The unexpectedly rapid increase in use of digital banking channels as a result of the COVID-19 lockdowns, and the ongoing desire for social separation and less contact, has left banks and credit unions with a two-fold challenge.

First, they need to better understand what’s transpired — and how much of it is going to stick.

Second, having more or less been sucked into a digital vortex by unexpected events, they have to decide what they will do going forward.

Even at the country’s largest bank, JPMorgan Chase, there are more questions than definite answers. At the Barclays Global Financial Services Conference 2020, Jen Piepszak, Chief Financial Officer, was probed concerning the influence of the COVID-19 period on its digital versus physical strategies. The questioner pressed this in part because pre-COVID the megabank was pursuing aggressive branch expansion in new markets including setting up flagship branches in certain markets.

“It is true that we’ve done some reprioritization to accelerate certain things in terms of our digital capabilities, … given customer needs through the crisis,” said Piepszak. “But broadly speaking, we haven’t changed our priorities.”

Then she added this regarding the bank’s branch footprint: “We won’t make any decisions before we’ve had the benefit of really learning everything we can and listening to our customers. But it is possible that we accelerate some of our de-densification plans … in certain markets while we continue to expand to new markets.”

The nation’s largest bank may be treading the path towards greater digitization with some caution, but research reports from BAI and from Visa subsidiary Plaid make it clear that greater reliance on digital channels will continue after the worst of COVID and that institutions ignore the pandemic shift and the underlying, ongoing trend at their peril.

The months ahead represent an opportunity to learn and adapt from a trial by COVID. “BAI found that half of consumers are using digital products more since the pandemic’s arrival, and that 87% of them are planning to continue this increased usage after the pandemic,” says Karl Dahlgren, Managing Director. He explains that this can be built upon.

“Through this increased usage comes visibility into customers’ needs and expectations,” he explains. “This will most likely result in priorities being reviewed, adjusted and possibly changed.”

BAI’s research looked at use of bank and credit union digital services, while Plaid’s research examined rising use of fintechs’ apps during the pandemic. BAI’s study also found that a brake on further digital progress is fear — not fear of COVID, but fear of fraud. A good quarter of consumers remain digital late adopters, with many reasons to hang back, including fraud concerns.

Use of Both Financial Institution Digital Services and Fintech Apps Rise

Americans stepped up their use of fintech apps as the pandemic intensified over the summer, according to Plaid’s research.

“The majority of Americans used fintech before the crisis, but COVID-19 accelerated adoption — during the pandemic, people used more fintech apps, more frequently and for more financial tasks,” Plaid’s report states.

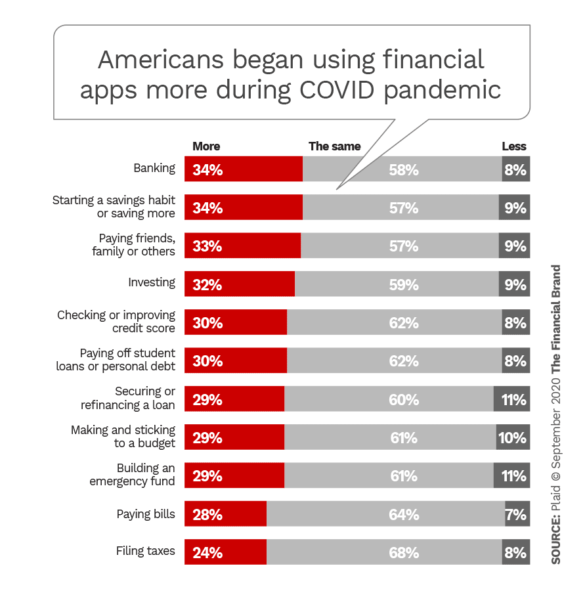

Overall, 59% of Americans use more apps now to manage money than pre-COVID-19. This usage covers a wide range of financial tasks, led by increased handling of daily banking, but bringing in many more money matters, as described in the chart below.

