There was never a year like 2020 in retail banking. Even before the pandemic resulted in over a million lives lost, businesses shut down worldwide, and social consciousness caused global protests, the banking industry was in a state of transformation. But the impact of change was accelerated exponentially during 2020, with digital engagement and technological advancements advancing years in a matter of months.

As we entered 2020, it was already clear that the most successful retail banks were exhibiting digital leadership that drove advanced innovation and a higher level of profitability. The gap in success between the banks that embraced digital transformation and those that were laggards started to appear in new customer acquisition results, efficiency ratios, customer satisfaction improvements, and overall digital maturity. The impact of both fintech firms and non-financial tech giants was being felt and consumers continued to ‘kick the tires’ of alternative banking options.

Continuing a trend that had been in place for several years, most financial institutions stated a prioritization of an improved customer experience while, in actuality, many still were focused more on cost containment. Digital banking leaders already realized the importance of real-time advice, leveraging open banking and restructuring delivery networks to favor digital over physical. For fintech firms, the importance of scale was already clear, with many firms looking to partner with traditional financial institutions that wanted to jump-start product innovation initiatives.

Below we reflect on some of the most popular topics from 2020 with related charts and illustrations.

Read More:

- 7 Essentials of Digital Banking Transformation Success

- How to Avoid Digital Transformation Failures in Banking

- Digital Transformation Requires More Than Technology Upgrades

Digital Transformation Lacks Definition

The potential benefits of digital transformation were understood in early 2020, but few organizations fully understood what was required to become a ‘digital bank’. Most considered digital banking as the ability to conduct banking online or with a mobile app as opposed to providing a digital experience comparable with tech giants.

Beyond not having a clear understanding of what digital transformation required, few organizations were moving forward aggressively to provide the best digital banking functionality. According to the Digital Banking Report, “State of Digital Banking Transformation,” published in January, few organizations considered themselves digital transformation leaders, with less than 50% of organizations believing they were prepared for competitive threats, customer expectations or technology advancements.

![]()

Part of the challenge at the time was that leadership lacked experience in implementing massive transformations. At the same time, the financial strength of the industry in January 2020 resulted in complacency around making large, overarching changes to what had long been the operating norm in banking.

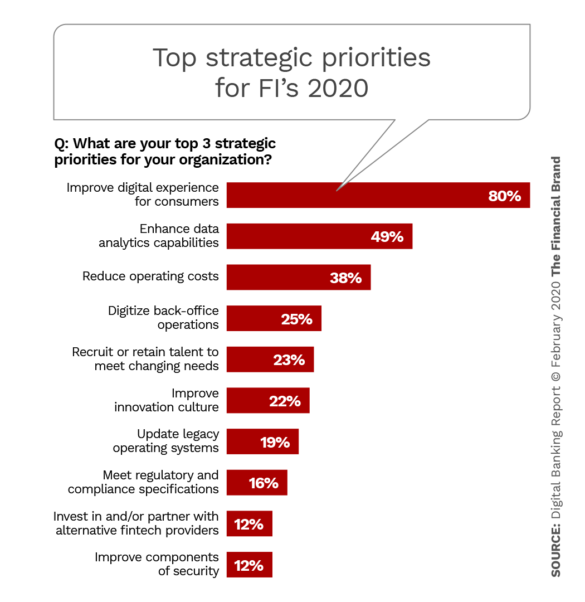

When asked about the types of investments in digital technology financial organizations were making, 80% responded that they were investing in mobile technologies. This illustrated the importance of the mobile banking channel to the execution of digital technology goals but also reflected a rather narrow definition of digital transformation.

The research done at the time reflected steps that can improve the potential for digital transformation success that are still relevant today:

- View the digital transformation process as overarching, creating new business processes and integrating new technologies from the inside out.

- Have digital-savvy leaders who are willing and able to lead an entire organization in the digital transformation process.

- Build the workforce of the future, providing the foundation for education and hiring.

- Focus on speed of delivery, personalization and customer engagement.

- Support a culture of innovation and encourage the building of new business models.

