Over the past few years, more traditional and non-traditional lenders have developed improved digital lending processes. This includes investments in online applications and borrower portals, as well as new digital tools to improve borrower acquisition and servicing. For the most part, the digital transformation has focused on automating previous paper-based processes as opposed to significantly improving the borrower experience.

The industry is ready for Lending 2.0, where traditional loan processes are abandoned for completely new experiences which mirror the experiences in other industries. Instead of completing a traditional application online or on a phone, best-of-class digital lenders are finding ways to significantly reduce the steps needed to compete an application, and have vastly improved the speed of approval and funds deployment by completely revamping internal processes. Finally, by leveraging AI, machine learning and expanded internal and external data sources, the number of household who can be approved for loans can be expanded exponentially.

According to a study from PwC, “Lenders need to think bigger than ‘minimizing the number of clicks,’ reducing manual data entry, and improving the speed of decisions. Instead, digital investments need to be aligned to the overall company strategy and desired omnichannel experience.” Organizations need to avoid digitizing current inefficient legacy processes. Organizations that don’t change underlying loan culture, processes, and technology will not succeed in the long term.

“Financial institutions today are seeing a rapid change in the channel equation. The percentage of applications received via branch and call center is diminishing while the digital channel is growing rapidly. Lenders today must develop quick to market strategies that help them position as a digital lender or risk losing to other lenders who innovate quickly,” states Kyle Kehoe, President of the ACTion Business Unit at CRIF Lending Solutions.

Expanding Digital Banking Capabilities to Serve Borrowers

There is no denying the exponential growth of online and mobile banking for day-to-day transactions, such as viewing account balances, making payments and transferring funds. According to Juniper Research, by 2021, half of all adults worldwide will use a smartphone, tablet, PC or smartwatch to access financial services— up 53% from 2017. The acceptance of digital banking solutions is expected to continue to increase as more consumers integrate digital solutions from all industries in their daily lives.

Most consumers are already asking for simpler, faster and more personalized solutions from their financial institution. The challenge for most banks is being able to develop digital solutions that extend beyond basic transactional banking services.

Competition is already addressing needs not met by traditional lenders. In addition to creating digital-first solutions that simplify the application, closing and disbursement processes, non-bank lenders are creating demand for new services not offered by most traditional banks and credit unions. For instance, marginal credit risk personal loans, digital student loans, digital mortgages, and even digital small business and commercial loans are being offered.

Digital lending solutions are typically much faster, more transparent and easier to understand the logic of approval due to expanded sources of insight on the borrower. In a 2016 Federal Reserve survey, 45% of respondents complained of long waits for a credit decision, and 42% felt the application process was difficult. In contrast, online lenders far outperformed traditional banks on both counts, with only 17% complaining about long waits and 26% noting a difficult process.

With consumers shopping and making most decisions online or on a digital device, traditional banking organizations may not even realize they have lost a loan opportunity. And, despite believing that a ‘digital lending’ solution is offered, if the experience is not a lot faster than the paper process being replaced, process abandonment occurs.

Read More: Advanced Analytics And The Future of Digital Lending

Challenges to Offering Digital Lending Solutions

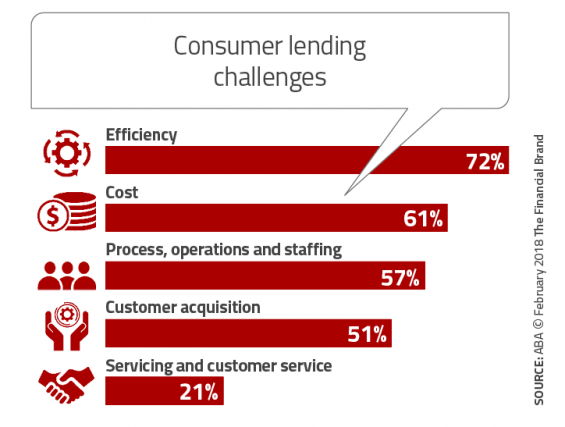

When asked to cite the challenges banks face in consumer lending, respondents to an ABA survey said efficiency was the leading concern (72%), followed by cost (61%), and process, operations and staffing (57%). The responses were much the same for small business loans.

