Following on the heels of what happened with consumer banking, financial institutions are seeing fintechs and other non-traditional players increasingly eat away at their small-to-medium sized business (SMB) clientele. A major reason for that is banks’ inability to routinely use data day-to-day for tailored customer offers and decisions, and failing to take advantage of all the internal and external data at their disposal.

That’s the conclusion drawn by a new Accenture report. And it explains why SMBs are one area where fintechs have been highly successful in snatching customers from banks and credit unions. Indeed, there are now more than 140 fintech startups serving SMBs and entrepreneurs, addressing needs including bookkeeping, expense-tracking, insurance, invoicing, payment processing and payroll, according to a 2020 11:FS study.

The study found that 62% of SMBs don’t believe their business banking account offers any additional benefits compared with their personal accounts. Just over two-thirds (67%) use one of six fintech business platforms compared with 51% using one of five large banks.

Dig Deeper: Fintechs Threaten to Disrupt the Small Business Banking Market

The New Competition:

Shopify, which is used by around 30% of all U.S. ecommerce sites, is now the 10th largest platform providing financial services to SMBs.

The Accenture report highlights several notable examples of fintech disruption in this area. One is Shopify, which is used by around 30% of all U.S. ecommerce sites. It is now the tenth largest platform providing financial services to SMBs. Another is Stripe, which has created an end-to-end lending application programming interface (API) for ecommerce sites to offer financing options to SMB customers, adding further potential to erode into traditional institutions’ business.

“Many [financial institutions] are responding to these challenges by ramping up their investments in data, advanced analytics and artificial intelligence (AI),” Accenture states. “Yet most have encountered roadblocks on their journey towards data- driven reinvention.

“Much of the rich, real-time transactional data to which banks have access lies fallow.”

— Accenture

“While many [institutions] have developed pockets of data and analytics excellence,” the firm consulting firm continues, “they are struggling to scale up deployments, embed data-driven decision-making into day-to-day operations, and use data to drive truly transformative change across the business. Much of the rich, real-time transactional data to which they have access lies fallow.”

Read More: How to Nail the Small Business Banking & Lending Market

Tons of Data, Yet Key Details Are Lacking

A major issue for traditional commercial banking providers is that some of the traditional data sources they use for decisioning don’t provide enough detail on customer behavior to glean meaningful insights, observes Jared Rorrer, a managing director and head of Accenture’s Commercial Banking industry group. Things change dynamically, and it’s necessary to respond quickly, with the right insights for decision-making, at the right time, he says.

“This requires an expanded data ecosystem, combining first-party, third-party and broader digital signals to inform the bank’s actions,” says Rorrer, who responded by email to questions from The Financial Brand. “However, many banks are not able to fully leverage the power of their expansive internal data sets because they lack a scalable and agile data foundation and the appropriate levels of multi-speed data governance.

“Banks are also challenged with understanding exactly what questions need to be answered and what information sets and insights are best suited to get to that answer,” Rorrer continues. “What is important to know about the customer so that the bank can reach out with relevant messages and offers?”

Read More: The State of Customer Data Management in Banking

What Are the Biggest Obstacles?

The four main obstacles that banks face in achieving this level of data maturity as described by Rorrer are:

- Internal siloes

- A focus on making incremental rather than wholesale improvements

- Digital transformation “fatigue”

- A lack of business ownership.

Some of these issues are nothing new. Organizational silos are often cited as a major hindrance to achieving any kind of meaningful digital transformation at banking organizations. For example, Accenture says that 50% of financial institutions cite difficulty in accessing data from disparate internal sources as one of the top three challenges in implementing their AI strategy.

When they do engage in data-driven transformation projects, financial institutions tend to focus solely on “easing immediate pain points” the Accenture report notes, which is more of a band aid strategy than a wholesale shift. This is exacerbated by the time spent by IT departments digging banks out of technical debt as a result of years of digital transformation projects, which leads to a lack of appetite internally for taking on more lengthy IT projects.

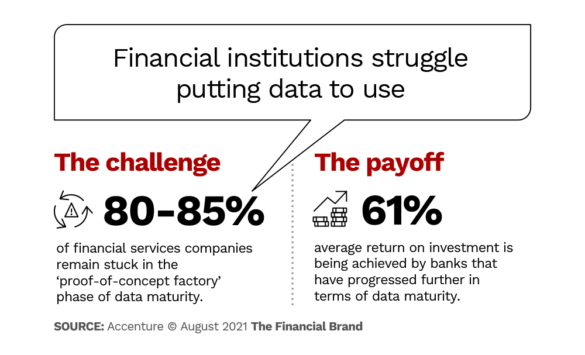

These can be strong headwinds to overcome, notes Accenture: “Many are finding themselves trapped in a loop of frustrating proofs of concept and are unable to grow data and analytics efforts beyond a few small centers of excellence. Rather than using data to drive innovation and create new business models, they are reaping modest returns on investment from small revenue or cost-reduction wins.”

How to Rack Up Some Data Wins

Jared Rorrer notes that banks and credit unions can invest in critical building blocks to break through internal silos and make better use of data, such as data access, quality, and cloud-based foundations.

He also says that data-driven institutions invest in empowering employees to conduct basic data, business intelligence and analytical tasks. “Banks looking to get the most out of their data can mobilize cross-functional teams — business, IT, data and analytics — that work together to share insights, fostering a sense of engagement in the process from the start.”

Data leaders at financial institutions can get internal buy-in for bigger projects by focusing first on small wins and moving up from there. For example, Accenture notes that a bank or credit union may start out by using machine learning to inform credit decisions around short-term products where the risks of loss are low. It can then expand these capabilities to additional risk products such as overdrafts, corporate credit cards and merchant cards.

As it grows its data capabilities and confidence, the institution can expand autonomous capabilities to trade products and core lending products such as foreign exchange and derivative products, traditional cash flow loans, and asset-based lending.

Ultimately, Rorrer says that traditional institutions can start to win back SMB customers by through proactive and preemptive customer engagement and offering purpose-driven and forward-looking products and services.

In time, the analyst believes that banking providers can increase efficiency by leveraging data-driven operating models, AI and cloud-enabled architectures and strong ecosystem partnerships to drive transformation at scale.