It comes as no surprise that consumers across the globe are increasingly using their mobile devices as a way to research, shop, bank and pay. The reason for this trend is due to increased number of smartphone owners, combined by the benefits of convenience, accessibility, security and continued increase in functionality.

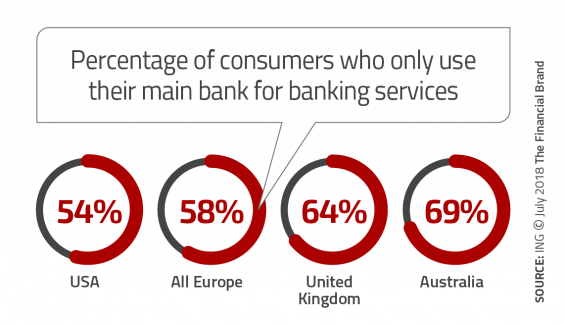

According to the 2018 ING International Mobile Banking Survey, despite these benefits, the majority of consumers in most regions say they have continued to use their current banking provider. The shares who only use their primary institution for a range of money services are the highest in Luxembourg (76%) and Belgium (73%), and the lowest in Turkey (50%), Germany (54%) and Poland (54%). Reliance on a traditional financial institution is 54% in the US, 58% in Europe on average, 64% in the UK and 69% in Australia.

“Natural inertia no doubt plays into incumbent providers’ hands,” states the report. Yet “challengers” − whether they be new-style banking providers or financial technology companies – have gained ground in recent years and may continue to do so.

For those consumers who said they did use organizations other than their traditional provider, the most common reason was for money transfer. In Europe overall, 21% of consumers who used outside organizations did so for money transfer services. Similar percentages were seen in the UK (16%), Australia (16%) and the US (18%).

Peer-to-peer payments, often on a mobile app, were the second most mentioned activity done through organizations beyond a consumer’s traditional provider. The use of a challenger organization for P2P transactions was highest in the US (18%), followed by 15% of consumers in Europe overall, 11% of consumers in the UK and 9% in Australia.

When ING asked why people went beyond their traditional financial institution, 16% cited “being able to do payments whenever I want” and 14% said “to increase the convenience.”

Mobile Devices Top Choice for Daily Account Checking

Before online and mobile banking, consumers used their paper check registers to keep track of activity and relied on paper statements, phone agents or the branch teller to validate their calculations. In fact, the vast majority of end-of-month branch activity was customers depositing their monthly check and the branch updating account balances.

With the advent of both online and mobile banking along with digital statements, the consumer no longer needs to wait for the mail to arrive or to call their financial institution to verify monthly, weekly or daily balances. Instead, the majority of consumers now use their mobile device for activity verification.

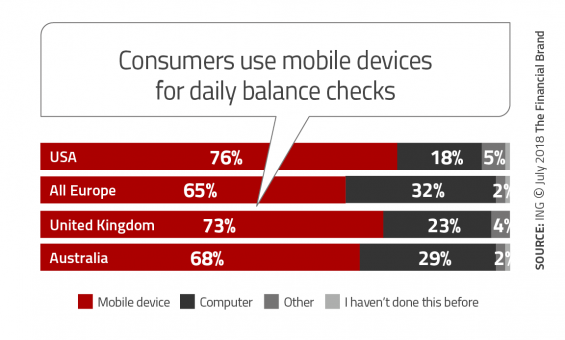

According to ING, an overwhelming percentage of consumers use their mobile device to check balances and verify transactions. And this number continues to rise as more organizations are able to provide real-time activity updates. The reliance on mobile banking for balance verification underlies the potential to use this habit to build broader engagement. Mobile banking should be increasingly used for proactive, personalized service recommendations, content delivery and other mobile money management tools.

In-Store and Online Payment Habits Differ

Consumer decisions on how to pay differs between in-store and online shopping. According to the ING research, 75% of US consumers shop online at least once a month with a computer, tablet or mobile phone. This frequency compares to 78% of consumers in the UK, 55% in Australia and 67% of consumers across all of Europe. The percentage of people shopping online differs across countries due to cultures and availability of options, but is increasing in all regions.

The way consumers pay online differs between countries surveyed. Availability of options, convenience and security all impacted the choice made. For Europe overall, credit and debit cards, whether details are stored online or re-entered in each transaction, accounted for 42% of online purchases. PayPal was next, with 32%. In the US, stored and manually entered cards represented 62% of online payments, with 22% of consumers using PayPal.

Another option — ‘Local payment methods’ — refers to a wide range of digital ways to pay, including apps such as Netherlands-based Twyp or European solution Boon, but also other options such as interbank solution iDeal. These type of options are available in European countries, but are not available in the US or Australia.

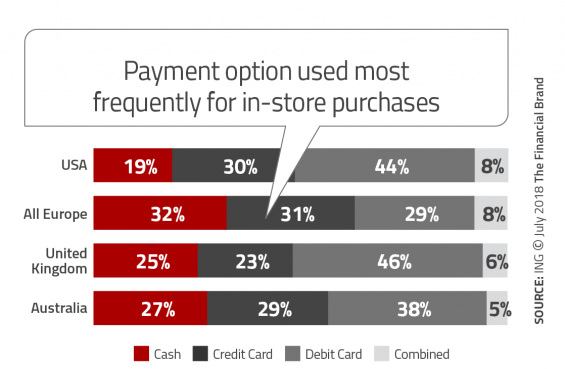

![]() As would be expected, the prominence of payment options used differed when consumers were asked about their in-store payments. In the US, only 19% of in-store payments were made in cash, compared to 32% in Europe overall, 25% in the UK and 27% in Australia. Alternatively, debit card payments were the most prominent in the UK (46%) and the US (44%), with the blended average across all of Europe showing a preference of credit card use for in-store purchases.

