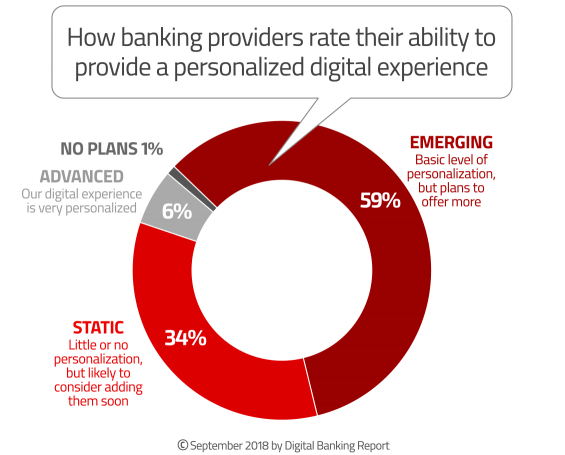

Banks and credit unions are increasingly adopting a more personalized approach to connecting with consumers across all media channels, according to research from the Digital Banking Report. To stay ahead of the competition, financial services companies are making efforts to build human connections with consumers and trying to build a more emotional style of consumer engagement.

This is impacting all customer-facing components of the retail banking organization, from marketing to product development, to back-office operations, channel management and innovation. It is also changing how data and advanced analytics are used to create more robust views of each customer and member, with the objective being to replicate the targeting and engagement power of tech giants like Facebook, Google and Amazon.

“Facebook and Google are the gatekeepers of online targeted advertising,” says eConsultancy. “Commonly referred to as a duopoly, because of their hold on digital advertising and the media landscape, they accounted for approximately 63.8% of all online ad expenditure in 2017, up from 57.5% in 2016 and 47.1% in 2012.” At the same time, Amazon is becoming a third force in personalized digital advertising, generating billions in digital ad revenue.

This is placing the process of customer experience management at the forefront of most financial services organizations’ strategies. As customer expectations increase, getting to know consumer needs and behaviors has become critical. Competing on price or product offering no longer suffices – the ability to personalize engagement, in real time, is the bar being set.

As financial institutions collect and apply data, there is also the opportunity to generate insight into sentiment towards a bank or credit union brand. This feedback allows financial institutions to improve their offering and retain loyalty towards the institution.

Read More: The Psychology of Personalization In Banking

Changes in Targeting & Marketing Strategies

As availability of internal and external data grows greater than ever, there are new opportunities for targeting on the individual level, leveraging more granular communications. With the increase in digital channels, institutions have the ability to personalize both the audiences targeted and the messages communicated.

The expansion of digital capabilities and channels puts stress on financial marketers, however, trying to manage this increased complexity. But, the potential of 5G, artificial intelligence (AI), connected devices, and voice search are considered worth the investment by most financial institutions.

The combination of mobile, artificial intelligence and machine learning will enable personalized experiences at scale. Further, while still at the infancy stage, the growth of voice-activated marketing is expected to create even more compelling experiences that combine behavioral data with contextual data.

Attaining The Single View of Customers

As consumers increasingly accept what can be achieved by the tech giants as the standard that all providers must meet, it is more important than ever for financial institutions to work towards a single customer view as opposed to working with segments or mass audiences. There are at least five reasons for having a singular customer view:

1. Identifying valuable customers and building relationships. Increasing what’s known about each customer or member allows for the movement from “selling” to “advising” and provides incentive to develop a long-tern perspective that can enhance loyalty. This allows the movement from individual campaign performance to customer relationship value growth.

2. Creating personalized content. Understanding the individual consumer is most powerful when creating personalized marketing communications: Because of the bar set by Google, Facebook, Amazon and others, the consumer expectation is that all marketing communications will be relevant, timely and specific to activity or behaviors that indicate need. This leads to more “pull” marketing than traditional “push” communications.

3. Responding to consumer changes. The customer journey is no longer consistent between consumers. People research, shop and purchase financial services differently than they used to —and differently than others who otherwise may look similar. Behaviors change based on where consumers are at any point in time, and the device(s) they prefer to use. With the single customer view, financial marketers can monitor changes in needs, behaviors and preferences, adapting strategies accordingly.

4. Developing proactive communication. In the past, financial services organizations only provided content reflecting what had already occurred. Having a single customer view allows banks and credit unions to be proactive. Now they can advise consumers regarding future needs. In the end, the more we understand consumer needs on a singular basis, the more we can proactively serve them.

5. Improving regulatory compliance. New data privacy regulations may make the single customer view a requirement, with the consumer having complete control over their identity and how we use insights. This will make it crucial for marketers to have a single customer view and to keep identity permissions in place.

That moving to a single customer view is important is acknowledged widely now — but achieving this perspective is anything but easy. Data silos, lack of integration of advanced analytics and difficulty in finding needed talent make it tough to move from great internal reporting to meaningful customer experiences.

The Future of Engagement

The days of mass marketing where the financial institution drove a single message to consumers is over, replaced by personalized products, offers and experiences where the consumer increasingly controls both the message and the channel. The future is 1:1 marketing where the message is delivered in real-time as a solution to an immediate need.

In a digital world, there is an increasing amount of people talking to people as opposed to banks and credit unions talking to people. The role of referrals and recommendations increases as does the interaction across social media channels. In each case, the consumer is looking for “people like them” who will help them along their customer journey. Organizations that can communicate to these “communities” will benefit.

Cutting through the marketing noise will become more difficult than ever, with the importance of artificial intelligence, customer journey mapping and new marketing tools like the 10-second video ad format replacing previous marketing strategies. “Demonstrating relevancy, improving personalization and understanding who your customer is will increasingly feature on the agenda for marketing,” says eConsultancy, “and, if balanced with respect for privacy and minimizing the perception of intrusiveness, will open opportunities for more dynamic conversations with consumers.”

While technology, techniques and channels may change, the focus should remain on brand purpose and understanding the consumer. Rewards will be earned by those that help each consumer simplify their financial life on a personalized basis.

Read More: 6 Insights To Get Your Digital Engagement Strategy Right