For about a decade now, studies, research reports and countless experts have been telling banks and credit unions what Millennials want from a financial institution. We’ve heard that Millennials hate big banks, love big banks, will never walk into a branch, actually want branches near where they live, and many other conflicting edicts. As the oldest members of this huge cohort approach 40, it’s worth reexamining another tried and true stereotype: that Millennials hate credit cards.

While it does seem like younger generations cast a more skeptical eye towards debt, there is still a place for credit cards in the Millennial wallet. Any number of breathless Chase Sapphire Reserve unboxing videos on YouTube make that apparent. Financial institutions wanting to deepen relationships with Millennial customers can do so by offering a credit card product that suits their needs, focusing on tangible benefits rather than just fees.

Default Option: No Fees, Low Interest

While many of the status symbol credit cards that appeal to social media savvy influencers do carry stiff annual fees, many Millennials will flock to no-fee cards. According to a survey from The Ascent, a research arm of The Motley Fool, 41% of Millennials own a no-fee credit card, the second highest percentage of age groups surveyed behind Baby Boomers. It’s clear that many Millennials appreciate the utility of credit cards, but have a discerning eye when it comes to fees. Even for cards with fees, financial Institutions can offer to waive the fee for the first year as a way to entice younger customers and build a long-lasting relationship.

Low interest rates are clearly another big factor for Millennials. According to the Ascent survey, interest rates were the top consideration for Millennials when choosing a credit card, ahead of having a good rewards program and no annual fees, in second and third place respectively. While no (or delayed) fees and low interest rates may not seem appealing for credit card issuers as it means less immediate revenue, the flip side is that these measures can help institutions build the foundation of a long-lasting and profitable relationship.

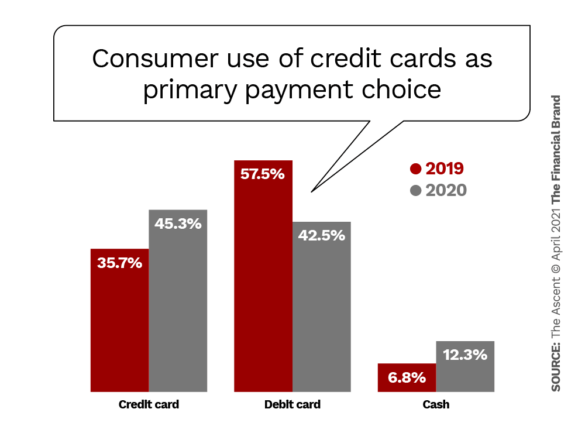

This is especially important because credit card usage is generally up. Nearly half of the respondents in the Ascent poll reported using credit cards as their primary payments vehicle in 2021, up sharply from the previous two years.

As credit card usage grows in popularity, financial institutions have a real opportunity to make further inroads with this generation, many of whom are accruing more wealth due to advancing in their careers as well as through generational wealth transfers.

Key Point:

Millennials are moving towards cards with no fees. Cards with annual fees can improve their chances by offering to waive the first year’s fee.

The Right Kind of Rewards

It’s fairly self-explanatory to say that consumers of all ages like cards that come with rewards. However, offering the right kind of rewards program is critical to capturing the Millennials eye — and dollar.

So, what does this age group want from rewards programs? Traditionally those have been programs that offer big points from usage spent on dining out and travel. After all, we have been told time and again that Millennials value experiences over possessions. Millennials — like most of the rest of us — have not done too much of either of those activities over the past year.

But as the world hopefully continues to reopen, Millennials will likely have a pent-up urge for dining and travel to get out of their system, and programs that reward spending in those areas will likely prove to be popular.

As the Millennial-focused Million Mile Secrets blog notes, “We millennials appreciate Instagram-able experiences, no hassles, no frills, efficiency, and the ability to do things on our time. In my conversations with fellow millennials, I’ve noticed there is a large misunderstanding about credit cards. There are so many opportunities to see the world using miles and points earned from the best travel credit cards.”

Since credit card rewards programs based heavily around travel and dining out did not get much usage in 2020, some issuers leaned hard into groceries, food delivery, streaming services and other everyday categories, Bankrate notes. However, these proved to be far less popular than programs based on travel and restaurants.

Read More: Is Everything Bankers Think They Know About Millennials & Gen Z Wrong?

Takeaway:

As travel and dining out become more regular again, Millennials will flock to rewards programs that offer points or cash back.

As dining out in restaurants and travel (especially international travel) make a welcome return to our lives, credit card issuers have a chance to reengage with Millennials by again offering robust rewards programs in these areas. The Ascent also notes the continuing popularity of such programs despite the pandemic and that the best ones “allows you to pay for your biggest travel expenses — including first-class airfare and luxury hotel stays — with travel rewards instead of cash.

You could also find travel cards that let you access airport lounges, offer complimentary travel insurance, or get you free upgrades on travel bookings,” adding that the best travel programs eliminate the need for customers to pay a foreign transaction fee on purchases made while traveling abroad.

The Bottom Line on Millennials and Credit Cards

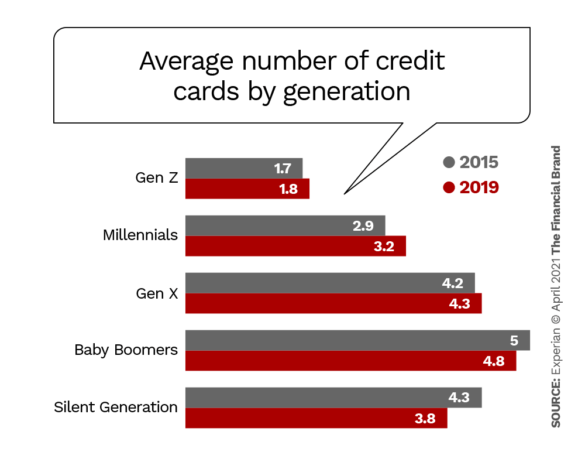

For all the talk about Millennials eschewing credit cards, the fact remains that they still own them (an average of 3.2 credit cards each, according to Experian) and have demonstrated they will use them if they are targeted to their needs and desires.

This can help financial institutions foster deeper relationships with Millennials and perhaps entice them into other financial products we have been told they are not interested in — such as a mortgage.

Because as it turns out, people’s tastes change as they get older. As so eloquently put in this article from Experian: “The further out Millennials get from the financial crisis of the late-2000s — when they witnessed the effects of out-of-control debt — the more open they seem to be taking on new credit and debt.”

Read More: 10 Years Ago, Targeting Millennials Was Critical – What Now?