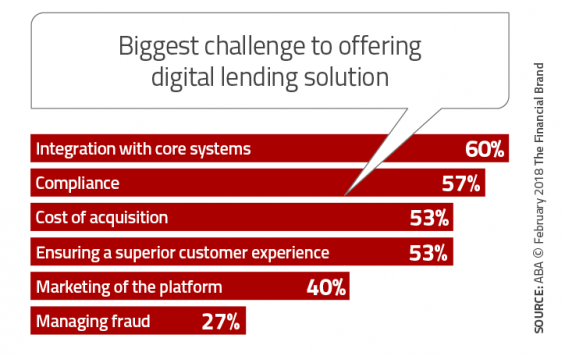

When asked the biggest obstacles to implementing a digital lending platform, respondents in the ABA survey were most concerned about integration with core systems (60%), compliance (57%), cost of acquisition (53%), and ensuring a superior customer experience (53%).

When asked the biggest obstacles to implementing a digital lending platform, respondents in the ABA survey were most concerned about integration with core systems (60%), compliance (57%), cost of acquisition (53%), and ensuring a superior customer experience (53%).

Playing Digital Lending ‘Catch Up’

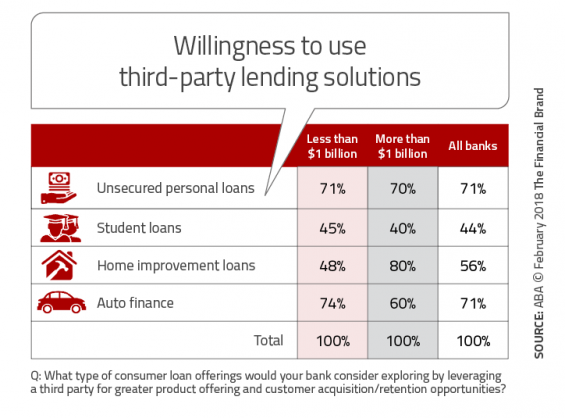

According to the ABA research, only half of larger banks (assets above $1 billion) and just 38% of smaller banks are already using a digital loan origination process, usually for mortgage and consumer loan origination. Within the category of consumer loans, digital loan origination was most prevalent for unsecured personal loans (73%), home improvement loans (56%) and automobile loans (69%).

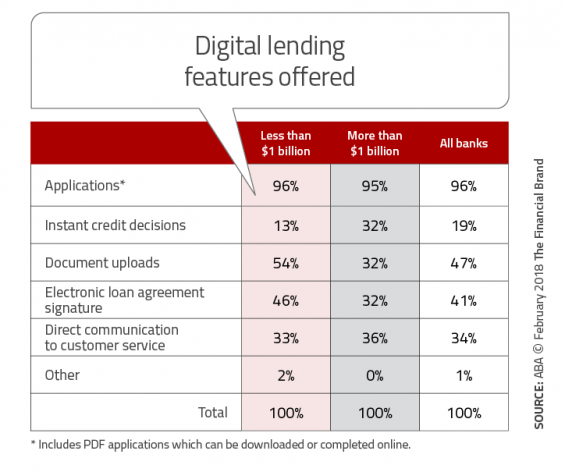

Of the banks that offer digital loans, most have only digitized the loan application (96%), compared to 47% that have

digitized document uploads, 41% e-signatures, and 34% digital channels, such as email or instant messaging for customer service. It can be assumed that these results indicate simply a digitization of paper documents as opposed to the digitization of the loan process (including back-office operations).

This is reinforced by the finding that only 13% of small banks and 32% of large banks offer instant credit decisions. This is further reinforced by the fact that in almost all cases surveyed, mobile customers in search of a loan are simply directed to the organization’s web site as opposed to a mobile application capability.

This is reinforced by the finding that only 13% of small banks and 32% of large banks offer instant credit decisions. This is further reinforced by the fact that in almost all cases surveyed, mobile customers in search of a loan are simply directed to the organization’s web site as opposed to a mobile application capability.

