By now there can’t be a financial institution marketer with a pulse who isn’t keenly aware that the competition for consumers continues to rise to levels never seen in the formerly staid banking business.

Anything that helps marketers and retail banking executives to meet that challenge is hugely valuable, particularly insights into 1. customer acquisition and 2. customer retention. While bank and credit union customers have proved to be sticky compared with the experience in other industries, several factors could alter that. Two in particular that are frequently mentioned are the rapid inroads of digital technology and the changing expectations of consumers for product and service capabilities in the digital age. But are they the biggest reasons?

Digital agency Yes Marketing surveyed 1,000 U.S. consumers to determine what factors influence their decision to stay with their current financial institution or look elsewhere. And then, flowing from that, what lessons can be drawn for financial marketers in terms of the stories they tell new and existing customers?

What are the Key Acquisition Drivers?

There are many ways to look at the challenge of attracting consumers to do business with your institution. Yes Marketing focused on two in particular: product and service factors, and trust in the institution.

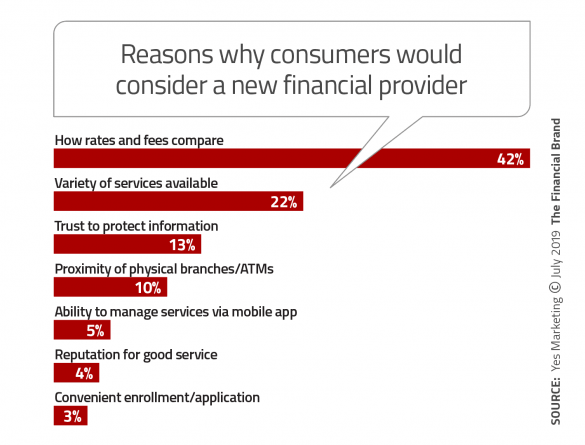

Looking at products and services first, one factor — how rates and fees compare — ranks highest among the consumers polled. Asked to choose the single most important influence for selecting a new banking provider, two out of five (42%) selected “rates and fees.”

The survey did not distinguish between rates and fees, nor between rates paid and rates charged. But having had a taste of somewhat higher deposit interest rates for several years, it’s likely that consumers are eager to hang onto what they can. Loan rates, of course, are a perennial competitive factor, as are fees. In fact, banking fees have long been one of the biggest sore points for many consumers, a factor that challenger banks have jumped all over with their “no fee” offerings.

Just over one fifth of consumers (22%) say the range of services available is a key factor in considering a new financial institution. Marketers who may be thinking, “We’re a full-service institution with a wide range of products,” may be missing the point. The typical bank and credit union offers pretty much the same product and service lineup as every other financial institution. But today consumers expect even greater choice. (Consider that on Prime Day, Amazon promised over a million deals.)

As companies that haven’t traditionally been considered competitors to banks and credit unions expand their services (e.g., Robinhood, Wealthfront, SoFi and others), traditional players need to cater to changing consumer needs by adding complementary services beyond the staples that are now considered table stakes, stakes the report. It recommends, for example, that banks and credit unions “consider offering bank-agnostic money transfers (supported by integrations with brands like Zelle or Venmo), tax services such as those offered by TurboTax, or free credit monitoring services offered by brands like Credit Karma.”

Trust comes in as the third-highest-ranked influence. Traditional financial institutions enjoy an edge over new competitors here — for now. Accenture research backs this up. The consulting firm found that among consumers worldwide, three out of five would be willing to share significant personal information with their banking provider, including location data and lifestyle information, in exchange for a better deal. People are much less willing to trust other types of companies to the same degree.

Why do we say, “for now”? Marketers must view the trust factor through a generational lens. When Yes Marketing analyzed consumers’ top three factors influencing their choice of financial institution (rather than just the #1 choice, as shown in the chart above), younger consumers emphasized trust substantially less than older generations. Only 14% of 18-21 year-olds and 19% of 22-37 year-olds included trust in their top three choices, compared to 34% of 38-52 year-olds and 47% of 53-71 year-olds.

