability Across Digital Channels

The online abandonment problem often comes down to the customer support experience. When people are physically in the branch, it’s easier to assist them immediately with any issues that arise. When that experience moves online, support channels are too often limited to email (with a delay of hours or days) or phone (a jarring disconnect from an interactive digital experience). And while self-service may indeed be what many customers prefer, many others do not want to help themselves.

Fortunately, the pandemic has elevated awareness of several digital channels that more accurately replicate the real-time, personalized feel of in-person service. For example, live text chat is now easy for financial institutions of all sizes to deploy quickly. Enabling video chat and click-to-call capabilities levels up the human element of the service experience.

Led by big names like Experian, more financial institutions are leveraging the built-in communication capabilities of social media platforms (Facebook, Twitter, Instagram) to assist customers in real time.

Insider tip: Online appointment scheduling enhances one-to-one service experience. Just as you likely encourage customers to make appointments to ensure a seamless, personalized experience, deploying an online appointment scheduling solution can add personalization to digital service experiences.

Countless platforms have emerged to meet the sudden demand amid the pandemic, but leading solutions can be deployed in as little as one day and deliver intuitive functionalities that help ensure the right expert is available to connect when it’s most convenient for the customer.

4. Doubling Down on Digital Service Enrollment

Every bank and credit union know that digital services are absolutely critical anchors for establishing new-customer loyalty. But a significant portion of people still prefer in-branch transactions. Their use of digital services remains extremely limited.

Many new account onboarding programs take a well-intentioned customer-guided approach: helping the customer set up services that align with how the customer indicates they prefer to transact. But in this “new normal,” where digital services are often the only option, financial institutions need to double down on promoting, educating and ultimately enrolling customers in the full breadth of digital services.

You cannot afford to wait for the customer to hit a service barrier.

Insider tip: Focus on remote deposit capture. The most common reason customers of all demographics still visit a branch location: to deposit a check. Making sure a new customer is set up for and understands how to use remote check deposit is one of the easiest ways to establish a pattern of loyal customer behavior.

One of the more interesting and effective ways to encourage remote deposit adoption is by sending mobile deposit letter checks — literally mailing new customers a letter with a low-denomination check and instructions on how to deposit it through a bank’s mobile app. This innovative approach gives customers tangible incentive to discover remote deposit capture.

5. Being Proactive About Communication Helps Sell DAO

As every financial institution now moves to a digital-first approach, they should be cautious of moving too far towards the hands-off style of many digital-only financial institutions. Customers may be forced to choose your digital services right now — but they still value your more complete offering that differentiates you from fintechs.

With rapidly evolving circumstances and swirling uncertainties surrounding the pandemic, customers’ needs are sometimes shifting before even they fully recognize it. To build a solid foundation for a loyal customer relationship, and to move from service provider to trusted partner, your institution needs to be confident and bold about reaching out to new customers — early and often — with services and solutions.

Insider tip: Harness AI to anticipate customer needs. Recognizing the need to be sensitive to over-selling during a time of fragility and uncertainty, some of the most innovative banks and credit unions are leveraging artificial intelligence (AI) tools to more accurately predict and anticipate customers’ needs.

These smart tools create complex data-based trigger programs, automatically monitoring customer behavioral data so they can reach out to customers at the right time — for example, delivering relevant information and offers to customers who are actively in the market for home purchases or refinancing, or to reach out to businesses that are seeking lines of credit to help them survive and grow.

AI-driven customer outreach programs are also uniquely suited to the sensitivities of the current time — for example, helping banks avoid sending mortgage-related messages to customers who have forbearances.

Tough Times Forge Loyal Customers

The sudden, profound and evolving pressures of the COVID crisis have challenged every financial institution to rethink how they connect with their customers. These abrupt changes aren’t easy. There’s no understating the risks and fears around losing customers, losing business and losing revenue over the coming months.

But banks and credit unions of all sizes would do well to lean into proactive strategies for succeeding in the new normal that is taking shape — strategies like elevating onboarding to fit a socially distanced world.

None of this will be easy. But those financial institutions that invest in meeting evolving customer expectations and building new customer trust will emerge with loyal customer relationships forged through tough times.