In the first quarter of 2021, fintech firms worldwide raised $22.8 billion in investments through 614 deals. – more than doubling the amount raised in the fourth quarter of 2020 – and representing the largest venture capital-backed fintech funding quarter ever, according to research released by CB Insights. The first quarter 2021 numbers even surpassed the the previous funding record from Q2’18 that included Ant Group’s $14 billion funding round.

Much of the growth in the first quarter can be attributed to the 57 mega-rounds of $100 million+ that occurred in the first quarter. This was the most mega-rounds ever, accounting for 69% of total funding in the quarter. This made the average deal size for Q1’21 almost double what was seen in Q4’20 – from $19.3 million to $37 million.

North America led the fintech funding race (264 deals/$12.8B), followed by Europe (151 deals/$5B) and Asia (147 deals/$3.7B). Combined, these three regions accounted for over 90% of the total fintech funding for the quarter. While Australia (11 deals/$193M) and South America (20 deals/$999M) both saw modest increases in deals, Africa saw a 22% drop in deals during Q1’21 (21deals/$45M). Europe saw funding growth almost triple quarter-over-quarter, attributed to mega-rounds which accounted for 68% of the continent’s total funding for the quarter.

Why Should I Care About Fintech Funding:

Seeing where venture capital money is flowing helps traditional banking organizations understand what financial sectors, regions and specific competitors are drawing the most attention in the marketplace. This perspective can assist in prioritizing strategies.

See Also: The World’s Biggest Interactive Directory of Digital Banks

Not All Sectors Participated Evenly in Fintech Funding Growth

When the funding is broken down by sectors, there were some that saw significant growth in Q1’21, while others saw only modest gains. The largest levels of funding were in the payments, digital banking, digital lending and wealth management sectors. A recap of the key events in all eight sectors covered by CB Insights is provided below:

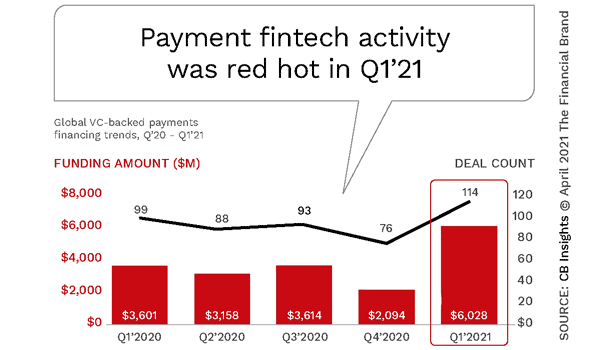

Payments. Funding for payments companies tripled compared to the previous quarter, with over $6 billion in funding. The number of deals (114) increased by 50%, with 18 mega-rounds accounting for over 75% of the total funding.

Neobanks. The number of deals for digital banking fintech firms (65) declined by 12% from Q4’20 to Q1’21, but funding grew by 25% during the same period. This was the first decline in deal activity since Q4’19, but the third consecutive quarter of funding growth.

Digital Lending. Funding within the digital lending sector tripled to $4 billion in the first quarter of 2021, while the number of deals doubled to 102 during the same period. There were eight mega-rounds in the quarter, which was was the highest total since Q2’19.

