Consumers’ frustrations with their primary financial institutions range from simple grumbles and mild distrust to outright rage. But how annoyed does a consumer have to be before they’ll leave? And what are the trigger points?

In its Retail Banking Vulnerability Study, consulting firm cg42 suggests that major retail banking brands face greater risks than ever that consumers will leave them. The firm estimates, based on an analysis of a large consumer survey, that 11% of major bank consumers could walk.

People’s top five frustrations with their banking providers include:

- Acting in dishonest, unethical or illegal ways

- Constantly slapping them with nickel and dime fees

- Failing to offer competitive rates and pricing

- Data breaches or exposing personal/account data

- Hitting them with overdraft charges

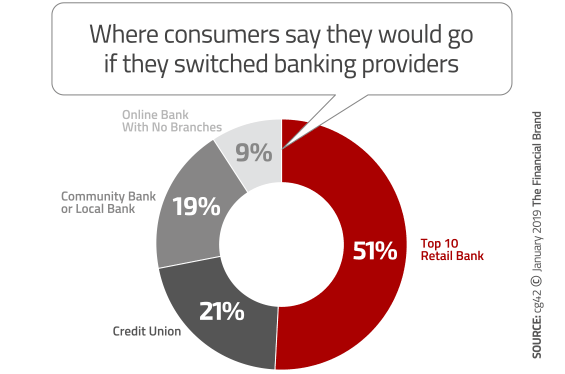

Although more than half of those consumers would simply switch to another large retail bank, almost as many say they would consider other choices. Nearly one in ten would be willing to go with an online bank with no branches.

The number of potential defectors represent $344 billion in retail deposits and $16 billion in revenue, according to cg42. The firm notes that these figures have grown over substantially in recent years, indicating that more consumers are ready to move. The advent of online-only players and the possibility of non-traditional competitors like Amazon, has convinced many consumers that it’s easier to shift their main banking relationships than it was in years past.

The Most Vulnerable Big Banks

The cg42 study ranked large institutions’ relative risk of losing business. Among ten major banks studied by cg42, an average of 21% of their customers were at risk of switching within the next 12 months.

Bank of America, ranked at greatest risk, has been in that spot in two of the three previous surveys, and has always been among the top three. The firm’s analysis of BofA customer frustrations indicates that overdraft fees led three out of five categories of dissatisfaction, including “most-shared complaints.”

Wells Fargo, continually buffeted in recent years by news of unethical or fraudulent behavior, ranked second in the study, moving up from fourth place since the 2015 report. For Wells, engagement in questionable activities topped four out of five categories, underscoring the price of reputation risk.

After BofA and Wells Fargo came PNC, BB&T, U.S. Bank, SunTrust, Citibank, TD Bank, Capital One, and then Chase.

In 2015, JPMorgan Chase ranked at the second-highest risk of losing customers, but they improved markedly, dropping all the way down to the tenth spot.

The report also reviewed what had improved Chase’s ranking such that it was the least vulnerable institution among the ten. According to the report, Chase is “outperforming its peers on frustrations related to ease of use and customer service.” The firm suggests investment in the right tools brought about this turnaround.

Americans Want to See New Blood in the Banking Industry

The cg42 study also probed consumers about popular big tech brands and their potential to disrupt the banking sector. Would people be willing to bank with Silicon Valley giants like Google, Facebook or Apple? All generations are receptive to the idea generally. Amazon in particular is a major threat to traditional banks and credit unions. Millennials represent traditional institutions’ greatest risk, with one in four willing to bank with Amazon.

| Which company people would switch to if they offered banking services |

Millennials | Generation X | Baby Boomers |

|---|---|---|---|

| Amazon | 25% | 15% | 5% |

| PayPal | 21% | 15% | 4% |

| Apple | 21% | 12% | 4% |

| 20% | 12% | 2% | |

| 10% | 6% | 1% |

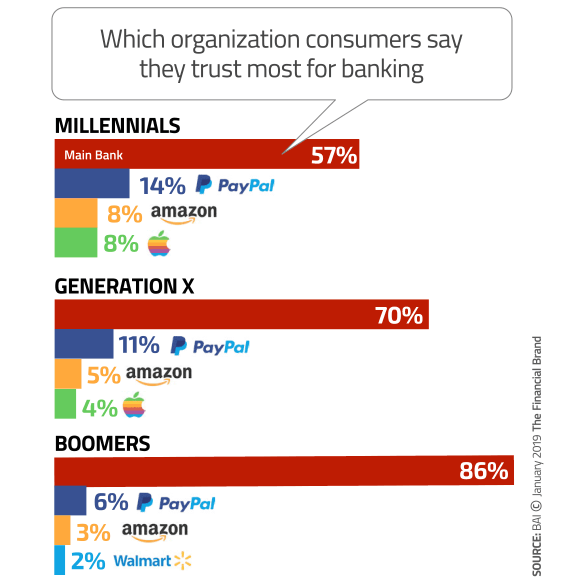

When asked by BAI who they would most trust to handle their financial products and services, these figures shift downward — likely the result of how the study was administered and survey questions worded — but the outcome is still basically the same: traditional institutions face a significant competitive threat from outside challenger brands.

