Almost 9 out of 10 financial institutions believe that digital transformation will fundamentally change the services they offer and completely reboot the industry’s competitive landscape. Despite this overwhelming belief, most organizations lack a digital strategy. This sets up a dilemma that can impact the ability to eliminate threats and take advantages of future opportunities.

The solution is for banks and credit unions to look within their organizations. They need to understand their current competitive position, strengths and weaknesses, internal culture and capabilities. Many organizations will need to consider how they can restructure their distribution models, improve their value proposition, and provide consumer-centric digital solutions that will improve their satisfaction and increase growth.

Digital transformation must occur as a comprehensive, enterprise-wide strategy — an effort led from the very top, rather than uncoordinated, one-off initiatives.

Digital transformation must occur as a comprehensive, enterprise-wide strategy — an effort led from the very top, rather than uncoordinated, one-off initiatives.

The need to respond to channel shift, product opportunities, and digital transformation trends is addressed in the 10th annual Innovation in Retail Banking report, sponsored by Efma and Infosys Finacle and published by Digital Banking Report. The report includes a review of the previous nine years of the publication, providing a snapshot of the marketplace and innovation trends through the years. The report also provides analysis regarding the preparedness of organizations for a new banking ecosystem.

( Free Download: Innovation in Retail Banking 2018 )

Open Banking Seen As Biggest Technology Trend

As the banking industry is in the midst of massive digital transformation, organizations are increasingly using automation to improve efficiency and reduce costs. While the economics are enticing, the real value of intelligent automation may actually be as a driver of increased revenue growth and enhanced customer satisfaction.

Unfortunately, most financial institutions are still only scratching the surface of potential benefits of digitization beyond cost savings. While many have implemented some advanced technologies, most are simply moving forward on an iterative basis, as opposed to embracing enthusiastically any technology to its optimal potential.

A great example is with AI and machine learning. Institutions continue to improve their use of these tools in the areas of risk and fraud management (traditional areas of emphasis), but the tools see far less application to improving customer targeting and communication. The same is true with Open APIs, where most institutions are using these opportunities in legacy fashion as opposed to taking advantage of an expanded banking ecosystem with broader financial services … or even non-financial experiences.

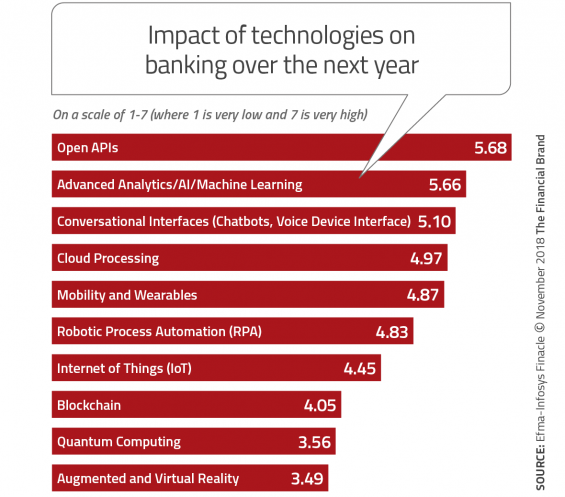

When the report’s surveyors asked financial services organizations worldwide about the impact of advanced technologies in the next 12 months, Open APIs were considered to have the largest potential impact. (They scored 5.68 on a 7-point scale.) Obviously, this scoring is positively impacted by institutions in the European countries where Open Banking is already being regulated. However, we saw Open APIs as being scored highly by all banks in all regions, reflecting the forward view of most respondents.

While advanced analytics/AI/machine learning and conversational interfaces were the next most mentioned technologies expected to have an impact, other research done by the Digital Banking Report has found that commitment to these technologies is much more aspirational than evidenced in current use. In fact, the relatively slow adoption of advanced analytics is one of the major concerns regarding the ability for many financial institutions to compete in the future.

Finally, note that, despite significant industry discussions around the potential of blockchain technology, the anticipated impact of blockchain in retail banking over the next year is far lower than that expected from most other advanced technologies.