Read More: Why Most Digital Banking Transformation Efforts Have Stalled

Use of AI in Banking Fails to Meet Expectations

The discussion of the importance of artificial intelligence (AI) in banking was very prevalent in early 2020, with some financial institutions embarking on initial testing of deployment of models using the vast amount of data available. Unfortunately, while there was no question that the use of data and AI benefits the consumer, the vast majority of deployment by legacy organizations continued to focus on cost reduction and productivity and/or risk management. In other words, very little of the focus was on the customer experience benefits possible with AI.

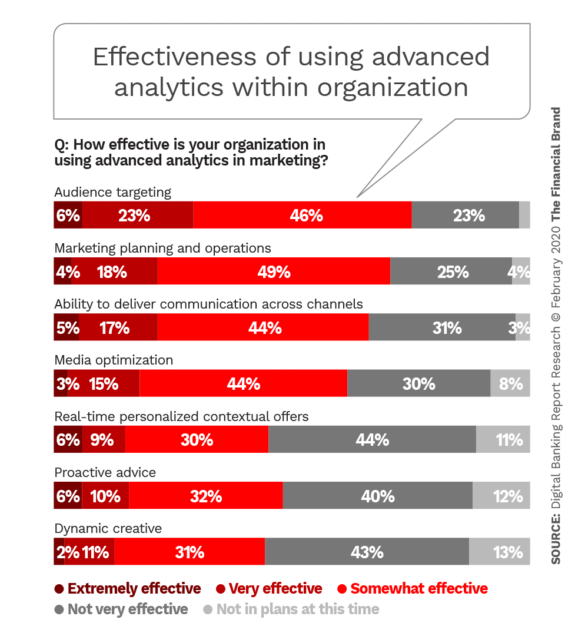

When we asked financial institutions globally about their strategic priorities as part of the Retail Banking Trends and Predictions report, it became clear that the deployment of AI for the benefit of the consumer has lagged the hype by a significant amount.

The research found that only the largest financial institutions, and some of the smallest organizations considered themselves adept at advanced targeting, multichannel communications, real-time contextual offers or proactive advice. Despite the impact of the pandemic, these dynamics did not change significantly during the past year.

The research found that only the largest financial institutions, and some of the smallest organizations considered themselves adept at advanced targeting, multichannel communications, real-time contextual offers or proactive advice. Despite the impact of the pandemic, these dynamics did not change significantly during the past year.

Read More: Artificial Intelligence in Banking: More Hype Than Reality

Digital Skills Gap Impacts Digital Banking Transformation Success

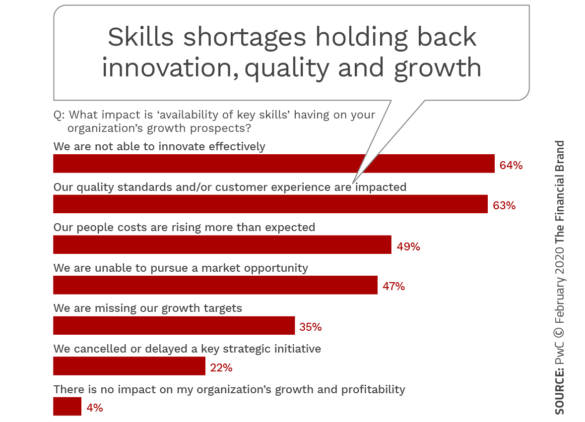

While financial institutions were investing more in technology and digital capabilities in early 2020, much of the payback from these investments were stalled due to the lack of digital talent within the organizations themselves. According to PwC’s 22nd Annual Global CEO Survey, published in February, almost 80% of the banking CEOs who responded saw skills and talent shortages as a threat to their growth prospects, with 35% being ‘extremely concerned’ and 44% being ‘somewhat concerned’. “Most [financial institutions] believe that this skills gap is undermining their organizations’ ability to innovate effectively and provide a winning customer experience,” stated the report.

The research found that the skills shortage had an impact on all areas of financial institution growth. For instance, nearly two-thirds of respondents who stated they were ‘extremely concerned’ about skills shortages believed that their organization would be ‘unable to innovate effectively’ or that quality standards and/or customer experience would be impacted.

Despite the need for skills that were in short supply within financial institutions, few organizations filled these needs with outside talent. While some of this hesitation was caused by a concern around needing financial institution experience, part of the challenge was because of the negative view of the banking industry by skilled digital talent.

