Massive changes in consumer behavior occurred during the pandemic and are not likely to revert back to the old ‘normal’. This includes a major reduction in branch visits and a greater reliance on digital interactions across the entire customer journey. In response to these changes, financial institutions must move beyond making banking faster and easier to building new ways to engage with customers experientially.

Humanizing the digital experience requires the combination of data, analytics and modern technologies to offer a level of personalized engagement that can exceed what was previously possible in a branch. From real-time customer support, to proactive recommendations that enhance the potential for financial wellness, this level of engagement will separate the the winning banks from those simply meeting basic transactional needs.

Customer Engagement Trifecta:

Banks must combine data, analytics and modern technologies to understand the customer journey and achieve optimal engagement.

At a time when in-person experiences can be inconsistent at best, and disappointing to the customer far too often, well supported digital engagement can provide a high level of consistency as well as humanized support.

Satisfaction with Financial Institutions Dropping

Financial institutions can no longer depend on traditional customer satisfaction surveys as the way to gauge whether a customer will remain loyal. Most satisfaction surveys use outdated metrics, giving banks and credit unions a false sense of success and security. Customers want investment in their relationship, not just their transactions.

Rather than asking about branch experiences or transactional ease, organizations must ask whether a customer’s personalized needs are being fulfilled and whether their financial institution has their best interests in mind. This includes engaging post-purchase and offering assistance using content that the customer can access at their convenience.

To achieve this level of engagement, financial institutions must combine data, analytics and technologies to understand the customer journey and deliver the type of interaction that will drive trust, loyalty, and growth.

Read More: What Customer Data Platforms Can (and Can’t) Do For Banks

More than ever, consumers don’t just want personalization, they are demanding it.

According to the World Retail Banking Report, published by Capgemini and Efma, consumers want their financial institutions to provide personalized experiences that are rewarding, emotionally connected, and integrated with their lifestyle. Unfortunately, nearly half of the survey respondents said their banking relationships were neither emotionally connected nor well-integrated into their lifestyles.

Many respondents also said they were not receiving seamless experiences across all channels, value for the money, or innovation that keeps pace with other digital relationships.

( Learn More: The Ultimate Customer Engagement Playbook in Banking )

Banks Must Leverage Power of Personalization and Engagement

McKinsey found that companies that excel at personalization generate 40% more revenue from those activities than average players – across all industries. Organizations that are leaders in personalization differentiate by creating customized recommendations, reaching the right individual at the right moment with the right engagement communication.

72% of consumers expect the businesses they buy from to recognize them as individuals and know their interests. Transactions and ongoing engagement have a significant positive impact. “Recurring interactions create more data, allowing for even more relevant engagement over time – creating a flywheel effect that generates strong, long-term customer lifetime value and loyalty,” states McKinsey.

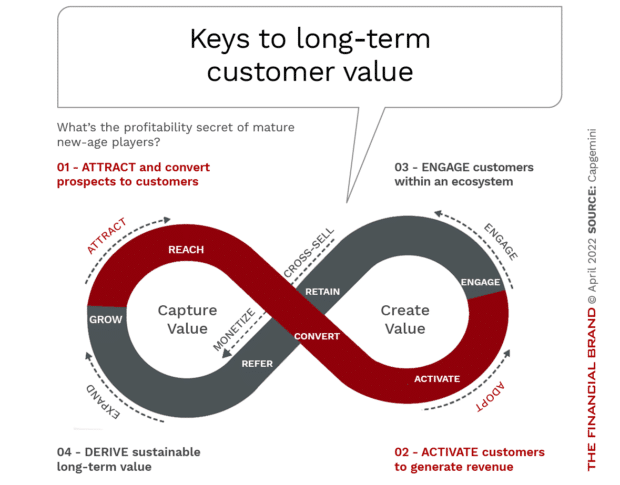

Personalization Extends Beyond Marketing:

Rather than focus solely on short-term marketing wins, banks should look for long-term drivers of growth and emphasize customer lifetime value.

