The benefits of strategic planning are well documented. Done well, a strategic planning process allows organizations to set a direction, providing objectives and goals that are used for assessing progress across the organization. Strategic planning also allows organizations to be proactive, by better understanding opportunities and threats that may be on the horizon. Being proactive can improve differentiation versus the competition and enable the efficient deployment of resources. Finally, a strategic plan increases operational efficiency, helps to increase market share and profitability, and makes the overall business more sustainable in the long term.

Unfortunately, just having a strategic plan is not enough.

At many financial institutions, the strategic planning process fails because the planning is done simply to say that bank or credit union has a plan. If an organization is not committed to implementing the strategy, the planning effort may turn into a demoralizing factor .

Other reasons may doom a strategic plan. A plan may fail if the right people are not involved in the process. Or if the effort is just a minor iteration of past annual efforts. Or if there is a complete naivety about marketplace conditions including opportunities, threats and changes that could impact the institution’s future viability.

However, the biggest planning issue in the financial services industry doesn’t usually center on inadequate involvement in the process, lack of goals and objectives, inability to assess the marketplace realities, or even a lack of commitment.

The biggest barrier is the inability of many banks and credit unions to change.

The best planning efforts will never drive positive outcomes if institutions don’t commit to, and invest in, strategies that will change the way they do business. This shortcoming has plagued the industry for several decades. The impact of not adjusting to market realities has been camouflaged by positive financial results (in most cases).

It is time to commit to changing the entire strategic planning process and taking steps that support your plan … or stop wasting your institution’s time and money on a process that will never produce the desired results. The demise of those organizations that are just going through the motions of strategic planning may not occur in the next 2-3 years, but the marketplace will soon reward the banks and credit unions that have prepared for a new banking era.

Talk is Cheap

Every year, the Digital Banking Report does research on the Trends and Predictions for the upcoming year. For the past few years, the top trends mirrored the top strategic objectives mentioned by financial services organizations worldwide. The top five areas that almost every organization agreed upon as being important for success (in slightly different orders each year) were:

- Improving the customer journey

- Applying data and advanced analytics

- Digitizing the organization

- Building better payment solutions

- Reducing operating costs

These are all valid objectives, with the prioritization of these objectives being different at every organization. The problem is that in other research done by the Digital Banking Report, and virtually every consultancy, financial industry influencer, and even financial organization, the progress on any of these objectives is far less than the potential. In many cases, there is even evidence that organizations will say they are moving forward on an objective, but investment (human and financial) does not reflect this ‘commitment’.

In other words, many organizations are not backing up their strategic plans with definitive action. They are not embracing disruption of “banking as usual.” This is a recipe for failure — and reinforces that the strategic planning process at many organizations must change immediately.

CX in Banking is Terrible

Despite being the primary stated strategic objective for most financial services organizations, most customer journeys have not changed much since the early 1980s. This is not because the consumer hasn’t changed — most banks and credit unions have not adjusted to market realities.

More than 50% of banking transactions are now conducted through digital channels. This not only impacts how a consumer researches and selects their financial institution, but also how transactions are conducted. While consumers initially did only rudimentary transactions via online banking or a mobile device, more involved engagement is now desired. This is the result of consumers being exposed to non-banking tech organizations (Amazon, Google, Facebook, etc.) that have simplified everything from purchasing products to digitizing every component of a travel itinerary.

Consumers want simple ways to interact with their financial institution that will be contextual to their personalized needs. In the majority of cases. they do not want to visit a branch unless absolutely necessary. They want financial solutions that are proactive and reflect real-time activities and needs, not pre-scheduled product campaign messages that provide minimal value.

Financial organizations of all sizes have the ability to use data and advanced analytics to proactively engage with consumers in ways that will save them time and money. In return for this enhanced value proposition, consumer will be more satisfied, more loyal and will deepen their relationship. Most institutions must re-calibrate how they engage with their customers and members to reach the potential that strategic planning is meant to achieve.

Read More: Top 7 Customer Experience Trends in Banking

From ‘Great Reports’ to Personalized Engagement

Virtually every strategic plan goal or objective requires the application of data and advanced analytics to maximize success. No other industry has access to more individual transaction, behavior, and demographic data than banking. Unfortunately, while most banks and credit unions have data organized to see product and organizational metrics, significantly fewer have applied this insight in a way that can differentiate the organization from a customer or member perspective.

With the influx of new competitors that are offering better financial solutions by combining data, analytics and digital technology, traditional financial institutions need to prioritize the entire data and analytic function. As with the other strategic planning objectives, knowing that this must be done has not resulted in a significant change in investment or talent deployment.

According to the Digital Banking Report, investment in machine learning and artificial intelligence initiatives remains focused on risk and fraud elimination as opposed to improved consumer engagement. These are iterative improvements in the use of data and analytics as opposed to the transformational improvements needed.

If there is one priority that most banks and credit unions must commit to in order to make the strategic planning process impactful, improving the collection, cleansing and deployment of data is probably number one.