Financial Institutions Not ‘Data Ready’

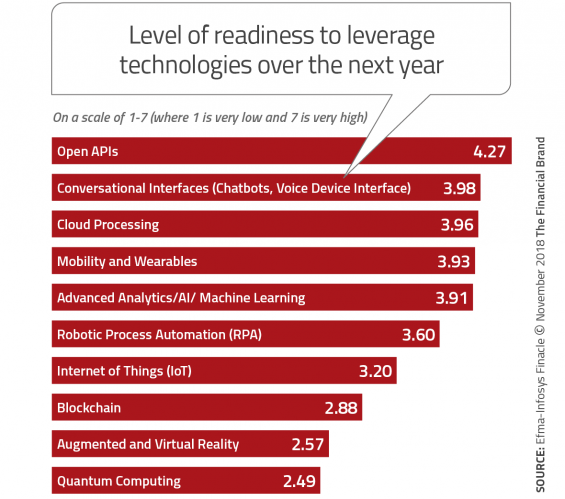

In spite of the high rankings for the impact of advanced technologies, none of the technology options had a high level of readiness on the 7-point scale. The good news is that financial institutions globally believed they were in the best position with Open APIs, conversational interfaces, cloud processing and mobility/wearables.

Of ongoing concern is the relatively low score for the ability to leverage advanced analytics and machine learning. This is an ongoing theme throughout the research, which can inhibit all other technology advancements and innovation efforts.

Product Revenues At Risk

When asked what banking product lines will be most important to organizations in 2022, payments, mobile wallets and lending topped the list. This should be a red flag for organizations who also rank fintech and big tech firms as the most formidable competition, since these are the three areas where non-traditional financial institutions already excel or could overtake traditional banks from a customer experience perspective.

Should financial institutions begin to look for new revenue sources as they become less competitive in the product areas of payments, mobile wallets, digital lending and cards? Or, is a better strategy to reposition organizations as platform participants, offering both internally built and external offerings to satisfy consumer needs? Better yet, the best strategy may be to eliminate product silos and to integrate products into a broader ecosystem offering.

Digital Distribution Takes Center Stage

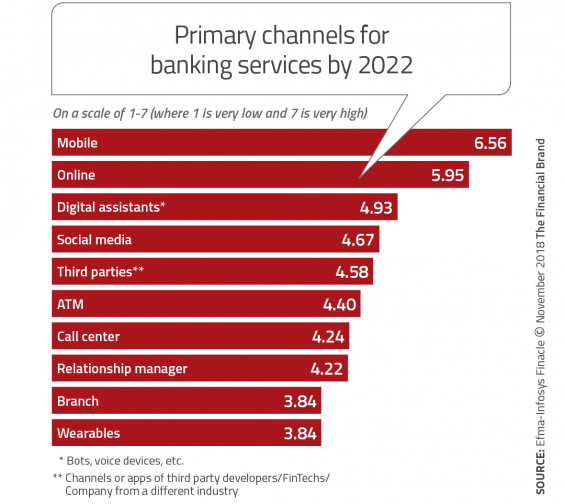

When banking organizations were asked to determine what channels will be the most important in 2022, an overwhelming majority of organizations saw mobile and online being the primary distribution channels. After the current digital channels, it is surprising that digital assistants (bots and voice devices) were seen as the third most likely channel, with social media close behind. The impact of open banking can be seen by the fact that third-party distribution was seen as a more important channel than ATMs and call centers.

In a very dramatic view into the future, banking organizations worldwide see branches as the second-least-likely delivery channel in the future, with relationship managers also being rated very low, Interestingly, this year’s survey respondents did not have much “digital love” for wearables.

Preparing for the Future

Overwhelmingly, financial executives who responded to this year’s Innovation in Retail Banking survey believed that the future of retail banking will be most impacted by “changing customer behavior and demands.” In addition, technology and digital changes will begin to have a bigger impact on strategies than regulatory changes. The challenge will be to respond quickly enough and strongly enough to make a ripple in the increasingly crowded financial services ocean.

The increasing loss of important components of traditional banking product lines and the shifting distribution of services will increase the importance of agility at all financial institutions. The importance of data and advanced analytics will also increase as the need for building improved customer experiences surpasses the need to cut costs as a path to success.