The word “fintech” still translates to “start-up” for many in the banking industry. And that’s not completely wrong. New fintech ventures hatch all the time.

Looked at in total, however, the fintech marketplace has grown up. As described in an EY report, fintechs today are a thriving mix of start-ups and numerous established companies that offer a broad array of financial services worldwide.

The main reason for that growth is that consumers, as well as small and midsize businesses, are embracing fintech services at a blistering pace. Worldwide, more than three out of five (64%) of digitally active consumers engage in one or more fintech services, EY found. Among the fintech companies the firm considered: Discovery, Yolt, Coinbase, Marcus by Goldman Sachs, Moneytree KK, Grab Financial Group, Funding Circle, and Juvo.

“No longer just disruptors, fintech challengers have grown into sophisticated competitors, with an increasingly global reach,” says Gary Hwa, EY Global Financial Services Markets Executive Chair. Fintech players strive to make financial services more accessible for both consumers and businesses, Hwa states. “By connecting customers to a digital world, fintech enhances their experiences, making them efficient, economical and frictionless.”

This dynamic does not operate in a vacuum, however. Bank and credit unions increasingly are embracing (or at least see the urgent need to embrace) digital transformation to match the expectations of consumers. More and more often this is taking the form of partnerships or other arrangements between incumbents and fintech providers.

Key themes from EY fintech adoption report

1. No longer just disrupters, fintech challengers have grown into sophisticated competitors, with an increasingly global reach.

2. Many financial incumbents, such as banks and insurers, offer credible fintech propositions of their own.

3. The interactions between challengers, incumbents and players from outside the financial industry are forming fintech ecosystems that are replacing traditional bilateral partnerships.

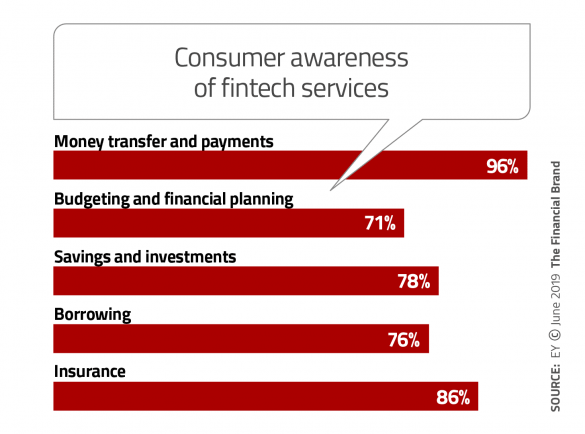

Fintech Awareness Huge Among The Digitally Active

According to EY, fintech adoption among consumers has nearly doubled over the past 18 months. In addition to the 64% of consumers that use one or more fintech services, a staggering 96% of the 27,000 consumers surveyed internationally are aware of at least one alternative fintech service relating to making a payment or transferring money.

The figures vary greatly by country depending on political, regulatory, legal and other factors. China and India are at the top with 87% fintech adoption, thanks in part to the massive usage of the Alipay and WeChat ecommerce apps in China and the Paytm payment app in India.

The lowest adoption rates are found in Japan (34%) and France (35%). The U.S. comes in at 46%, but EY points out that U.S. consumer adoption of fintech services has grown 23% in the last four years. Other notable adoption rates: Russia and South Africa (82%), Peru (75%), The Netherlands (73%), the U.K. (71%), and Germany (64%).

One of the reasons for strong growth in consumer adoption of fintech services is that “traditional financial services companies have entered the fray in a big way,” notes Hwa. Many financial institutions have sprung into action and are offering fintech solutions — either on their own, by partnerships or by forming fintech “ecosystems” that EY sees as replacing traditional bi-lateral partnerships.

“We fully expect this trend to accelerate as nonfinancial companies enter the space and leverage technology and innovation to provide frictionless, transparent and highly-personalized services,” states Matt Hatch, Partner, Ernst & Young and the EY Americas FinTech Leader. EY considers nonfinancial companies (Google, Apple, Amazon, for example) distinct from both fintech challengers and traditional financial services companies.

Read More:

- 4 Myths Preventing More Fintech+Banking Partnerships

- Trends in Fintech Collaboration: Start With The User Experience

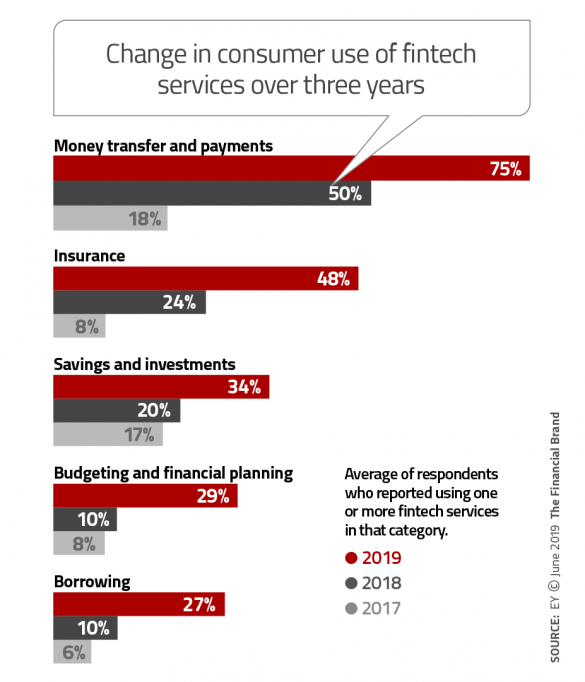

Payment Products No.1, but Budgeting and Savings Have Potential

Consumer use of fintech products and services in all of the banking-related product categories in EY’s study has dramatically increased in each of the firm’s three studies from 2015 to 2019. Money transfers and payment products remain the most widely used, with 75% of consumers using at least one fintech service in this category, up from 50% in 2017.