A Need for Speed

The primary consumer benefits of a digital lending solution are the interrelated components of simplicity and speed. How many steps can be eliminated from the traditional application process to make the borrowing experience seamless to the potential borrower? Instead of dozens of questions included in a traditional loan application, is it possible to deliver access to funds without an application? Can money be available to good customers and members every time they open their mobile banking application or in an almost immediate approval time frame?

Today’s digital banking consumer has an insatiable need for immediate gratification. They don’t want to leave their desk or move to an alternative channel if they like using their phone for making purchases. This requires a level of agility and culture not evident in most financial organizations. It also requires a complete overhaul of traditional loan approval processes.

Traditional siloed banking environments are not conducive to the development or deployment of a real-time digital lending solution. Best-in-class digital lenders are not constrained by legacy processes or organizational structures. They leverage cross-functional teams to bring a differentiated solution to market.

For instance, can traditional real-time credit bureau risk analysis be leveraged to perform real-time credit analysis on a compete customer database for loan approval? Can a combination of internal and external factors be used to pre-approve a modest unsecured personal loan for 80%+ of a customer/member file. Then, can access to these funds be made as easy as a single touch of a finger?

Emerging technologies such as machine learning, natural language processing, and conversational agents can improve efficiency, and discover hidden insights that can help digital lenders make quicker and more effective decisions. These same decision tools can help improve targeting and marketing communication.

Design Matters

When building a digital lending solution, the design must be oriented around the needs of the customer/member, while also being conducive to internal parties, such as loan officers and the marketing team. Consumers should be involved in the development of the solution, using an iterative design process.

Beyond the initial application and/or acceptance, the entire customer journey must be considered in the design. There are opportunities to apply user-centric design concepts in servicing and collections as well, with the impact of generating higher satisfaction and more loans.

Unfortunately, the design of many digital banking functionalities are built to save on costs as opposed to being built from the perspective of the consumer. “Your desired experience should drive your technology decisions. Not the other way around,” states PwC.

Delivering a Next Generation Lending Experience

Delivering a differentiated digital lending solution is more than just taking the lending process out of the branch and placing it one the computer or phone. It includes the ability to provide an almost immediate decision at the time and place desired by the consumer. It is about letting the customer or member know they have money available to borrow in close to real-time. It also includes a credit evaluation algorithm that is continuous and that includes both traditional and non-traditional scoring components, expanding the pre-approved borrowing universe.

The result is a lending solution build for the digital consumer, providing an exceptional consumer experience. Ultimately, it should significantly increase loan generation while lowering costs. The solution may be built internally, or in conjunction with a fintech provider that has already done the ‘heavy lifting.’

According to Kehoe from CRIF Lending Solutions, “The most successful financial institutions deploy a digital lending strategy that enriches the full lifecycle of the loan and removes friction from all steps including automated decisioning, stipulations, verification, documents, and booking. They also have a top down culture of embracing the digital strategy in all channels.” He goes on to say, “Examples of this include having a tablet based digital experience in the branch, video chat, and optimized client risk based pricing. Lenders who do not work through the process to enhance back end legacy systems and process risk having less than optimal workflow and ultimately turning off new clients”

According to Kehoe from CRIF Lending Solutions, “The most successful financial institutions deploy a digital lending strategy that enriches the full lifecycle of the loan and removes friction from all steps including automated decisioning, stipulations, verification, documents, and booking. They also have a top down culture of embracing the digital strategy in all channels.” He goes on to say, “Examples of this include having a tablet based digital experience in the branch, video chat, and optimized client risk based pricing. Lenders who do not work through the process to enhance back end legacy systems and process risk having less than optimal workflow and ultimately turning off new clients”

In the end, successful digital lenders will focus their investments on improving the customer experience at the same time as they improve operational efficiency. Most importantly, organizations need to avoid digitizing bad legacy lending processes. Design the best new process flow and then automate accordingly … with the external and internal ‘customers’ in mind.