Alternative options to hiring from the outside was partnering with current solutions providers, strategic partners or hiring project workers that are not part of the full-time staff. A better long-term solution would be to up-skill and re-skill current employees within the organization. The PwC research found that 40% of organizations were interested in retraining and up-skilling, with 23% willing to hire from competitors, and with 16% hiring from outside the industry and building a direct pipeline from higher education organizations.

Read More: Banking Must Bridge the Growing Digital Transformation Skills Gap

COVID Disrupts Retail Banking Marketing Communication

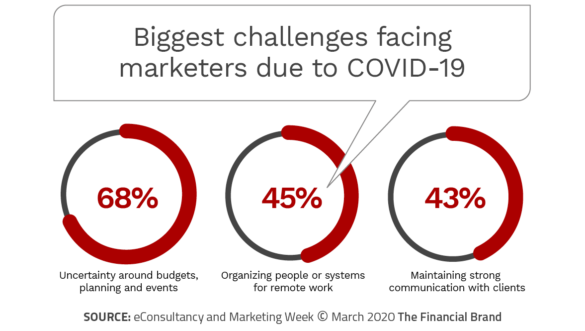

Overnight, the marketing communications playbook got rewritten in March, as organizations had to explain how to do banking without branches while providing support for consumers who may have lost jobs or were simply concerned about making their next mortgage or rent payment. Initially, marketing messages did little more than state the obvious in an impersonal way. Eventually, organizations began to provide more personalized communication around financial assistance such as loan payment deferrals and remote deposits.

As email boxes and social media became flooded with messages about COVID-19, it was increasingly difficult for a bank or credit unions to stand out from the crowd, or show a heightened level of empathy and authenticity. Those organizations that focused on personalized messages of support were rewarded with greater loyalty and word of mouth promotion as customers increasingly used social media to voice their satisfaction … or disappointment.

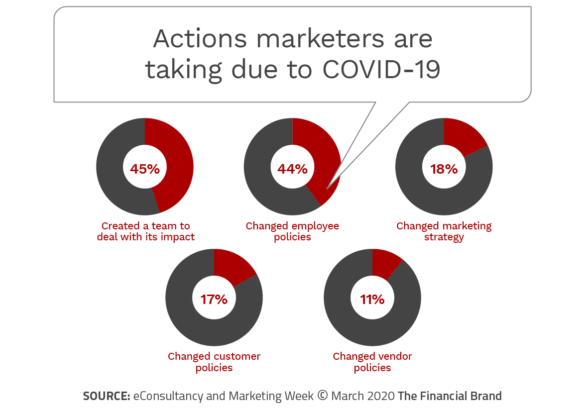

By the end of March, 45% of marketers indicated their company had created a team specifically to deal with the implications and impacts of the outbreak, while 44% changed employee policies in areas such as remote work, travel and bonuses. It was also found that organizations had already changed marketing strategy as well as consumer and vendor policies.

One of the major takeaways from the early days of the pandemic was that organizations and departments within these organizations could perform well during a crisis, even when working remotely. There was no single playbook that worked for every organization, but those that understood the importance of ultra-personalized communication that focused on consumer needs benefited early and often during 2020. Those organizations that were slow to respond or did not perform well during the pandemic will be in the worst position in 2021 and beyond.

COVID Alters Digital Banking Battlefield

As the COVID-19 crisis continued, banks and credit unions were forced to quickly provide digital engagement capabilities, from digital account opening to digital loan applications. While many of these initiatives lacked user experiences that consumers would later expect, the digital maturity improvements began to resemble what fintech and big tech players had offered for years. At the same time, many fintech firms began to be challenged by a drop in venture capital funding as money shifted to only the largest and most established non-traditional players.

More than ever, the gap between progressive legacy banking firms and fintech offerings narrowed at the same time that consumer digital expectations escalated. Coming out of this crisis, there will be much more clarity as to which organizations are embracing the digital transformation process and which firms will continue to “fake digital” – only making iterative changes to respond to short-term needs.

The difference between the best digital providers in financial services and those from the majority of legacy financial institutions is that digital-first organizations build digital experiences starting with the customer. Beyond simply providing digital capabilities, the design of digital experiences begins with making internal processes and engagements simple and seamless. More than anything else, COVID highlighted the difference between simply presenting a false digital facade and truly building a strong digital experience.

