Google indicates that there are hundreds of thousands of references on the web to the phrase “data is the new oil.” Given how politically incorrect fossil fuels are in some circles, this makes the phrase an analogy that’s both apt and awkward.

Apt, in the sense that companies, especially financial institutions, have mountains of historical data to draw on. Plus, they can wade right up to their necks in newer data. Mastercard reports that 2.5 quintillion bytes of new data are generated daily.

Awkward, in that consumers waffle on how they feel about disclosing their data and about how it will be used.

“Many consumers feel brands don’t know them well enough to serve them in a way that makes them feel special,” states an Accenture Interactive report, “See People, Not Patterns.” However, the report continues, “When those brands seem to know too much — and act on that knowledge — they can quickly lose consumers’ trust. That push and pull between consumers’ desire to be known and their wish for privacy has increasingly become an issue for brands.”

Research for TransUnion by Aite Group indicates that financial organizations are seeking additional, external sources of data even as they struggle to make use of what they have internally. (The study included banks, credit unions, insurance firms and other financial players in multiple countries, including the U.S. Over three-quarters of respondents were banks and credit unions.)

“Financial institutions continue to capture a vast amount of information on how consumers behave and interact every day,” says the TransUnion study. “Big data is getting bigger. However, finding valuable insights hidden in the data is becoming more challenging for analytics executives as the number of data sources and types grows exponentially.”

As they work to find the optimum blend of inside data and outside data financial marketers also need to find the right balance between maximizing their use of data and avoiding the possibility of regulatory controls on how they gather and use it. While two out of five expect to explore the use of artificial intelligence to manage and analyze massive data streams, the rules AI will work by must be devised and monitored by humans.

What Creeps Out Consumers, and Three Ways to Ease Their Fears

After surveying thousands of consumers in Europe, the U.K., Canada, and the U.S., Accenture found that consumers aren’t terribly impressed with the algorithms into which many brands pour increasing amounts of data: “Often, digital advertising behaves in a way that suggests a brand does not know the shopper at all. Or a brand collects data without having a clear purpose for doing so.”

Overall, 65% of the firm’s sample said they would provide more data if they saw an improvement in what brands did with it, and 73% said they would do so if brands grew more transparent about how they will use data provided.

Consumers’ top five “creepiest advertising techniques”:

- Receiving an ad for something discussed near a voice assistant but never actually searched for, 73%.

- Being followed by an ad across devices, 69%.

- Dealing with a chatbot that can access your past shopping history — browsing in addition to purchasing, 66%.

- Being shown an ad on a social media site based on behavior on another site, 66%.

- Interacting with a chatbot with access to your past customer service dealings, 64%.

“One central task of leaders in this environment is to limit data gathering to information they have a right to know,” states Accenture Interactive, “and they must provide value in exchange for that data.” Brands that don’t work at this — and the responsibility begins with CMOs, according to the firm — face reputation risk, regulatory risk, and financial risk.

Accenture suggests three tiers of data gathering be established, each with its specific standard:

- Zero-party data: Make consumers want to share data by giving them value in exchange.

- First-party data: Gather only what you have a right to know and what will help to tailor service to the consumers’ needs.

- Second- and third-party data: Approach the use of data from outside parties in a balanced fashion.

Warning for marketers: Accenture found that seven out of ten consumers surveyed would drop a brand if they decided the company’s data usage was invasive.

Read More:

- Data and AI Power the Future of Customer Engagement in Financial Services

- Banking Execs Must Get Hands Dirty to Dig Up Data-Driven ‘Gold’

Making the Most of Data from Multiple Streams

There is a growing abundance of data in many financial organizations, according to Gene Volchek, SVP of global Data Science And Analytics for TransUnion, and yet “a hunger and thirst for more data.” In addition, data already possessed tends to reside in silos that even today don’t always talk effectively to each other, and many organizations need more data analytics talent and application of technology.

A verbatim comment from one of the U.S. retail bankers taking part in the survey speaks volumes: “Data is fractured; there’s no common keys or even a set definition of key terms such as ‘customer.’ 40% to 50% of analysts’ time is spent wrangling the data.”

Volchek says he was surprised to see that U.S. financial companies are a bit behind those of other countries in using AI and machine learning techniques. Regulation represents one stumbling block for financial institutions, because it can make it harder to link certain types of data for forming a full picture of a consumer.