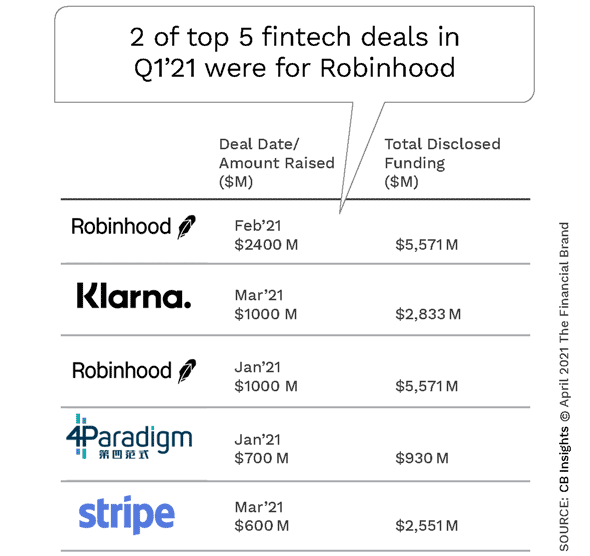

Wealth Management. The funding in the wealth management sector grew by more than 5X to $5.4 billion for the most recent quarter. Companies in the space have created products and services that change the way people invest, save, and manage their money. The majority of the funding (63%) was the result of two funding rounds for a total of $3.4 billion for Robinhood during the quarter. That said, the number of deals still rose by 27% during the quarter.

Insurtech. Funding in the insurtech sector increased only 12% for Q1’21 ($2.3B), while the number of deals actually dropped from 97 to 92. According to CB Insights, the insurtech sector was the only major fintech sector where mega-rounds represented less than 50% of total funding in the quarter.

Capital Markets. Funding in the capital markets sector increased by 250% to $8 billion in Q1’21, while deal activity dropped by 4%. Like wealth management, mega-rounds were over 80% of total funding in the quarter. Interestingly, since 2010, private companies in the capital markets category have received the most individual investments from banks out of any fintech category.

SMB. Fintech solutions geared at small- and medium-sized businesses (SMBs) have been getting more attention as more organizations try to serve the needs of this often forgotten segment. While there was a drop in the deal activity for the SMB sector for the third consecutive quarter, funding grew by 2.5X to $3.4 billion during the period.

Real Estate. Despite a pandemic-fueled jump in mortgage and refinance applications, mortgage funding dipped in 2020. As the real estate market makes a strong comeback, real estate sector funding appears to be making a comeback, with funding to real estate companies growing 29% to $2.4B for Q1’21.

While M&A and IPO Activity Soared, Investment Performance Has Lagged

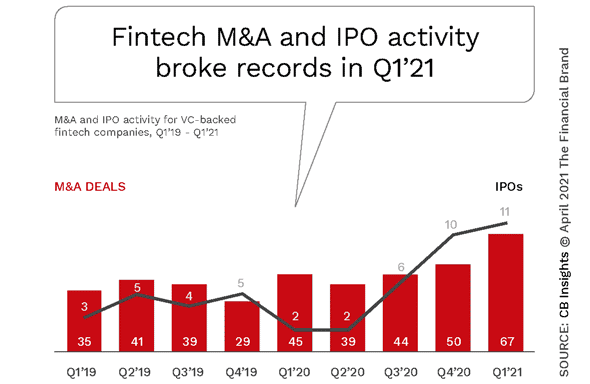

During the first quarter of 2021, the number of M&A deals for VC-backed fintech companies hit new highs (67), with IPOs following suit (11) during the period. While most of these exits came into the market with very high valuations, performance since going public has lagged the S&P performance since the first of the year.

Interesting Insight:

While the focus around fintech investment is usually on venture capital (VC) funding, traditional banks are increasingly investing in fintech firms.

Big Banks are Big Fintech Investors

A recent research report from CB Insights provides insights into where three of the top banking organizations are investing in fintech firms. According to the report, Goldman Sachs and Citigroup are among the most active investors, through their investment arms GS Growth and Citi Ventures respectively. The two firms have participated in 69 and 51 fintech deals respectively from 2018 through 2020 across a broad array of fintech sectors.

Goldman Sachs has focused much of its recent M&A strategy on wealth management, alternative lending and capital markets. Citi has also focused on the capital markets sector, backing 13 deals in this area since 2018. Citi has also made investments in the payments and wealth management sectors.

Finally, JPMorgan focuses their fintech investments on the capital market and small business sectors. According to CB Insights, the company has invested in 12 capital markets deals and seven in SMB solutions between 2018 and 2020. JPMorgan also made four investments in wealth management and four in payments.