Financial institutions have two ways to grow credit card receivables and revenue: Acquire more cardholders or increase spend among existing ones. Of the two, investing in existing cardholders typically yields a higher return on investment.

The challenge is identifying which existing cardholders to target and determining what changes in behavior are needed to generate added value. To help sort out the options, credit card issuers should tap the rich transaction and credit bureau data they have on cardholders to inform targeting and messaging strategies.

There are three steps banks and credit unions can follow to accomplish this. The first step addresses consumers who have just opened credit card accounts with an institution.

1. Engage With New Cardholders Early and Often

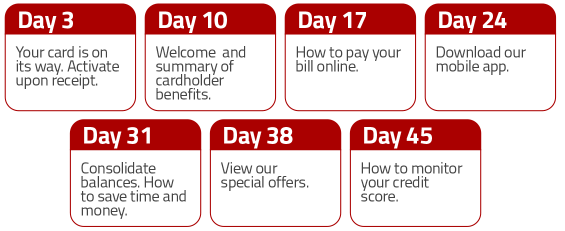

The first 45 days after a new credit card account is opened are critical for establishing a strong cardholder relationship. An “early-month” onboard program that reinforces the value proposition of the credit card and encourages use helps develop the type of spending habits needed to become top of wallet.

Email is a cost-effective channel that can easily be used to reach new cardholders. Here’s an example of an email onboarding calender for the first 45 days after someone opens a credit card account:

2. Prioritize Existing Cardholders Based on Potential for Incremental Spend

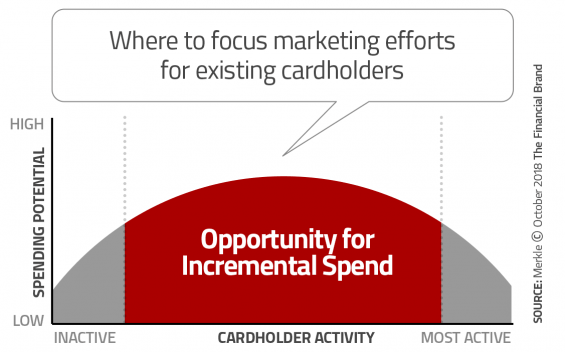

It’s tempting for banks and credit unions to focus offers on their most active and valuable cardholders. In reality, however, it is often difficult to generate incremental spend from this segment, especially if an institution’s credit card has the largest share of wallet. Instead, work to retain this segment through constant recognition and priority service.

On the flip side, it is very challenging to re-activate cardholders who have not used their credit card for 60 days or more. A proactive retention program will help prevent cardholders from getting to this point. The program should identify cardholders at risk of becoming inactive and reach out to them. The most sophisticated approach is to use a predictive model based on data patterns of cardholders who have become inactive.

As an alternative, card issuers can look for changes in spend behavior. For example, a cardholder whose transaction activity declines substantially would be a prime target for a retention program. Changes in a cardholder’s credit file could also trigger a need for early intervention, especially if the activity indicates a new account being opened.

After setting aside active and inactive cardholders, you are left with an audience that can be prioritized. Lifetime value models built using transaction and credit bureau data can quantify the potential for incremental spend.

In the absence of such a model, marketers can also utilize simpler recency, frequency, monetary (RFM) scoring techniques to rank cardholders and determine where to draw the cut-off for marketing investment. Typically, marketers find the greatest potential with the majority of cardholders who fall between the bottom 25% and the top 25% in terms of cardholder activity.

3. Align Offers to Encourage Desired Behavior

Once the target audience is defined, the question becomes “How to unlock the cardholder potential?” Promotional offers can be very effective if the strategy aligns with the desired change in cardholder behavior.

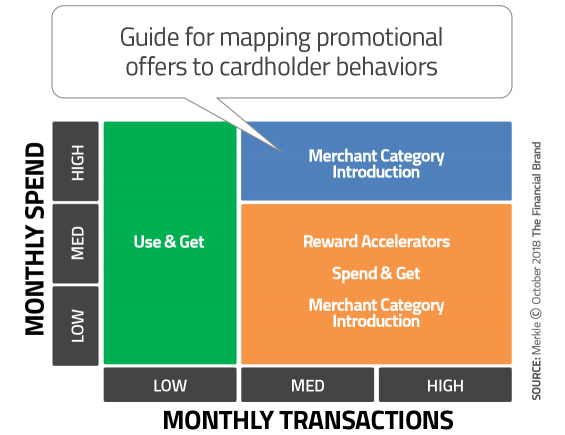

The first step is to segment the target audience based on number of transactions and total spend. The second step is to map the segment with the appropriate offer type.

Use and Get Offers are best suited for cardholders that have low transaction activity. The goal is to encourage repeat usage, preferably in high-volume purchase categories such as gas, groceries, and dining. For example, “Get a promotional rate of 0% if you use your card five times or more to purchase gas or groceries.”

Spend and Get Offers are appropriate for cardholders that have frequent, low-ticket purchases or who may be splitting spend across multiple cards. The goal is to get a higher share of wallet. For example, “Spend $3,000 or more over the next 30 days and get a $25 statement credit.”

Reward Accelerators are effective for cardholders who are vested in your loyalty program. Bonus points or cash-back incentives encourage more frequent purchases and higher spend. For example, “Earn three times the points for all grocery purchases in the next 30 days,” or “Spend $3,000 or more and get 5% cash back.”

Merchant Category Offers are intended for cardholders who have low-to-no spend in a specific merchant category. For example, “Use your card to pay for utilities and get two times the points,” or “Get 10,000 bonus miles for all travel purchases made in the next 90 days.”

Establish a testing plan that incorporates at least two offers within a category to understand what resonates with your cardholders. If your processing platform allows, consider testing an opt-in offer where cardholders enroll in a promotion. This is a great way to control offer costs by removing passively engaged cardholders.

Mining transactional data, segmenting cardholders, and differentiating offers requires a lot of thought and planning. Nevertheless, this is a much more effective approach compared to “one-size-fits-all” marketing communications. Start off simply to achieve some quick wins, and then use the insights gained to optimize results.