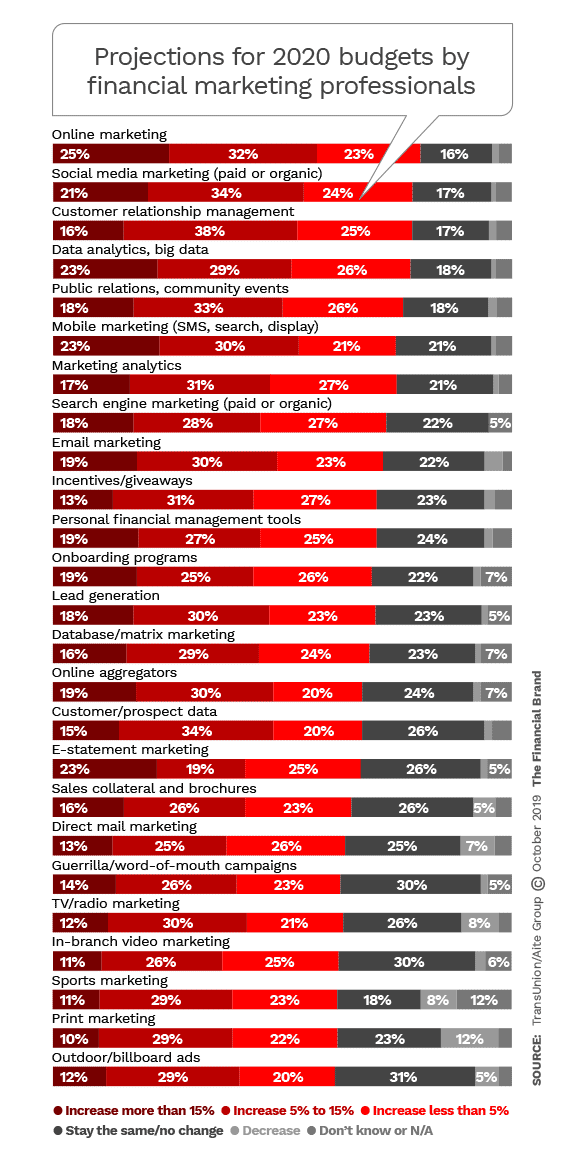

Another hurdle: Respondents indicated that much of their data isn’t quite ready to be manipulated by AI techniques. Data analytics and marketing analytics are two areas of significant spending growth anticipated for 2020, according to TransUnion’s study.

One other challenge to the use of data by financial institutions is what TransUnion calls the “democratization” of data. Volchek explains that analysis used to travel a long loop from the management of the business line to analysts to the information technology staff and back again. There was more control and projects took longer to turn into action. Today’s technology keeps much of the process in the business unit and that shortens the time frame and speed to applying data analysis to the market.

“The traditional handoff no longer occurs,” Volchek explains. While this puts the execution closer to the need, it also argues for pushing data standards further down into a financial institution so all users understand what’s expected. This could help to avoid the kinds of problems suggested by Accenture Interactive’s research.

Serving Consumers Better Means Understanding Them Better

A key aspect of applying data in a bank or credit union is understanding the needs generated by various life events for consumers at different ages and in different circumstances. It’s a fundamental of selling that you don’t offer what you want to sell, but what a consumer needs.

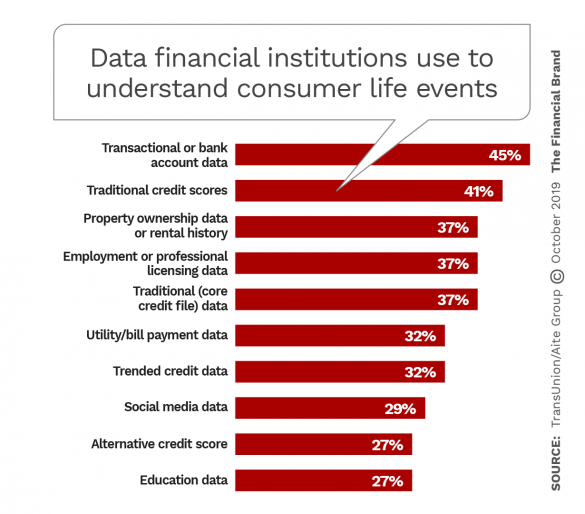

While many financial institutions rely most heavily on two key data sources, bank account data and traditional credit scores, Volchek notes that a growing number of additional sources of data are being added to the stream. Take, for example, trended credit data. The classic report was a snapshot, whereas the more-advanced trended report gives the financial institution a sense of how the consumer has been doing over time. Volchek points out that other, more leading-edge data sources are also being drawn on these days, such as social media postings.

New, alternative types of data are being applied for multiple purposes by financial institutions. While nearly half have been using them for marketing, they serve additional purposes, such as prescreening prospects before they are marketed to.

Even today, when a social media platform is trying to start an international cryptocurrency, a natural question may be, what can financial marketers do with newer forms of data like social media insights?

One of the survey respondents, a marketing professional from a U.S. bank, addresses that in TransUnion’s report: “We would like to bring in sociographic information. For example, what are our customers doing on social media, and what’s available to understand customer behavior in the marketplace?”

Social media data, in fact, was the fourth-highest category of data spending identified in the study. It was surpassed only by data on mobile habits (browsing, app usage and more), the top category, followed by analysis of call center data, and analysis of purchase data.