The 2018 Guide to Financial Marketing report, sponsored by Deluxe, is the industry’s best resource to understand the allocation of budgets, prioritization of strategies, and the challenges faced by financial marketers globally. For the first time, this report also provides a an understanding of the digital marketing tools being used by financial institutions to improve targeting, automate delivery and generate better results.

Compared to other industries, the banking industry lags in the application of these advanced marketing technologies, impacting both the ROI of marketing initiatives and the customer satisfaction with marketing communication. Given the decreasing cost and increasing availability of advanced analytic tools, the availability of modern marketing platforms and the decreasing cost of online communication, we are surprised by the lack of digital marketing maturity by most organizations.

As we have seen in the most recent financial marketing editions of the Digital Banking Report, while financial marketers state that they want to improve targeting, personalization and the measurement of results, the commitment to these priorities is not reflected in investments being made. Organizations will suffer if talk about improved marketing continues to be just that … talk.

Click Here to Download the 2018 Study

2018 Marketing Priorities

As has been the case in every year of the survey, ‘deepening current relationships and increasing share of wallet’ continues to be the most mentioned ‘top three’ marketing priority in 2018 (mentioned by 51% of the respondents), decreasing slightly in importance from 54% in 2017. Loan growth decreased in importance a bit in 2018 (mentioned by 44% of the respondents), but retained the number three spot as a top three priority, a drop of one spot from where this priority was for each prior year of our research.

Taking over the second spot on the priority list was the need to generate deposit growth. In 2018, 47% of respondents listed “deposit/checking growth” as a top 3 priority compared to 31% last year. This was the greatest change (either up or down) by any priority in 2018. In fact, deposit/checking growth was the most mentioned ‘top priority’ in 2018 (mentioned by 25% of respondents).

Somewhat counter-intuitively, the prioritization of acquiring new customers/members continued to fall in 2018 as did the priority of digital channel adoption. The percentage of respondents that mentioned the importance acquiring customers dropped from 35% to 30% since last year, with the importance of increasing the use of digital channels falling from 38% to 32%. Somewhat more surprising is that only 7% of all respondents placed the importance of promoting digital channels as the top priority this year.

Given the need to grow the overall customer base and the need to support digital channel, these drops in prioritization are concerning.

The importance of brand building, attracting business banking relationships and generating Millennial accounts remained relatively unchanged from 2017, with each priority remaining relatively low compared to the most important priorities. The relative importance of ‘retention’ and ‘growing new markets’ continued at the bottom of the priority list in 2018, like previous years. The reason for this lower placement is probably a reflection on the high priority of the other objectives as opposed to a marketing belief that these two priorities are “not important”.

2018 Marketing Priorities by Organization Type

Similar to 2017, when the marketing objectives are broken down by type of financial institution, larger banking organizations have a significantly different set of priorities than either community banks or credit unions. As in 2017, cross-selling continues to be a much more mentioned ‘top three’ priority for larger organizations than it is for smaller financial institutions.

In 2018, the focus of the larger banks continues to be all about digital channels, with large and regional banks making the adoption of digital channels a top 3 priority at a scale that is more than 3 times as high as community banks or credit unions.

This should be a major concern of every bank that is not in the top 10. Without a significant prioritization of digital channel engagement, the ability to acquire and retain an increasingly digital consumer base will be more and more difficult.

Part of the reason for not promoting digital channels more by smaller organizations could be because many of these same organizations lag in digital product development. This combination of slower digital transformation and lower prioritization of digital channels could be a recipe for digital disaster.

Because the largest banks are increasingly successful at acquiring new deposit and loan customers (compared to their smaller peers), the marketing prioritization of deposit and loan growth is significantly lower than other sizes of financial institutions.

Other highlights of significant priority variance by type of institution are the following:

- National and regional banks increased their mentions of improving brand awareness from 2017. Community banks and credit unions did not change the importance of branding in 2018.

- National and regional banks continue to place a lower priority on loan growth than smaller banks and credit unions, with mentions remaining at about half the level of community banks and credit unions.

- Credit unions continue to have the highest emphasis on loan growth in 2018, but this emphasis is lower than in previous years.

- National and regional banks place the highest priority on digital channel engagement and a low priority on attracting younger consumers. While this sounds counter-intuitive, it is a reflection that attracting Millennials will be a natural outgrowth of supporting digital channel usage.

- Community banks place a much heavier emphasis on building business relationships than larger banks or credit unions.