Consumer Banking Behaviors Changed Forever

As COVID-19 continued in 2020, consumer banking and payment behavior changed dramatically. As many consumers were forced to work from home, financial institutions limited access to lobbies and people continued to be worried about everything touched by others, financial institutions realized that digital banking would move beyond younger demographic segments to become the standard method of financial services engagement for all.

Even when the pandemic subsides, most financial institutions have realized that just because consumers may be able to visit branches doesn’t mean they will. It also became clearer that going back to using cash, checks or point-of-sale systems requiring tactile engagement may not ever return to what it was pre-pandemic.

The move to digital payments and away from cash and checks was not a new trend, but it certainly had not been the overarching trend it became during the past nine months. As evidenced during the 2020 holiday season, consumers are buying products online more frequently than ever. The impact is a tremendously increased use of digital payment options, and reduced POS, cash and check usage.

For most financial institutions, COVID provided a perfect opportunity to reduce physical branch networks, double down on digital banking investment, leverage new technologies, encourage digital payments and partner with fintech firms that can assist with all of these transformations. As financial strains on financial institutions are expected for the foreseeable future, digital alternatives provide a foundation for cost reductions.

For most financial institutions, COVID provided a perfect opportunity to reduce physical branch networks, double down on digital banking investment, leverage new technologies, encourage digital payments and partner with fintech firms that can assist with all of these transformations. As financial strains on financial institutions are expected for the foreseeable future, digital alternatives provide a foundation for cost reductions.

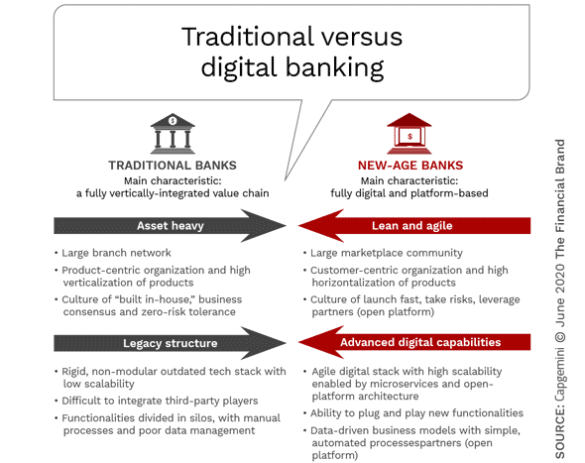

New Digital Banking Models Must be Pursued

The pandemic heightened the urgency for all financial institutions to reassess their existing business models, core systems structure, distribution networks, commitment to innovation and product assortment for a new reality of consumers expecting simplified digital solutions. The new model for banking must also reflect more agile and aggressive competition and shareholders expecting greater efficiencies.

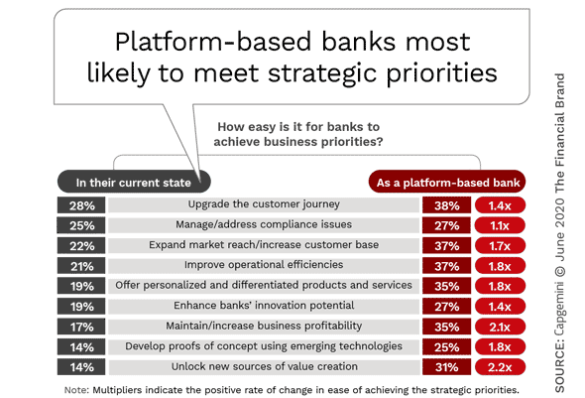

According to the World Banking Report 2020, banks and credit unions that can deliver fully digital, platform-based banking will realize significantly lower acquisition costs, an improved efficiency ratio and much lower costs of distribution. The banking model for the future may also shift to an open banking approach, leveraging third-party solutions, including partnerships with fintech providers.

For those organizations that decide to move to a platform-based structure, there is often the benefit of agility and the ability to create value with an ecosystem of interdependent producers, suppliers and distributors. In banking, the efficiency provided by a platform-based model may also be significant.

