Financial institution marketing has long focused on the milestones of life — first big job, marriage, homebuying, retirement. But that legacy focus may soon be eclipsed by the concept of financial wellness. Major life events clearly are still important, but are becoming just one part of a much larger priority.

“Financial well-being is not exclusive to those ‘financial moments’ when consumers make purposeful decisions on their finances,” writes Jan Bellens, Global Banking and Capital Markets Deputy Sector Leader for EY. “It is driven largely by everyday behavior and decisions — some big and binary (such as deciding to get a college degree), some small and gradual (such as going to the gym).”

Traditional financial institutions have not typically played a big role in these everyday financial decisions beyond handling transactions and providing loans — and in some cases providing transaction-related notifications. Money management tools mainly center around the monthly financial statement and call-center help. All important services, but pretty unexciting, Bellens observes.

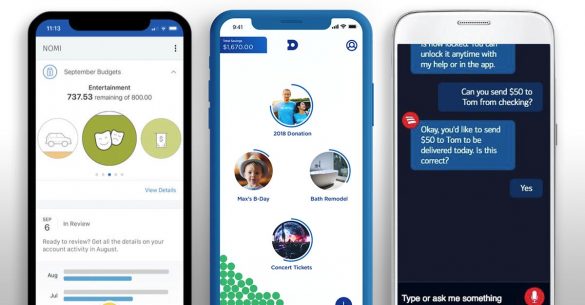

Some financial institutions have launched mobile apps or chatbots that proactively help consumers manage their finances or put aside money (RBC with Nomi, Fifth Third with Dobot, Bank of America with Erica). And while some of these tools have the ability to incorporate a consumer’s full financial picture, the majority of banking apps are still restricted to the banking ecosystem, EY observes.

Nomi, Dobot and Erica

What’s at Stake for Financial Institutions

In 2018 research conducted for Fiserv, The Harris Poll found that exactly half of U.S. consumers say they want a budgeting tool to help them save and track spending, and almost half (44%) want a service that consolidates account information from multiple organizations (for Millennials, the latter figure was 66%). Further, the research uncovered that just over a third (34%) of all U.S. consumers want to be able to manage all their financial accounts in a single, online location or app, and real-time access to their financial information is desired by the same number.

Financial institutions able to meet this changed expectation can increase customer loyalty at a time when people are able to switch banks more easily. “This means banks that embrace financial well-being as a core principle must demonstrate how their digital products and services create lasting value for their customers,” EY states.

So far, most innovation in financial wellness tools has come from the fintech world — with apps like Mint, Acorns, YouNeedABudget, Varo Money and many others. The popularity of many of these digital solutions that use artificial intelligence is spurring more banks and credit unions to up their game. As described in EY articles, traditional institutions have a great opportunity to lead in financial health applications, but they also face the threat that other broader platform providers, notably big tech firms, could move faster to usurp the lead role.

The August 2019 launch of the Apple Card was as example of this point. The mainly virtual card combines money management elements with a credit/debit/instant rewards product residing in your phone.

Why AI-Powered Wellness Presents a Major Opportunity

“Financial institutions have an opportunity to leverage data and technology in new ways,” EY maintains, including the use of predictive analytics and machine learning to help customers find ways to save money and avoid recurring fees. Connecting an AI-powered chatbot or app to a digital wallet could be very powerful. It would allow a financial institution to track spending and use that data to make recommendations.

“Imagine walking into your local supermarket and not only having your phone identify where you are, but also ‘speak’ to your digital wallet and banking app to identify the trades-offs you could make based on your shopping list, or your historic preferences,” EY states.

Gamification in the app could encourage consumers to maximize saving. Then, at the end of the week, the $5 they have saved compared with their typical supermarket visit would automatically be swept into a savings or investment account. A key point is that consumers don’t need to think about it, according to EY. They don’t need to actively engage with a financial service provider. It all happens seamlessly in the background.

This is essentially what the Apple Card does, except that the money “saved” is a cashback reward versus smarter spending.

“Existing banks have a window of opportunity to lead in financial wellness, but they will need to move faster if they want to stay at the forefront of this amazing opportunity.”