A major portion of consumers overall trust banks — Gen X and Boomers especially. However, the fact that 43% of Millennials would put their greatest trust in organizations other than banks bolsters the threats outlined in the cg42 study, further supporting the argument that loyalty and inertia are loosening their grip on today’s financial consumer.

BAI’s finding isn’t unique. In its latest international Customer Loyalty in Retail Banking Report, Bain & Co. found that 29% of respondents trust at least one tech company more than they trust their primary bank. Even more stunning, more than half (54%) of respondents trust at least one tech company more than they trust banks in general.

This follows an earlier Bain survey indicating that two out of ever three Amazon Prime consumers would be willing to try out a free online bank account offered by Amazon. Among Amazon users who don’t have Prime service, 43% would be willing to give an Amazon banking service a try. Even 37% of consumers who don’t use Amazon would try a free online account from them. (Like every other study, those who favored Amazon banking in Bain’s Amazon research tended to be younger consumers.)

According to Bain, tech giants have “already reset customer expectations for what a good experience feels like.”

“The experience of Alibaba in China proves that a technology firm can succeed quickly on a large scale in financial services,” observes the authors of Bain’s report. “In just four years, Alibaba’s repository for leftover cash from online spending became the largest money market fund in the world, through its Ant Financial Unit.”

Better Digital Service: A Major Reason to Switch

It’s not just frustration that can coax consumers to move to a new banking provider. An ABA survey of consumers found that seven out of ten use a mobile device to manage their bank account at least monthly. Of those who use online access and mobile apps, the opinion of their current institution’s offering is generally positive: 32% rated it excellent; 34% very good; and 27% good. Only 6% rated services as fair or poor.

Yet the research also indicates that the burgeoning cadre of mobile users provides a fertile pool of potential switchers, particularly those with killer digital services. One in six respondents in the study said that they would change institutions for “a better digital experience.”

More specifically, consumers outlined a variety of services that they consider valuable enough to move for. One in six (17%) said they would make the switch for services like mobile payments and bill pay. One in seven would seek a new banking provider that offered budgeting tools. Roughly one in ten are particularly interested in things like online loan applications and integrated voice/digital assistants such as Alexa.

When Too Much Digital and Self-Service Is a Bad Thing

Everyone appear to really want the full menu, and not just an all-digital choice all the time… or at least the feeling of it. This is one of the findings coming out of research fielded by CCG Catalyst. Their study was based on in-depth interviews with both consumers and businesses.

Paul Schaus, CEO at the CCG Catalyst consulting firm, says that the industry needs to understand that there has been a subtle rethinking of what an institution is, in the minds of both consumers and businesses. Once there were “products” on one hand and “service” on the other, the latter reflecting the human element, how well the bank’s officers and staff took care of people. Schaus contends that the growing role of digital means that more of what the public sees of a bank or credit union is its self-service channels.

Schaus contends that when bankers speak about poor service, they are talking about unsatisfactory human contact, but that when consumers speak of service they are often referring as much to poor product design or performance. After all, for many that is what their bank is.

If a financial institution’s mobile app isn’t fresh and friendly with the latest smart phones, people will feel the provider’s service is poor, even though they aren’t interacting with staff at all. The survey found that 23% of consumers and businesses were frustrated by institutions’ self-service channels, both online and in-branch.

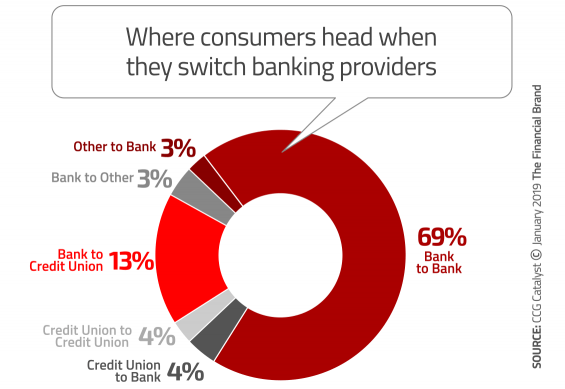

Where self-service isn’t sufficient, Schaus says, consumers and businesses continue to favor branches, which still tends to favor larger, national players. Schaus points out that many of those changing institutions are moving from one large bank to another — typically BofA, Wells, Chase, and Citi.

CCG Catalyst’s study found that when people move, they usually move to a bank. Only one in five respondents chose a credit union when making the switch.

There’s a warning sign in CCG Catalyst’s study: 28% of consumers and 27% of businesses felt they had “no relationship” with their provider and were “treated like just another number.” The more someone uses mobile and online from a larger institution, the greater their disconnect, the study found.

In an age where “personalization” and all that it implies is possible with adept analysis and use of data, it seems risky for institutions to be leaving close to a third of both consumers and businesses feeling like they’re out in the cold. Especially when players like Amazon and Google seem to know what we’ll do before we do it, and what we want before we want it.