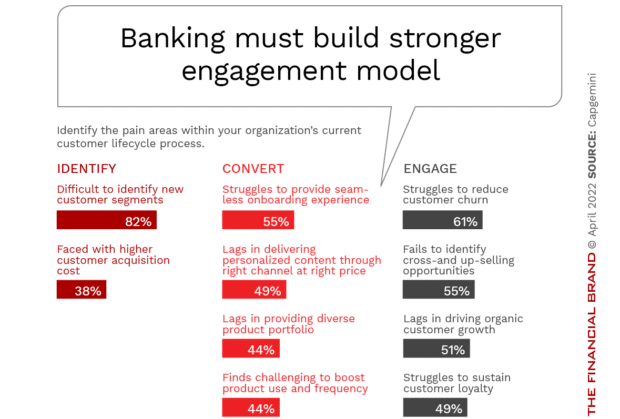

Capgemini found that most banks are challenged to build a strong engagement model across the entire customer lifecycle. The overwhelming majority of organizations (95%) are negatively impacted by outdated legacy systems and core banking platforms. Similarly, 80% stated that the lack of data maturity hinders customer lifecycle process improvements. According to Capgemini, 82% said they have difficulties identifying new customer segments and 55% struggle to provide seamless onboarding experiences.

( Learn More: Consumers Demand Improved Digital Banking Customer Engagement )

Invest in Future-Ready Data Infrastructure

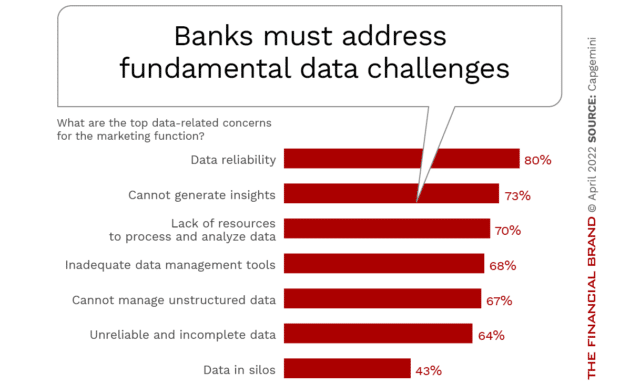

Banks and credit unions have vast amounts of internal and external data at their disposal, from transaction and demographic data to locational, behavioral, lifestyle and social data. Despite this abundance, 73% of financial executives surveyed by Capgemini said they struggle to turn data into useful insights.

Not only do banks have concerns around data reliability (80%), but almost three quarters can’t generate insights and 70% said they lacked the resources required to process and analyze data. As incumbent banks race to keep pace with the nimble fintech organizations, financial institutions of all sizes can leverage third-party solution providers to convert raw data into valuable insights that can support personalization and engagement initiatives.

Third party partnerships can also help to create new offerings that combine traditional bank offerings with non-financial lifestyle products and services. Partners can also help to create embedded banking solutions with non-financial third parties. These new platform models go beyond collecting data for enhanced personalization, by creating new revenue opportunities outside fees and spread.

Customer Engagement Goes Beyond CMO Role

While research would lead to the belief that the CMO is expected to own the customer lifecycle and manage each facet of customer engagement, the reality is that building an engagement model across the customer lifecycle requires a cross-organizational commitment. Data and insights must be shared to empower all employees to assist with the innovation, product development and customer engagement process. Obviously, this requires the commitment and support from the C-suite.

Businesses that succeed in scaling personalization and engagement must create teams that cut across marketing, product, analytics, and technology, using a hub-and-spoke approach to reach the customer at the point of interaction. According to McKinsey, these teams run hundreds of tests per year, enabled by advanced data analytics and test-and-learn techniques.

As can be expected, most financial institutions and, more specifically CMOs, are still not adequately prepared to move from a product-centric organization to a customer-centric financial institution. There needs to be a cultural shift at most organizations that will support the customer journey – from the customer’s perspective – helping the customer improve their financial wellness.

According to McKinsey, “Looking across the customer lifecycle, leaders build a granular view of where there is the most value. They leverage customer segments and micro segments, and factor in behavioral, transactional, and engagement trends. They use those insights to define and quantify their personalization and engagement objectives and ground their efforts in customer-centric key performance indicators (KPIs).”

Financial institutions that can build a strong personalization and engagement model at scale will be rewarded with increased sales, improved loyalty, enhanced revenue growth, and a flywheel impact that will position the organization on an enhanced trajectory.