For more and more consumers, the ability to feel financially secure has become more complicated and increasingly stressful as the burdens of health care, educational funding, retirement, and daily expenses grow. This stress impacts consumers’ personal relationships, physical and mental health, and has a significant impact on productivity at work.

Fiscal wellness reaches far beyond simply setting aside more money. The concept has a foundation of financial education and the need to change current behaviors. Pretty charts and budgeting tools do little good if the underlying behaviors can’t be modified.

Making matters worse, most consumers have no idea of how secure they are (or aren’t). According to research released by Prudential Financial, Inc., one-third of Americans do not have an accurate handle on the state of their own finances, thinking they are either better or worse off than they actually are. The research also found that Americans’ most pressing financial worry is the thought that they will never be able to retire and will have to continue working as long as they can hold a job.

These findings are reinforced by insights from the Center for Financial Services Innovation (CFSI) on individual financial behavior indicators. This study found that when the interconnection between spending, saving, borrowing and planning are analyzed, many consumers turn out to be struggling.

- Only 28% of Americans are considered financially healthy.

- 47% of consumers spent more than or equal to their income in the last 12 months.

- More than a third of all consumers (36%) are unable to pay all of their bills on time.

- Nearly a quarter (22%) of all Americans say they worried that their food would run out over the last 12 months.

- Nearly a third of Americans (30%) say they have more debt than they can manage.

With so many households classified as financially unhealthy by CFSI, it is imperative that traditional and non-traditional financial services organizations provide financial wellness tools that can change consumer behavior.

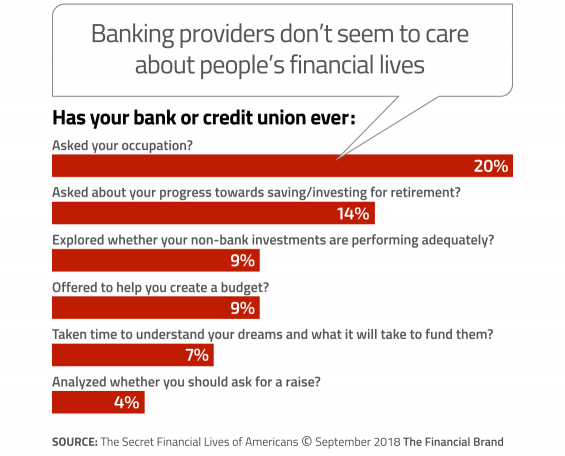

Virtually no traditional financial institution offers the tools that consumers in need require. Third-party budgeting apps are only a small part of the solution to relieve financial stress. Making matters worse, most banks and credit unions don’t even collect the basic data needed to provide basic assistance.

There is a great opportunity for financial institutions to leverage data already collected and insights consumers would be willing to share. What is needed is a great financial education tool, tracking capabilities, a rewards component, ongoing engagement and a “personal financial trainer.”

Correlation Between Physical Health and Fiscal Health

In much the same way that weight loss is only part of a healthy lifestyle, saving is only part of a strong financial lifestyle. The behavioral aspect of making changes in a person’s life is what can make losing weight and keeping it off or saving money permanent. So any program that is built to make a major lifestyle change needs to focus on the mental component.

With physical wellness, one of the leaders in the industry is Weight Watchers (now known as WW). The success of Weight Watchers is attributed to the tools they provide to encourage healthy behaviors. Beyond recipes, packaged food products, calorie and fitness tracking tools, and a rewards system, they also provide ways for people to meet in groups and work with wellness coaches. Weight Watchers understands that struggles with weight loss have a lot to do with personal thoughts and emotions that tend to be barriers.

A new entrant into the physical wellness category is Noom. With many of the same strategies and components as Weight Watchers, Noom provides all of the tools in a completely digital format. In other words, all of the health education, recipes, daily engagement, calorie and fitness tracking and even the coaching is done through a mobile app. Yes, Noom is unique because it provides a live health coach — not a bot — that a subscriber can communicate with within the app.

A member logs in first thing in the morning, enters their weight for the day, reads highly personalized daily wellness education tips and completes short, entertaining quizzes that provide insights for future engagement. This begins the process of tracking meals consumed and calories burned.

Making a usually tedious process of tracking calories simple, Noom has a food database of close to four million options with the values for different portion sizes. Leveraging an easy crowdsource functionality, the Noom database grows continuously when members enter missing recipes or food brands. Fitness tracking is done through integration with a number of tracking apps including Apple Health.

So what can a digital wellness program like Noom teach bankers and credit union executives about building a digital financial wellness app?

1. Simple Enrollment

A financial wellness tool will only be successful if the offer is strong and the enrollment process is easy. Interestingly, Noom does the majority of prospecting using mobile-friendly GIFs on Facebook and Instagram. Because the Noom app is designed for mobile, it is highly engaging and simple to use. A successful financial wellness tool should also be designed in a way that would generate prospects using short-form videos.

“The digital prospect doesn’t want to read about your financial wellness app, they want to see it in action on their phone.”

Once a prospect is enticed by one of the many ads on social media, Noom makes the early enrollment process easy. As with any good mobile app, Noom captures the prospect’s email address first and foremost. This allows anyone who disengages during enrollment to be re-targeted with additional incentives. After the email is collected, the Noom prospect is walked through a completely virtual enrollment process. The cost of the program is about $49.50/month (after a free, 14-day trial).

When was the last time you saw a traditional banking app that had a “personality”? Is there a financial wellness app in the marketplace that looks like it will be easy to use, fun to engage, and have the components needed to change behaviors? Most importantly, is there a banking app in the marketplace that is not ashamed of charging a fee because of the scant value it provides? As an aside, collecting a credit card information for post-trial purchase provides an amazing amount of data that can be used to help financial wellness engagement.