As would be expected, the prominence of payment options used differed when consumers were asked about their in-store payments. In the US, only 19% of in-store payments were made in cash, compared to 32% in Europe overall, 25% in the UK and 27% in Australia. Alternatively, debit card payments were the most prominent in the UK (46%) and the US (44%), with the blended average across all of Europe showing a preference of credit card use for in-store purchases.

ING payments analyst Karolina Derwisz said, “Taking into account the pace of development of in-store payment networks, the share of physical cash remains relatively high.”

Detractors to Digital Payments Remain

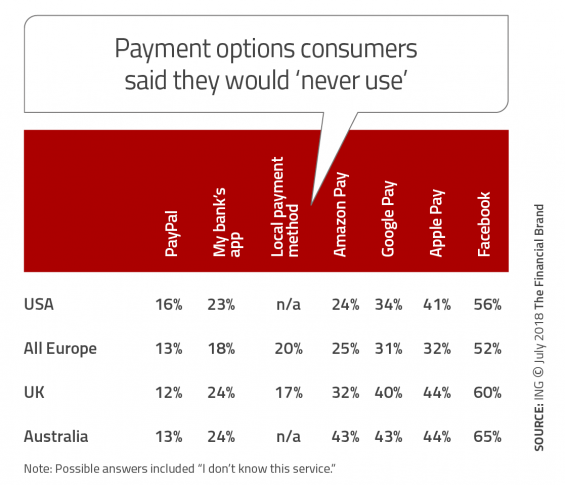

Despite all of the industry talk of the proliferation of digital payments, some consumers aren’t convinced of the benefits of this payment option. The ING research found that there is still a measurable percentage of consumers who say they would ‘never use’ a digital payment solution.

Across all major markets, PayPal has the lowest negative perception overall. Only 13% in Europe and Australia say they would ‘never use’ PayPal, with the negative perception of PayPal being slightly higher in the US (16%). Of concern for banking organizations, PayPal is a more acceptable payment option than current bank alternatives.

The least popular digital payment alternative is Facebook. Across all regions, Facebook had a greater negative perception than any other option, with more than 50% of consumers in every market saying they would ‘never use’ Facebook to make payments. As mentioned, neither the US nor Australia have a local payment option.

When asked why they did not want to use the digital options, 44% said “I always have my card or cash with me anyway,” 42% do not see any added value compared to the payment methods they already use, 36% had concerns about data collection and storage, and 27% said the method is “unsafe”. Even among those who would ‘never use’ a digital option, only 8% said the option was not easy and only 5% thought digital options were too expensive.

Read More: Consumers Threaten to Bail If Banking Providers Can’t Improve Digital CX

Consumers Want Digital Alerts to Help Manage Money

Not enough attention is given to the potential power of alerts and notifications as it related to building engagement, helping consumers proactively manage their money and increasing satisfaction. When ING asked about automated reminders or notifications sent via a mobile device or computer, it is clear the consumer would appreciate more communication. Research showed that consumers want more proactive ways to feel in control of their money.

Not enough attention is given to the potential power of alerts and notifications as it related to building engagement, helping consumers proactively manage their money and increasing satisfaction. When ING asked about automated reminders or notifications sent via a mobile device or computer, it is clear the consumer would appreciate more communication. Research showed that consumers want more proactive ways to feel in control of their money.

More than half of European respondents found digital alerts and notifications as ‘very’ or ‘somewhat’ useful, with post-payment balance notifications being the most popular (80%). Other alerts found to be ‘very’ or ‘somewhat’ useful include:

- Notification of all payments more than a specified amount: 76%

- Notification of total monthly spending: 76%

- Showing real-time balance before making mobile payment: 77%

- Notification of any debit over a specified amount: 71%

- Weekly spending levels: 70%

- Notification around financial goals: 60%

- Comparison between what is about to be purchased and another alternative use of funds: 54%

Digital Transformation Provides Opportunity and Risk

Despite the fact that over 50% of consumers still rely entirely on their traditional banking provider for banking activities, it is clear many digital options are available that could change this historical loyalty. We are already seeing more and more consumers use alternative banking solutions for online payments, P2P transfers, borrowing and money management. We are also seeing an increasing percentage of consumers move their daily banking activities to mobile devices.

This digital transformation provides both an opportunity and a risk to traditional financial institutions of all sizes. For those organizations that build more robust mobile solutions as well as real-time money management tools, the consumer should respond positively.

For those organizations who do not update their digital banking platform, there is a significant risk of attrition, as consumers find ways to simplify their banking and their life with non-traditional providers. The risk of attrition is real, and in many ways invisible.

Starbucks currently is holding deposits in their loyalty program that would make them the same size as a top 100 bank in the US. PayPal, Venmo and other digital banking solutions can eliminate brand loyalty with any specific banking organization by making consumers more loyal to the payment solution than the underlying bank brand.

The time to build digital engagement with your customers and members is now – before it is too late.