While most financial institutions will not go “all in,” many may adopt more of a hybrid approach that will combine third-party products and services with existing products. There are obstacles to moving to a platform model, such as security concerns, legacy systems, and finding the right partners, but the benefits over time could be worth the journey.

Financial Institutions Inept at Using Data and Analytics

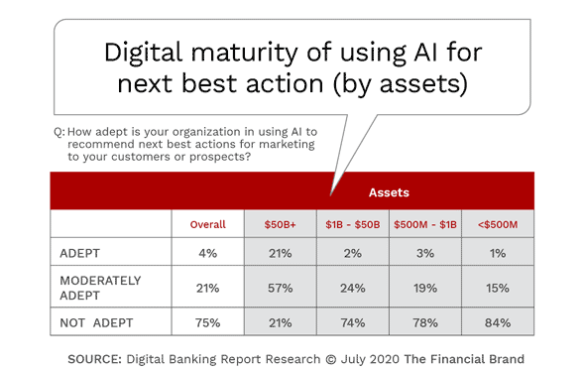

A major concern for banking industry is that it continued to lag most other sectors in the use of data and advanced analytics in marketing in 2020. More concerning is the fact that, except for the largest institutions, confidence in being able to leverage AI tools actually decreased in 2020, according to the Digital Banking Report.

When financial institutions were asked whether they could use AI to determine next best action/offer for customers or prospects, more than 75% of all banks and credit unions globally said they were “Not Adept.” While it was not surprising that 78% of the largest organizations thought they were either “Adept” or “Moderately Adept” at determining what to proactively offer customers using AI, it was surprising that organizations with assets between $1 billion and $50 billion consider themselves to be so much worse.

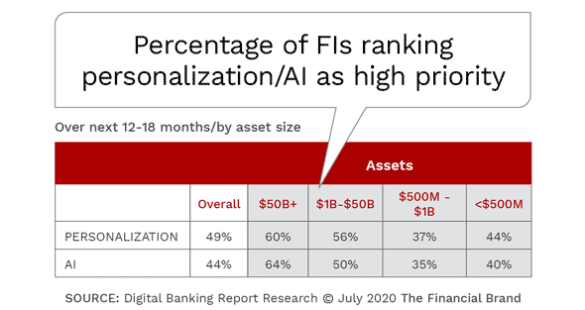

Despite this very low self assessment around the ability to leverage data and analytics for an improved customer experience, only 44% of organizations believed advanced analytics was a high priority for the future. A slightly higher percentage of firms (49%) believed personalization was a high priority. When broken down by asset size, it was clear that the largest organizations placed a higher priority on both personalization (60%) and AI (64%) compared to smaller organizations.

Organizations committing resources to improving their application of data and insights to improved marketing will be in a stronger position going forward. They’ll be ahead of other financial institutions in addressing both immediate challenges caused by the pandemic as well as being able to take advantage of opportunities going forward.

Read More: Data and AI Must Play Bigger Role in Financial Marketers’ Growth Strategies

Digital Banking Transformation Success Elusive

Done well, digital transformation provides immense opportunities for increased internal efficiencies and improved marketplace competitiveness. But, the challenge is that the process of digital banking transformation touches many areas of the organization, requiring prioritization of investments. The process also requires ongoing engagement and potential reorganization, because there is not a static endpoint.

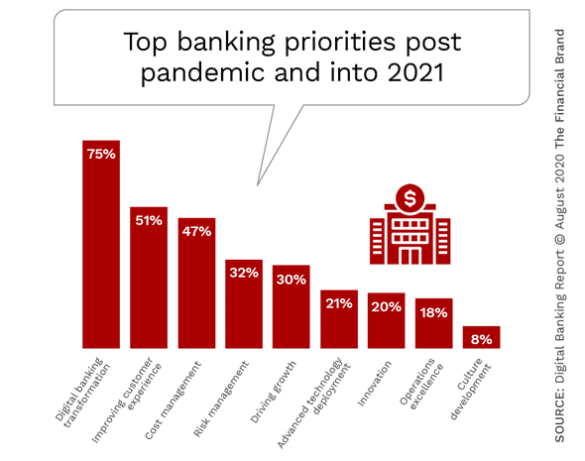

Research by the Digital Banking Report revealed an overarching awareness and enthusiasm around the process of digital banking transformation, with 75% of organizations worldwide citing it as a top three priority for 2020 and into 2021. Of concern however, was that only 21% of the respondents cited “deploying advanced technology” as a priority, with “operational excellence” (20%) and “culture development” (8%) rounding out the bottom three priorities. The lack of focus on technology, operations and culture will ultimately derail most digital banking transformation efforts.