Read More: Innovation Driving More Consumers to Switch Banks Now

Don’t be Misled by Seemingly Low Importance of Mobile Apps

Generational differences also come into play regarding the availability of a mobile banking app. As shown in the chart above, a tiny 5% of respondents overall consider that to be a top reason to consider moving to a new provider. Younger consumers, however, are much more likely to prioritize it. 42% of Gen Z respondents and 37% of Millennials include “Ability to manage services via mobile app” among the top three factors they consider in a banking provider, compared to 34% of 38-52 year-olds and only 18% of 53-71 year-olds.

In addition, as Nessa Felleson, senior marketing strategist at Yes Marketing, notes, consumers now simply expect that they can bank how they want to — by website, app, in person or by phone. A mobile banking app is no longer a novelty or even a value-add like it was even just a couple years ago, she points out. In other words, the low ranking of “digital” actually indicates just the opposite of what it might at first glance suggest. Certainly the soaring use of mobile banking apps would seem to confirm that.

Similarly, proximity to physical locations is a much lower priority for consumers than it was a decade ago. Many people just don’t need to visit physical locations anymore — and don’t want to. Only 10% cite it as a factor in considering a new institution. And note that this includes not only branches, but ATMs as well.

Transparency Builds Trust in a Financial Institution

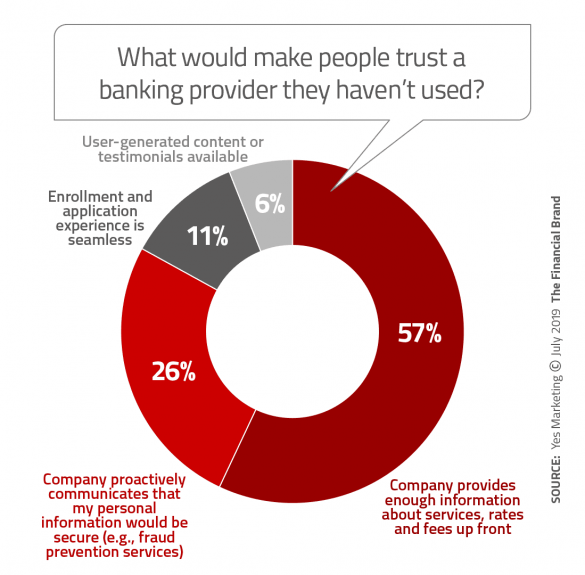

The research probed what would make consumers trust a financial institution enough to try using a new one. The top answer: Consumers are most likely to trust a bank or credit union if it provides specific information about rates and fees up front.

“More than half of consumers say rate and fee transparency is the most important contributor to trust.”

Echoing the finding regarding products and services, more than half (57%) of consumers say that rate and fee transparency is the single most important factor contributing to trust — far more than “proactive communication about security,” “seamless enrollment” and “testimonials.”

Financial marketers seeking to attract or retain consumers should consider this finding carefully in crafting their messaging. Transparency, particularly in regard to rates and fees, is an area where many traditional financial institutions don’t have a stellar reputation, falling back too often on minimum disclosures and opaque legalese not all of it required by regulation Just as people expect a mobile app to be easy to use and reliable, they want clear, accessible information about rates, fees, payoff dates, and various other terms.

Read More:

- Are People Happy With Their Bank? Study Reveals Blind Spots and Problems

- How to Acquire More Checking Accounts in an Amazon World

Relevant Marketing Messages Improve Acquisition

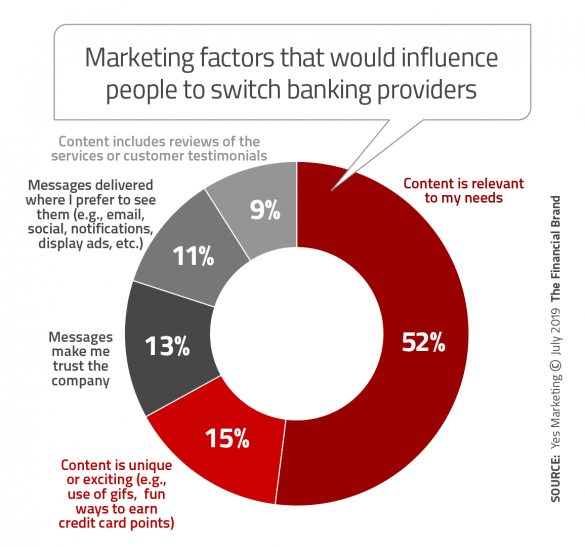

If you’re not communicating with consumers about the services they are interested in, the Yes report warns, “you’ve lost them before you get to know them.” Supporting that, data show that half of responding consumers ranked relevant marketing content as an important factor in deciding to use a financial institution.

No other factor comes close to relevance in importance in terms of messaging. That’s where a consumers’ existing institution has an edge — or should have — because of the amount of data it holds about the person versus having to rely on third-party data. However, new entrants into financial services are adept at using the latest analytics software and machine learning to personalize their digital marketing, something relatively few banks and credit unions have mastered.

As the report states, “Even if a consumer hasn’t engaged much with your brand, you should use whatever data is available to ensure they’re receiving relevant information. For example, target a consumer who has browsed your website’s page about auto loans with information about your rates and offers in that specific category.”

Financial Institution Messaging Needs Work

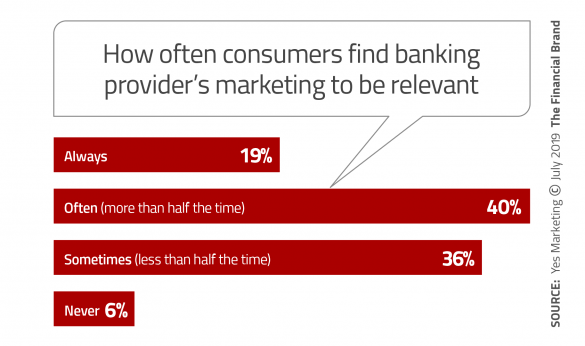

In terms of the frequency of marketing messages, bank and credit union marketers are getting things about right. The relevance of messages — much more important — turns out to be a weak spot.

About seven out of ten consumers say the frequency of email, text, and mobile app messages from their financial institutions is fine. In fact, two in five wouldn’t mind more text messages.

However, Yes Marketing found that two out of five (41%) of consumers say they rarely or never receive relevant communications from financial brands they use. “Considering the importance of relevant marketing messages throughout the customer lifecycle,” the firm states, “there’s no excuse for targeting customers you already have with content they don’t care about.”

Financial services companies are missing huge opportunities to provide timely and helpful content, the report states. “To keep customers around long term, don’t just self-promote. Create relevant educational content that indirectly relates to your offerings.” As an example, it mentions how Capital One offers links to its Learning Center in its app on topics relating to whatever the person is looking at.

But Will They Actually Switch?

In its 2019 U.S. Retail Banking Customer Satisfaction study, J.D. Power found that only 4% of customers had switched banks in the previous year, the lowest level since the study had been initiated. As mentioned in an earlier article, that could be the result of several factors including not needing to switch when moving, because so much banking can be done digitally, and also that many consumers are using new financial services providers without closing their primary financial relationship.

Nearly three quarters (72%) of consumers responding to Yes Marketing’s survey say they are not considering switching to a new financial services company. On its own, that would seem to be a strong vote for legacy institutions.

Nevertheless, complacency in the digital age is a highly risky strategy. For one thing, if 72% are not planning to switch, that means 28% of consumers are open to switching. In fact, younger consumers are far more likely to say they are considering a move to a different financial institution — two out of five (40%) 18-21 year-olds and 35% of 22-37 year-olds.

One of the best ways to thwart any intention to move elsewhere is continue to introduce innovative and easy-to-use services that fit into customers’ lives. Person-to-person payment capability is one example. As the Yes report states, “The easy integration of services into customers’ daily lives raises the barrier for switching to a competitor.”