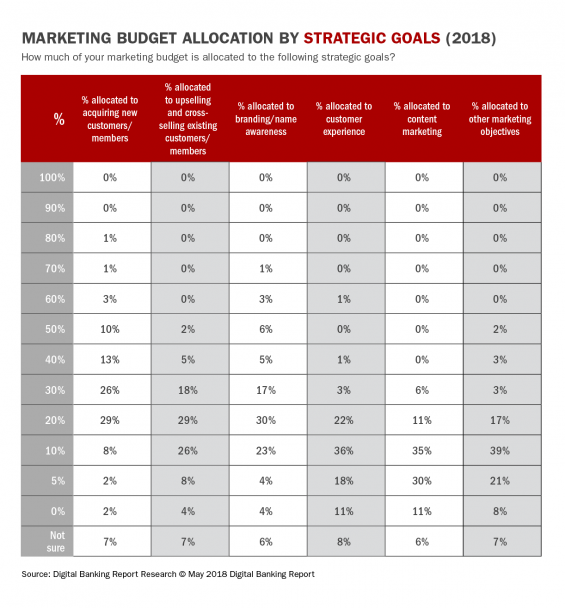

2018 Marketing Spend Not Aligned With Goals

Again in 2018, marketing budget allocation did not correlate with marketing priorities. For instance, 54% of financial institutions spent 30% or more on new customer acquisition, while only 25% of organizations spent 30% or more of their budget on cross-sell or up-sell of customers/members. While some of this allocation variance could be attributed to a higher cost to reach prospects, it is more likely that the budget allocated to generate sales from current customers is underrepresented. This contradicts the priorities mentioned.

While improving the customer experience has been the top retail banking trend for the last three years, only 5% of organizations allocated 30% or more of their budgets to this objective. This may be because some organizations don’t budget for CX initiatives independently or it is possible that it is not a marketing expense at some organizations.

As in the past, while organizations don’t mention branding as a top priority, spending on the organization’s brand continues to be larger than expected. For instance, in 2018, 32% of organizations allocated more than 30% of their marketing budget to brand awareness. In an age of personalized communication and digital connectivity, this level of emphasis on brand development seems higher than needed.

Click Here to Download the 2018 Study

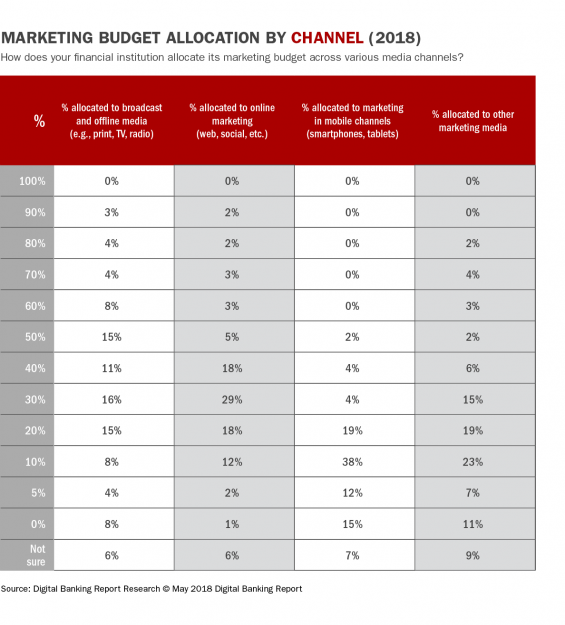

Marketing Channel Spend Remains in the 1990s

Global respondents to our financial marketing research survey illustrate how much we still use traditional media. For instance, financial institutions did not reduce their broadcast and offline marketing budgets over the last 12 months on average. As in 2017, 34% of financial institutions allocated 50% or more of their media budgets to traditional media. As was the case last year, there was a lack of commitment to digital channels, with only 15% of organizations committing more than 50% of their budgets to online media (compared to 14% in 2017).

Finally, similar to the prior two years of this research, virtually no organization committed more than 40% of their budget to mobile marketing, with only 2% of organizations committing over 50% of their marketing budget to mobile. In fact, the spending curve for mobile was almost exactly as it was for 2017.

Invest in Financial Marketing 2020

Despite the tremendous advance in consumer insight and advanced analytic tools, the banking industry continues to lag the marketing experiences created by other industries. Financial marketers must invest in new technologies and revisit product and channel strategies that reflect the expectations of the consumer.

In order to build personalized communication that reflects real-time changes in a consumer’s lifestyle, banks and credit unions need to stop making modest adjustments to previous marketing plans, and completely revamp strategies and tactics that are ready for the year 2020 and beyond.

This includes a major shift from acquiring new customers to using advanced analytics to provide contextual recommendations to current customers. This will change both the marketing priorities as well as the media channels used. This also includes investment in advanced analytics and marketing automation tools.

Without these investments, organizations will be ill equipped to serve consumer in the future.

Purchase the Report

The 2018 Guide to Financial Marketing, sponsored by Deluxe, provides insights into the strategies, tactics, priorities and challenges of financial marketing departments globally. Beyond a review of what banks and credit unions are focusing on in the coming year, there are comparisons to previous trends and insights into the use of new marketing technology solutions.

The report is based on a survey of over 200 financial services marketers worldwide and includes 90 pages of analysis and 44 charts.

You can download an executive summary of this Digital Banking Report or purchase the report by clicking here.