— Jan Bellens, EY

Indeed, Bellens warns that “While existing banks have a window of opportunity to lead in [financial wellness], they will need to move faster if they want to stay at the forefront of this amazing opportunity.”

On the plus side, banks and credit unions remain trusted institutions for protecting and securing customer data, the consultant points out. The bad news, he adds, is that traditional banking providers have been much slower in implementing the means to manipulate, analyze and leverage the data for the customers’ benefit.”

Read More: 6 Keys to Designing a Best-in-Class Financial Wellness App

Will Financial Institutions or ‘Platforms’ Like Amazon Lead the Way?

Research indicates there is increased need for financial guidance. Many consumers struggle to get a handle on their personal financial situation. Only 37% say they are satisfied with their financial health, well behind their rating for other areas of life, according to Fiserv.

EY envisions a closer connectivity between technology, financial services and health care industries “given the fundamental connection between physical, mental, emotional and financial health.”

“Health-care firms,” the consultant states, “will use patient-specific data from wearables and mobile phones to build real-time pictures of a patient’s health status, recommending targeted interventions.”

“Financial institutions will be forced to decide if they want to be an aggregator or be aggregated.”

On the financial institution side, “A rich array of data and analytics would enable hyper-personalized interactions that involve nudging, visualization and incentive tactics such as gamification to help consumers maximize their lifetime financial well-being.”

Getting to this point will be difficult for many legacy financial institutions as they must overcome internal technology and organizational silos along with rising standards for data security and privacy. The danger here, according to EY, is that as this broader wellness scenario unfolds, platform operators like Amazon, Google and Apple could be the ones to coordinate “an ecosystem of businesses” including banking, around the consumer.

“This would force today’s financial services firms to decide whether they want to be the provider of the service or part of the ecosystem that is called upon to create curated solutions for individuals,” EY states. “In other words, will your firm be the aggregator, or be aggregated?”

Read More: Today’s Digital Assistants Must Become Bot-Powered Banking Coaches

Financial Wellness Could Lead to Subscription Model

Assuming a bank or credit union decides it would prefer to be more than an aggregated data source, the path for most institutions will likely be partnering with a fintech to provide the necessary capability. Even tech-savvy Radius Bank opted to partner with Wallit, a rewards-based savings app for families and teens. Outright acquisition is another option for some, like Fifth Third did with the Dobot app in 2018.

Either way, that step tees up a larger strategic question, according to EY’s consultants.

“To deliver hyper-personalized experiences, the financial services industry needs to shift its focus away from individual products and toward propositions their customers truly value,” the firm states. It explains that this involves unbundling and then re-bundling products to deliver a tailored experience addressing three primary financial needs:

- Navigation: helping customers identify the best propositions to meet their needs.

- Concierge: helping customers access the right offerings.

- Therapy: helping customers resolve unexpected events and life challenges.

This re-bundling moves banks and credit unions toward a subscription model in which consumers pay for bundles of tailored products and services with fixed-fee pricing certainty and convenience, according to EY. This shifts revenue streams from product-focused to user-focused.

There are two ways to approach this, according to the firm:

- Offering tailored, concierge-style service.

- Adopting a more commoditized “platform play” emphasizing ease of use and accessibility.

Both strategies rely on a foundation of trust, says EY, adding that to truly establish trust, financial institutions must demonstrate to consumers they are doing right for them in all situations.

Beyond that, however, is the growing attitude among consumers, particularly younger generations, of preferring companies that have an ethical and moral approach to doing business. Mintel reports that 66% of U.S. consumers report that it is very important to them that a company acts morally and ethically. Financial wellness plays into that mindset, in contrast to high-cost overdraft plans, for example, or high-fee/high-rate credit cards.

Institutions choosing the platform approach can establish trust by protecting clients’ data and using it to better understand their needs and preferences. However, this option will likely only be viable for the largest financial institutions — on their own or in concert with a big tech company. EY predicts that big tech players will begin to win over financial services clients looking for wellness services, because of their “unprecedented expertise in leveraging data to optimize client experience.”

“It’s no longer enough to simply offer accounts, savings or loans,” EY maintains. “If we want people to be more broadly served financially, then we need to engage them in a digital dialogue … and be more proactive in helping customers achieve lasting financial well-being.”