In an industry that often fails to communicate in a manner that’s clear and understandable to the majority of the public, credit card terms and conditions represent a special challenge. Many more cards are out there than there are consumers who completely understand what they agreed to.

Research by Visible Thread indicates that 90% of the terms and conditions statements used by card issuers tested by the firm require a college education in order to be understood. In fact, only one set of terms tested — from Valley National — is easier to read than the firm’s harder-read standard, Moby Dick. On average Americans read at an eighth-grade reading level.

Credit card terminology is notorious for its opaque nature. Even in the days when cards were primarily marketed via “take-ones” and direct mail, lengthy disclosures of terms and conditions appeared in tiny, tiny type on long foldout sheets. Various legislative efforts, including passage of the 2009 Credit Card Accountability, Responsibility, and Disclosure Act — CARD Act for short — have attempted to improve transparency and disclosures.

Yet much of what consumers see remains hard to understand. Even where the language isn’t too advanced, other faults, such as too much use of passive voice, an academic tone, long sentences, and dense prose, can impact clarity. The report ranks institutions based on five different factors, with the overall top performers being Valley National; Bank of the West; USAA; HSBC; Chase; MB Financial Bank; Capital One and Citi (a tie); KeyBank and First Citizens Bank (a tie); and Discover.

Read More:

- Key Trends Reshaping Credit Card Marketing

- Study: Most Consumers Have No Clue What Financial Marketers Are Talking About

Card-Offer Clarity Improves Trust, Not Just Grammar

Visible Thread’s report indicates that this pattern of poorly crafted language impacts consumer trust. Citing the 2018 Edelman Trust Barometer, the report points out that the #1 action consumers say financial brands must take to regain trust is publishing easily understood terms and conditions.

Visible Thread’s report indicates that this pattern of poorly crafted language impacts consumer trust. Citing the 2018 Edelman Trust Barometer, the report points out that the #1 action consumers say financial brands must take to regain trust is publishing easily understood terms and conditions.

Yet, according to the Visible Thread report, credit card issuers continue to publish marketing materials online and otherwise with complex terms and conditions.

“If misunderstood, these can lead to serious issues for consumers, including unsustainable indebtedness,” according to the report. “At its most benign, complexity diminishes trust. Ultimately, more informed consumers will move their banking needs to the organization that communicates simply. Those who are less advantaged in society may miss the complex detail, and suffer default.”

Here is an example illustrating that in spite of disclosure duties, plain language remains possible:

Original Text: “The exact fee will be disclosed when the promotional offer is made to you, and will be charged when the transaction is posted to your account.” [1 sentence, 26 words, 4 usages of passive voice, 11.8 grade level]

Suggested Simplification: “When we give you the promotional offer, we’ll let you know the exact fee. And we will charge you when we post the transaction to your account.” [2 sentences, no passive voice, 4.8 grade level]

Read More: Three Marketing Strategies To Boost Credit Card ROI

Looking at Major Card Issuers’ Ratings

Using artificial intelligence and natural language processing, Visible Thread analyzed terms and conditions language on the web from 50 large U.S. card issuers. The Financial Brand also asked the firm to analyze terms and conditions for some major nonbank brands — Amazon, Google, and Starbucks — that have partnered with banking institutions to offer cards.

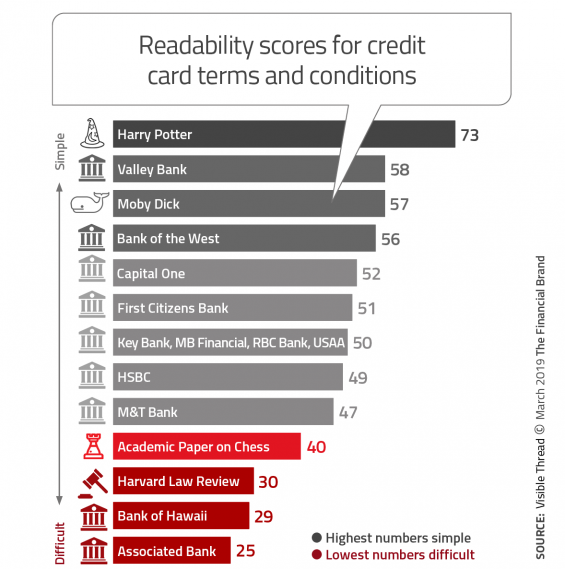

Some of the best and worst programs, as scored for readability, are shown in the table below. The study indicates that experts recommend striving for a score of 60 when aiming for the typical American consumer. The Harry Potter books come in much simpler, at over 72 on the Flesch Reading Ease Scale, Moby Dick comes in at 57.9, and at the far, less-readable end, come an academic paper about chess and the Harvard Law Review. (The most readable document ever would score 100 on this metric.)

The findings for the scans of the additional cards analyzed at our request were a mixed bag. The Amazon Rewards Card, issued by Chase, scored a 50 on the readability scale, as did the Google Store Card, issued by Synchrony. The Starbucks Card, issued by Chase, scored a 49. The Amazon Store Card scored lower, a 38.

4 Points for Cleaning Up Your Own Terms and Conditions

Some of the study’s specific findings:

1. Not one program used terms and conditions written to an 8th-grade level. Only two institutions came close: Valley National’s Gold Mastercard scored a grade level of 8.8 — essentially, just short of 9th grade. A 9.1 level went to Bank of the West’s Cash Back World Mastercard Card.

At the other end, the bottom ten issuers averaged a grade level of 14.67 — close to the level of a college junior. Associated’s grade level ranking came in at 16.1 — essentially, at the level of a college graduate.

2. Most issuers use too many complex words and phrases. The report makes reference to plainlanguage.gov, a federal site curating government plain English requirements and related blogs and tips, as a source of complex words and their simpler alternatives.

A score of 1 or below for complexity is preferred. Only two issuers met that standard, USAA with a 0.68 and BMO Air Miles World Elite Mastercard at 0.87.

By contrast, the poorest complexity score, 3.55, was shared by three programs: Texas Capital Bank, Flagstar Bank, and Webster Bank. All three low scores related to American Express Cards issued by the banks.

3. Everyone markets like a professor, with too much use of passive voice. No program went unscathed here. Visible Thread’s methodology found them all heavy on “academic tone.” For example, a passive construction like “Quality is monitored,” the report explains, can be turned around and made stronger as “We monitor quality.”

“Passive voice levels should be at 4% or lower,” the report states. “The average of all 50 financial institutions is 21.62% — a shocking 5.4X the recommended level.” The 4% target and the complexity target in the previous point are both based on Visible Thread’s analysis of the documents of clients over the last five years.

“Even the two top performers need to use active voice more to reach acceptable levels,” the report says of Valley National and Bank of the West.

4. Every issuer indulges in too many long sentences. Ideally, the report advises, no more than 5% of sentences should be over 25 words — try telling a lawyer or compliance officer that.

To paraphrase veteran NBC newsman Edwin Newman in his 1974 book Strictly Speaking: Will America Be the Death of English? no one involved in the law will abide a period when a comma will do, on the off chance that it could create a loophole someone might squeeze through.

An overall parting shot from Visible Thread: “Most industries struggle with content quality and clarity. Financial Services is among the worst offenders. The causes can vary, but culture is often a large influence. … Culture can create preconception that regulations and compliance matters must be complex. And because they are highly educated, industry employees overestimate the average customer’s sophistication.”