2. Digital Engagement

Immediately upon enrollment, the digital onboarding process begins with the Noom app. The Noom onboarding process is both direct and entertaining. A user will quickly realize that Noom provides solid science, practical coaching, and applicable behavior change techniques. The casual and fun brand personality comes out in every communication from Noom. Most importantly, insight is collected every day, including user fears, barriers, habits, etc., build new habits.

Noom’s digital interface really simple. Every day, the user is presented with a list of tasks to complete, including logging meals, weight, and exercise hours (it automatically tracks step count). There are insights about nutrition and fitness that the user is encouraged to read, with brief quizzes after each part of education. All along the way, the tone is fun and casual, delivering education in a very informal manner.

“Collecting information about financial fears, barriers, current behaviors, etc., allows for highly personalized contextual engagement and recommendations.”

For a financial institution building a best-in-class fiscal management tool, it will be important to avoid “bankspeak” that is both hard to understand and creates fear and reduces trust. The tool should be completely within the app as opposed to using traditional direct mail, email or even texts. Remember, a digital consumer wants to do everything within an app. An added benefit is that the consumer can go to one place, providing personal insights that can be used for future personalization and highly contextual recommendations.

3. Tools and Insights for Success

The Noom weight loss app uses a whole lifestyle approach, meaning the focus isn’t just on the food eaten. Though food choices are important, the app focuses more on the psychological aspects behind food choices and slowly changing old habits. Noom’s big-picture approach is similar to the Weight Watchers’ design. Every day, new education is provided in an engaging way, without heavy science or use of fears to convince. “Slips” are understood.

Financial institutions have the ability to help consumers with their fiscal fitness journey. If not, there are thousands of highly qualified professionals that can be enlisted to build a curriculum. The key is in the delivery. Can the financial education be delivered in an engaging and easy-to-understand way? Most financial planning processes are hard to understand and are similar to drinking from a fire hose – too much, too fast. Remember, the power of engagement is a communication partnership where the consumer wants to come back to the app daily.

As mentioned, one interesting component of the Noom program is the massive crowdsourced database of foods, recipes and brands. With close to four million entries, it is hard not to find the calorie count of any food a user purchases. Imagine how powerful a similar database of utilities, retailers, etc., would be as people want to easily set up budgets or make payments. No data entry … just search and select in a manner built for mobile.

4. A Human Coach and Group Support

Despite being a mobile-only solution, each Noom user is assigned a Goal Specialist (GS) or coach who is available to give the user individual guidance and support. There is personalized communication provided at least once a week through the app’s messaging system. The Goal Specialist helps to set new, short-term goals that are easy to achieve. If the user’s wants additional support, they can have dialogue with the GS during the work week if desired – all within the app.

Part of the challenge with financial management is the embarrassment of not being able to handle personal finances. Another challenge is the feeling of being overwhelmed by the scale of the daily financial challenges. A highly accessible human coach is the differentiator that can make a major difference for a financial institution. Instead of needing to visit a branch office weekly (or daily), the availability of a human who understands your personal situation is powerful.

After two weeks in the Noom program, Groups are available to join. These are groups of similar people with similar behaviors and goals. While not required, this can increase interactivity and provide a greater potential for program accountability and success. I have never seen a financial institution that has built a platform for group support … within an app. Leveraging the dynamics of social media apps like Facebook, group dynamics can be powerful.

5. Focus on Behavior and Accountability

It is a well-known fact why many diet programs don’t work long term. They focus on food rather than behavior. A successful health plan is more than knowing what to eat. It is about emotional needs, habits and accepted norms. Noom’s emphasis is primarily on underlying behaviors and habits. As an example, each user is asked about their “Big Picture Goal” (that has nothing to do with weight) in the first few days of the program.

“It’s not about the strength of one’s willpower; it’s about behavioral change. And behavioral change is a skill that can be learned.”

Virtual accountability is built for the busy consumer. Instead of meetings or long discussions, everything with the Noom app is about small steps to a large goal. Never is the process overwhelming, yet the user is held accountable on a daily basis.

The lesson for a financial institution wanting to build a best-in-class financial wellness application is to avoid emphasis on budgets, spending and other traditional components. While these are important, it is far more important to understand the “whys” around poor financial behaviors. When these are understood (through ongoing data collection), a bank or credit union is in a better position to help a user meet their goals. By breaking down the behaviors and activities into daily bites, financial management never will feel overwhelming again.

6. Rewards

Like many personal wellness programs, both Weight Watchers and Noom provide a reward system for encouragement. While a “treat yourself” food component is part of the rewards system, it is meant to eliminate guilt for “slips” more than teasing with sweets. Instead of food as a reward, Noom builds a reward system that encourages purchases of clothes, fitness equipment, self-help books, etc. The focus on reinforcing behavior with other behavioral tools is powerful. Noom even has “surprise and delight” recognition that is used infrequently but effectively.

Financial institutions could easily build a gamification component into a financial wellness app. Everything from a reduction of a current loan rate to a social activity for ‘achievers’ could be effective.

Tech + Humans for a Best-in-Class Financial Wellness App

For Noom, the use of data, AI and a human component has resulted in success for the company and its users. By using user insights collected in small doses every day, a personalized solution is created that leads to greater success. This is definitely make easier when all data and interactions are collected within the Noom app. Noom has reported industry high results in user weight loss and length of engagement.

The same kind of success could be achieved by financial services organizations that understand the dynamics of digital technology, data integration, consumer behavior and communication. There is a massive opportunity in the banking industry to deliver tools that can help consumers that are non-traditional and mobile-first. The opportunity can be very lucrative, since there is no reason a digital financial wellness app couldn’t be offered to the mass market with new customer growth being a very large side benefit.