Read More: AI’s Real Impact on Banking: The Critical Importance of Human Skills

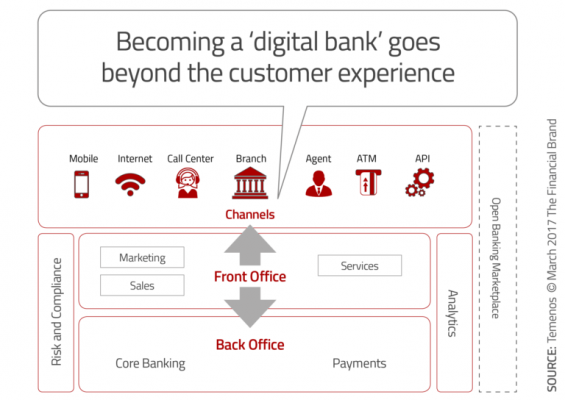

Being Digital vs. Digital Banking

It is much easier to deploy digital solutions than to be a digital organization. “Being digital” requires a rethinking of entire processes from the core of the organization as opposed to turning paper into PDFs. Unfortunately, most organizations either don’t understand the difference, or are unable to move away from traditional banking enough to think like a technology organization.

An excellent example of “being digital” is when mBank in Poland wanted to build a digital lending solution. As opposed to simply converting all of the lending paperwork into digital forms, management completely rethought the way digital technology, customer data, and revised back-office could work together to reduce friction and increase loan customers.

mBank put all involved departments from the bank in one room, at one time, with the goal of offering the majority of their customers a loan within 15-seconds. The team had to rethink application processes, credit scoring, risk, fraud, approval criteria, up-selling processes and deployment of mobile offers so that over 75% of their customers had a standing offer for a small personal loan delivered on their mobile device.

The result was not only an increase in loan volume, but increased customer satisfaction and a cultural shift within the organization that there was a commitment to becoming a digital bank. The most enlightened banks understand that to become truly digital they need to update their systems back to front. This will fulfill the business need for product agility, where banks and credit unions can offer the right products, over the right channel, and at the right time.

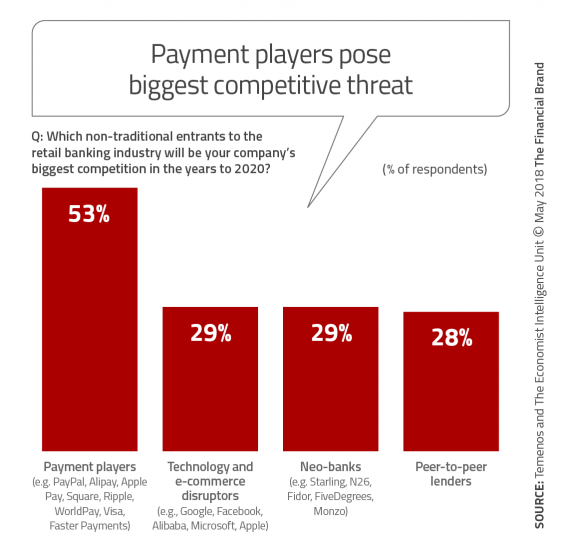

Payments Under Attack

One of the first banking services to be impacted by fintech firms and big tech organizations was payments. From merchant services (impacted by Square, Paypal, etc.) to payment transactions (Apple Pay, Google Pay), to P2P (Venmo, Facebook, Square Cash), every part of the payment product line has moved away from traditional financial organizations. In a world where payment transactions represent some of the most robust insights about a consumer, this shift is not favorable.

“Organizations are increasing investment in payments solutions to improve the customer experience and to support new solutions, focusing the most on P2P payments, mobile wallets and debit cards,” according to Fiserv. “Organizations believe P2P payments and mobile wallets are increasing in importance compared to other payment solutions, with most organizations believing real-time payments and P2P provide significant opportunities in the future.”

Regardless of which app rises to dominance, as the boundaries between point-of-sale and digital commerce become increasingly blurred, the ultimate winner in the race to make payments a more seamless, less time-consuming experience will be the consumer – but only if organizations act on the strategic planning goals that have been set around this important product set.

Shift from Cost Reduction to Revenue Enhancement

Almost every strategic plan in banking includes a major section around reducing costs. The challenge is, how far can costs be reduced without impacting the customer experience or limiting investment in important strategic initiatives?

Today’s consumer is wiser than ever around statements made by banks and credit unions regarding “product improvements” and “simple and easy”. They have come to expect that these statement usually are nothing more than ‘lipstick on the cost reduction pig’ presented by financial institutions as ‘benefits’ to the consumer. That is why ATMs were introduced and why mobile banking was promoted so heavily by banks and credit unions – to reduce costs. Consumers want to know, “What’s In It For Me?”

Instead of focusing on costs, organizations must look at ways to generate revenue as well as value for the consumer. Many financial institutions are only recently adjusting to a world in which insight can create value, while big tech firms have been living in this world for years. These firms are leveraging usage intelligence, feature-based packaging, and flexible consumption as part of their monetization strategies to use insight to generate more revenue.

Armed with new strategic objectives and initiatives around applying data and insights, banks and credit unions can begin to use digital technology not just to save money, but to generate new value for consumers and new revenue for themselves.

Moving From Annual to Real-Time Strategic Planning

Fundamental changes in the financial services industry provide both challenges and opportunities to strategic planners. There is an increasing need to build agility into the strategic planning and execution process, if banks and credit unions want to thrive in the digital age.

This requires modifications to the existing planning process. Bringing agility into strategic planning requires accurate forecasting followed by accelerated decision making through a lean process. Swift execution through strong collaboration of stakeholders and linked incentives beyond annual target setting is also required.

Read More: The Qualities of Digital Banking Champions

Digital tools and advanced technologies can be valuable facilitators of agility. Their benefits range from strategic analysis, decision making to multichannel execution. Ultimately, a continuous strategy planning process needs to be built which can be executed on demand.