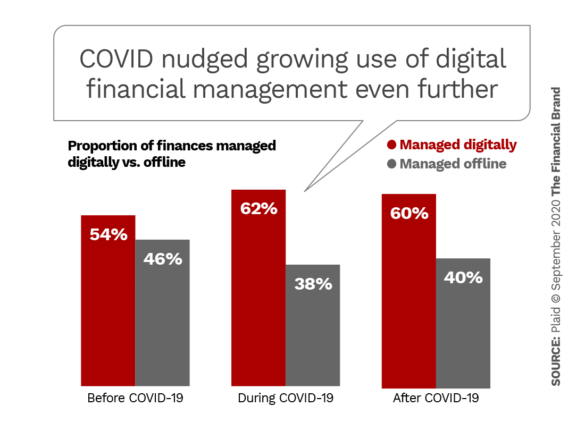

Two-thirds say that they will continue making more use of fintech apps post-pandemic. More specifically, a shift made during the height of the lockdown period is continuing, with more consumers using fintech apps to digitally manage their affairs than was the case prior to COVID-19.

Not only are Americans using fintech apps more frequently in COVID’s wake, they are using more apps. About half of the sample reported that they are now using three or more fintech apps. And a significant minority of people who use six or more fintech apps rose from 8% before the crisis to 14%.

The study also found that 57% of the sample cited time savings and 42% cited cost savings. In addition, on multiple levels use of apps reduced stress and fear of managing funds during the crisis for 37%, according to the report.

Regarding traditional banks and credit unions, as noted earlier, over half of the BAI sample found that people were using their institution’s digital services more. Interestingly, while fintech apps benefit from attractive design and a strong customer experience, generally, the BAI research found that people who leaned more heavily on their banking institutions during the crisis found a positive experience, frequently.

Seven out of ten consumers told BAI that they figured out the services on their own, while 23% used videos and other online tools that their primary financial institution made available. Only 9% indicated that they had to call for help or just gave up.

BAI’s research did a bit of myth busting, according to Dahlgren. “Responses on learning how to use digital services were consistent across all generational cohorts,” he says. “In fact, Boomers who found the digital banking experience intuitive came to 81% — suggesting that stereotypes about older consumers and technology simply are not true.”

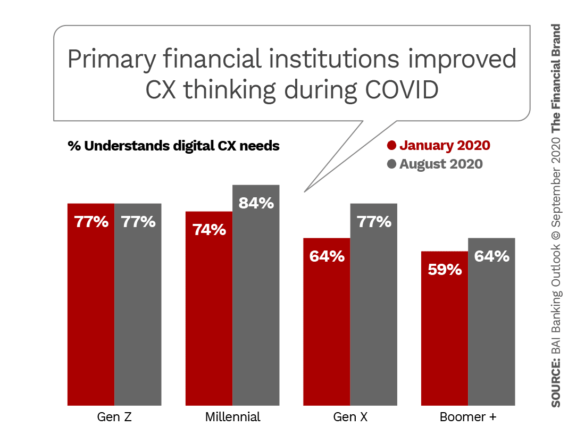

Banking institutions’ digital services received strong ratings, picking up in all cases but one — Gen Z — in the wake of COVID. BAI compared a pre-COVID survey’s ratings with an August 2020 survey and found that even in the case of Gen Z, ratings were quite strong.

