The public’s embrace of mobile wallets has been steady, but not quite up to industry expectation. According to a recent issue of the Digital Banking Report, entitled Digital Payments and Mobile Wallets, acceptance of mobile payment solutions are beginning to explode, however, mostly on the momentum of P2P payment solutions. According to the research, “A recent U.S. Bank Cash Behavior Survey found that 47% of consumers surveyed say they prefer the use of digital payment apps versus cash (45%). In addition, a study from Juniper Research found more than half (53%) of global transactions at POS will be contactless within 5 years … compared to just 15% this year.”

It’s hardly surprising that digital banking offerings would outstrip demand – at first. The public can hardly keep abreast of technological advances, much less the flow of possibilities they present. It’s a market reality that more or less dooms technology to produce solutions in search of problems, and leaves marketers hoping customers will acknowledge the problems and deem the solutions worth paying for.

Consider a device that, a little over ten years ago, solved a couple of problems no one knew existed: how to send text messages, and how to check Facebook with maniacal frequency. Suddenly, the touchscreen smartphone became a necessity. On its heels so did tablets and wearables.

The same devices are now poised to make banking faster and easier than ever. And while digital transactions the likes of checking balances, transferring funds, depositing checks, and paying bills have all become part of the new banking landscape, consumers and businesses are beginning to wrap their minds around and embrace more recent arrivals such as mobile wallets and P2P apps. After all, as far as they knew, until now, they managed to get along without them.

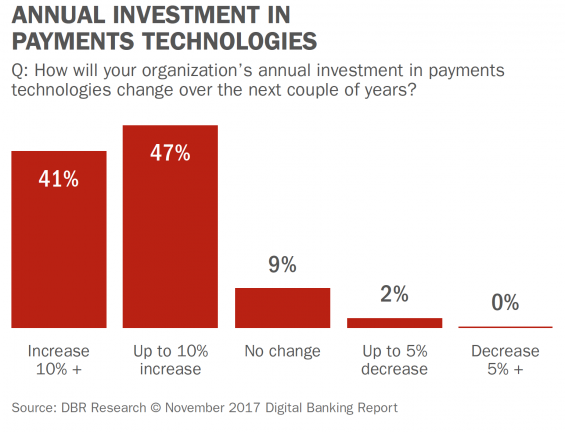

The banking industry realizes that it must adapt to changing behaviors or risk losing the expanding segment of digital consumers. And, while P2P payments have never been about turning a profit, this service is one of the strongest components of increasing ongoing consumer engagement. That is why, according to a recent Fiserv study cited in the Digital Banking Report,

“Organizations are increasing investment in payments solutions mostly to improve the customer experience and to support new solutions, focusing the most on P2P payments, mobile wallets and debit cards. Organizations believe P2P payments and mobile wallets are increasing in importance compared to other payment solutions, with most organizations believing real-time payments and P2P provide significant opportunities in the future.”

No wonder a spate of P2P apps have descended upon the market. “All market indicators point to person-to-person (P2P) use to be the ‘next big thing,’” says the Digital Banking Report. It makes sense. Before P2P, the one transaction digital banking hadn’t replaced was the person-to-person payment. Whether to reimburse a friend for movie tickets, repay your share of a lunch tab, or gift money to a child or grandchild, nothing was quite as convenient as handing over cash or a check. But, with emerging P2P apps making the transfer of personal funds clean, precise, secure, and, above all, easy, cash and checks may soon have to concede the race once and for all.

Not that P2P solutions don’t face a couple of hurdles. One is set-up. Apps that ask for hand-entered personal information and account numbers find themselves at a disadvantage compared with apps that snap a photo of an ID card or use the smartphone address book to keep the heavy lifting behind the scenes. Apps like Apple Pay Cash that only work within a proprietary operating system are also at a disadvantage to apps that work across the Internet of Things (IoT).

Perhaps a larger hurdle is the sheer volume of P2P apps descending upon and splintering the market. When every receipt of funds means downloading and setting up yet another app (that both the sender and receiver of money must both download), cash and checks regain some of their luster. With PayPal or its subsidiary Venmo, there is no need to share a bank, smartphone manufacturer, or operating system. For banks and credit unions, Zelle looks like it might have largely solved that problem with a more universal solution.

Zelle is simple to install and use and doesn’t require an account with a participating financial institution. But, speaking of participating financial institutions, that’s where Zelle’s potential to rapidly expand exists. As CNN Money recently put it,

“You and most people you know probably already have access to [Zelle] because it’s set up to work with your checking account at a participating bank. Have an account with Chase? Bank of America? Wells Fargo? You’ve got Zelle already.”

An impressive roster of participating financial institutions and the sheer numbers of account holders they represent has allowed Zelle to hit the ground running. Right now nearly 40 percent of financial institutions surveyed either offer Zelle or plan to offer it in the next year.

Regardless of which app rises to dominance, as the boundaries between point-of-sale and digital commerce become increasingly blurred, there’s one thing we can be sure of – The ultimate winner in the race to make payments a more seamless, less time-consuming experience will be the consumer.