While 75% of survey respondents indicated that digital transformation was a top post-pandemic priority, and the majority understood the importance of the components of digital banking transformation, most organizations were not successfully deploying the strategies needed to succeed. For instance, while an overwhelming 98% of organizations stated that improving the customer experience was either “very high”, “high” or “moderately” important, only 31% stated they were either “highly” or “very highly” successful at doing so. Just over half (51%) stated they were moderately successful at improving the customer experience. Of even greater concern, just over four in ten organizations (43%) considered themselves to have low or very low success with data and analytics.

![]()

Given the paradoxes described, it should come as no surprise that less than 20% of organizations believe they have deployed digital transformation “at scale”, with roughly half of the organizations stating they had ‘partially deployed’ solutions and 27% having ‘limited deployment’. While the largest organizations have a slightly higher percentage than average, so do the very smallest organizations.

Research suggests that the biggest inhibitor to digital banking transformation success is executive leadership commitment of organizational and cultural change. As senior executives and boards of directors hope to transform their organizations for the pandemic-fueled digital age, the culture of organizations must support innovation, the application of data and analytics, increased employee training and the investment in advanced technology to achieve the level of customer experience possible with digital transformation.

Future Winners Defined by Value-Added Experiences

To become a digital banking champion in a post-pandemic future requires more than advanced technology and a cool digital app. The goal is to create an organization that outperforms peers in market value, revenue growth, efficiency (cost ratios), customer satisfaction and even the ability to find and keep talent.

As organizations continued to improve digital functionality after COVID hit, leaders provided end-to-end online and mobile account opening functionality, while also enhancing the experience with several time-saving capabilities and user experience enhancements. From simple data entering, to progress trackers and ‘stop and resume’ functionality, the processes put the customer in control, with speed and ease of use being the differentiator. Digital banking champions also allowed customers to open a much broader array of services digitally, improving cross-sell and up-sell success.

The most progressive organizations also found ways to move ‘beyond banking’, including services ranging from transit passes and retail discounts to credit reports and privacy insurance. These types of enhancements are engagement and loyalty tools that help make using the mobile banking app on the phone or online a daily occurrence.

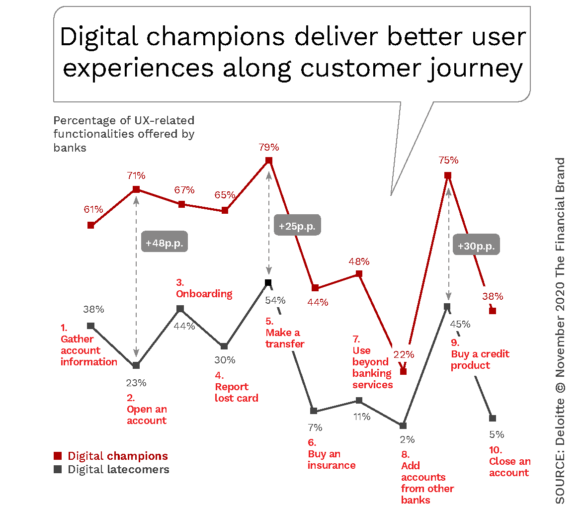

But probably most important, winning financial institutions will find ways to keep a consumer satisfied over time regardless of the channel they select or where they are in the customer journey. As illustrated by the chart below, digital champions in banking outperform at every step of the customer journey.

Read More: The Qualities of Digital Banking Champions

While 2020 was an unprecedented time of change and disruption, change will not stop in 2021. In fact, even as the impact of the pandemic may become clearer and less disruptive, other marketplace changes will continue or even become more impactful. As organizations move into 2021, the importance of an exceptional user experience will become even more significant. These experiences (both digital and traditional) will need to be supported by data, advanced analytics and an overarching institutional focus on building solutions from the inside-out, with the customer being at the center of the development process.