The most commonly used services in the payments category are peer-to-peer payments, non-bank money transfers, and in-store mobile payments, according to the report. The key to their popularity, it says, is the ease of setting up an account. Other services, such as lending on peer-to-peer platforms, have seen slower growth due to restrictions or regulations in some markets.

EY sees strong growth potential for budgeting and financial planning along with savings and investment services. “Part of the opportunity lies in reaching out to the demographic groups where adoption rates for these categories are still relatively low, including women, consumers in rural areas, and consumers without university degrees,” the report notes. The use of fintech savings and investment services, for example, is 27% for women and 40% for men.

“Only 27% of fintech users would prefer to chat with their bank using social media versus the institution’s own app or traditional channels.”

— EY report

Even among so-called fintech adopters (people who use a fintech service), security remains a primary concern. The research found that while adopters are much more willing than non-adopters to favor an app that allows them to view all their financial products in one place, they are actually more worried than non-adopters about security (71% to 65%). Interestingly, only 27% of adopters would prefer to chat with their bank using social media versus the institution’s own app or traditional channels.

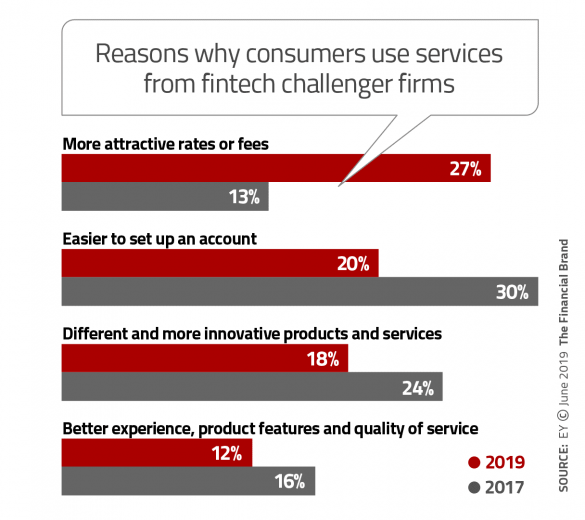

Frictionless Onboarding is Now Simply Expected

EY’s latest fintech research found a marked shift in reasons why consumers would choose to use a fintech provider. The firm considers it a telling sign of the fintech industry’s maturation that twice as many consumers in 2019 rank rates and fees as more important in their selection of a service than ease of opening an account. The latter was the top priority in the 2017 research.

“Fintech providers have evolved from simply trying to lure curious or frustrated consumers with an easy set-up process to developing new strategies to retain existing customers and induce them to make educated choices,” the report states.

Chinese consumers rank ease of onboarding as the least important consideration, EY further notes, reflecting the widespread adoption in that market of open APIs and platform-based services, which has made opening any kind of financial services account virtually frictionless. The research and consulting company believes China could be a leading indicator of what will happen in the U.S. and elsewhere as consumers here also come to expect a frictionless onboarding experience.

Read More:

- How Banks Can Prevail in a Fintech, Techfin World

- Fintech for Good: Five Innovators Changing The Banking World

Consumers Only Partly Embrace Non-Financial Companies

Since the release of the previous EY fintech report in 2017, the competitive spotlight has shifted to a degree away from fintech challengers to “big tech” challengers. In its new research, EY doesn’t focus on companies such as Google, Amazon, Facebook and Apple, but treats the category more broadly as “non-financial services companies.” These would also include telecommunications companies, retailers, automakers and others.

This emerging “non-financial company” threat could actually pull fintechs and incumbents closer together, EY maintains. “Challengers and incumbents alike face a new competitive threat that comes from outside the financial industry altogether,” the report states. These large nonbank firms increasingly are developing their own technology-enabled financial services offerings, building on existing relationships with customers.

EY found that nearly seven out of ten consumers (68%) are willing to consider a financial product offered by a non-financial services company. Consumers are most open to retailers (45%) and telecommunication firms (44%) as financial services providers, and most willing to use such services as digital-only banking and multi-merchant e-wallets.

That finding should be welcome news to communications giant T-Mobile, which launched T-Mobile Money in partnership with BankMobile, the mobile-first division of Customers Bank.

However, the road to financial services riches may have a few potholes for non-financial firms. EY confirms existence of a trust gap among many consumers — even digitally active ones — when it comes to financial services provided by non-financial companies.

The firm found that almost half (47%) of consumers polled said they would be happy to use financial services from a non-financial services company, if the company was working in partnership with a traditional financial company. 27% said they would be happy to use such services if the non-financial services company partnered with a fintech challenger. Just 18% said they would be happy to use the services if the non-financial services company offered them on its own.

That finding creates opportunities for both incumbent financial institutions and fintech challengers, EY concludes. “Even though non-financial services companies have led the way in deploying new technologies to deliver innovative services and have raised the bar on consumer expectations, they do not yet have the full confidence of consumers when it comes to providing financial services on their own.”