Read More:

- Digital Transformation Success Elusive For Financial Institutions

- Digital-First Banking Doesn’t Mean Chasing Every Fintech Innovation

- 5 Digital-First Strategies That Can Turn Banks Into UX Disruptors

- Fintech Buys Bank in Pursuit of Radical New Business Model

Direct Banking Enjoyed an Edge as COVID Ruled the Economy

A factor in digital adoption noted in both research studies is that consumers already using direct banks contributed to the strong showing by those institutions in increased digital usage during the pandemic. Here’s how four banking categories saw digital usage increase:

- Direct banks 67%

- Large banks 59%

- Regional banks 48%

- Community banks/

Credit unions 28%

Direct banks also received the highest ratings for understanding the CX needs of consumers:

- Direct banks 89%

- Large banks 77%

- Regional banks 76%

- Community banks/

Credit unions 61%

At first, this strong showing by direct banks seems a bit circular — digital is what direct banks like Ally do, by definition. Dahlgren agrees that this is a factor, but points out that direct banks already tend to have an appeal to younger consumers and that those people tend to be early adopters. Consumers of all ages were looking for touchless transactions, and direct banks had that down.

While community banks and credit unions came in last in both rankings, Dahlgren suggests they have an opportunity now to close that gap — if they take it.

“By leveraging their close customer relationships and using analytics to understand the most in-demand digital tools, they will be able to focus their strategies on offering the most preferred capabilities first,” he says. Instead of attempting to get the whole job done right away, he suggests prioritizing those areas that past BAI research has shown to be critical. This includes checking account balances, transferring money, paying bills, managing finances and depositing checks.

“Community bank leaders can use these insights to deliver the digital services most in demand while creating a plan to include additional digital offerings in the future,” says Dahlgren. More can be added as time and funding become available.

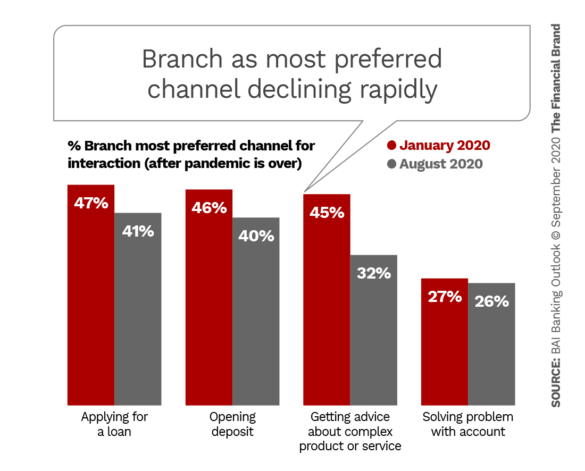

Plans for branches must be tempered by each institution’s experience, with even Chase still studying the implications of COVID. However, BAI’s research made clear that preference for branches is dropping.

Not Everyone Climbed on the Digital Train, But Banks Can Help Latecomers

Even though the banking experience was generally positive, the BAI study found that one out of four consumers surveyed were late adopters of digital services. They tended to give financial institutions’ digital CX the lowest ratings — overall, only 56% felt that institutions understood the kind of experience they wanted.

Dahlgren suggests that COVID was an unforeseen catalyst in the adoption of digital — executives have widely described it as putting them ahead for as much as five years.

“Those leaders who find a way to demystify the digital experience will be the most successful in accelerating their adoption and usage,” says Dahlgren. “That may come in the form of proactive outreach, incentives, video tutorials, testimonials and training.

Fear of Fraud is the Post-COVID Threat Financial Institutions Must Jump On

The BAI research affirmed that while CX is important and digital appealed to the desire for touchless banking, the biggest obstacle to more consumers embracing digital remains the fear of becoming a fraud victim.

Among the generational breakouts in the study, every group exhibited this concern to some degree:

- Baby Boomers 46%

- Gen X 42%

- Gen Z 37%

- Millennials 27%

Dahlgren points out that these worries are strong and that consumers support financial institution action on multiple fronts. For example, previous BAI studies have found that 60% of consumers would feel more secure if financial institutions used factors like fingerprints, retina scans and speech patterns to identify them. And many also support use of artificial intelligence and analysis of big data to verify who they are.

Going forward this is important to remember because BAI’s most recent study found that over half of consumers overall would switch providers for better digital service.

“Leaders should not become complacent because of a current high level of digital banking satisfaction,” Dahlgren warns.