Mortgage lending stayed healthy in 2021, even with the pandemic, and looks to continue to prosper in 2022. Although there are some worries of a housing market crash, most forecasters predict higher rates and higher home prices as demand continues to rise. However, successfully catering to changing needs of Millennial customers in particular will require digital transformation of the entire mortgage chain, even as upstart mortgage-related fintechs find new ways to exploit the demand.

“Mortgage providers that spent on digital infrastructure capitalized on their investments during the [pandemic] crisis, while those tied to physical paperwork lost new business,” concludes a global survey of financial services professionals by Infosys. “Instead of just surviving, many companies leapfrogged their competitors using new digital capabilities, and those companies will continue to race ahead in this new — and still evolving — mortgage market.”

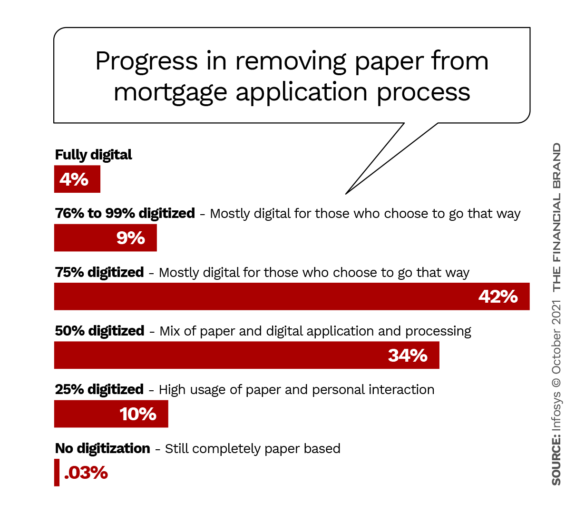

The Home Buying Experience Has Deeply Changed

Ramifications of the pandemic have combined to fundamentally reshape the mortgage-lending landscape. These include the rise and persistence of remote working, relocation out of central urban areas, increasing preference of online options, and the deployment of artificial intelligence applications.

Down with Complexity:

More than just a slick mobile application, today’s consumers expect the full home buying experience to be digital and simpler.

Many prospective first-time home buyers, used to quick and easy online banking, tend to gravitate to a home-buying experience that’s completely electronic. This expectation applies to all the actors involved with home buying: Realtors, appraisers, title searchers, notaries, home inspectors, and, of course, lenders.

“From integrated home buying services, virtual loan officers, digital mortgages, voice assistants, to crowdfunded mortgages and changing Millennial qualifications, the wants, needs, and expectations of customers are changing,” says Aidan Paringer, writing in a blog at bntouch.com. “The mortgage companies that can change with them will be the most successful.”

Rates & Prices: Numbers Tell the Tale

Forecasts for mortgage rates, while obviously not etched in stone, are remarkably uniform. According to a Home Buying Institute summary, Freddie Mac expects the average rate for a 30-year fixed home loan to reach 3.4% by the end of 2021, and 3.8% by the end of 2022. The Mortgage Bankers Association predicts it to reach 3.4% at the end of 2021 as well, but climb to 4.3% at the end of 2022.

Two individual sources cited are in agreement with the institutional predictions: Charles Dougherty, an economist at Wells Fargo Securities, puts the forecast at 3.5% for the rest of 2021 and 3.9% in 2022. And Raymond Sfeir, director of the Anderson Center for Economic Research at Chapman University, pegs the rate at 3.4% and 4% respectively.

Regarding home prices, which have been on a tear for the most part, Freddie Mac predicts them to rise 6.6% in 2021, and then, because of inflation, dampen slightly to 4.4% in 2022. New and existing home sales likely will reach 7.1 million by the end of this year, then decline to 6.7 million homes in 2022.

Looked at another way — from the point of view of real estate investors — the pandemic-instigated upheavals and support programs have combined to present home-buying opportunities. Homevestors Franchise notes that while GDP collapsed by 6.5% in 2020, it’s expected to grow 5% in 2021, and 3.5% in 2022. “A growing GDP can mean three things,” the blog notes. “Fewer distressed houses, higher prices, more activity.”

The Consensus:

Plenty of homebuying upside remains, so purchase loan originations will continue to be strong. But pressure on refis will increase.

Meanwhile, with the Federal Reserve likely to keep interest rates low through 2022, due to employment numbers continuing to lag pre-pandemic levels, the number of first-time homebuyers likely will increase. Homevestors Franchise estimates this to jump from 7.64 million in 2018-2020, to 9.2 million in 2020-2022.

A somewhat different view comes from the Mortgage Bankers Association’s annual forecast, which predicts the rate for 30-year fixed-rate loans will climb to 4% in 2022. However, the association notes that the Fed won’t likely raise short-term rates until the end of 2022. Therefore, MBA expects purchase loan originations to rise 9% to a record $1.73 trillion in 2022.

Mortgage loan refinancings, however, will fall precipitously next year, the association forecasts. Already expected to be down 14% in 2021, refi originations could be down another 62% next year.

Read More:

- How Banks Are Arming to Win the Digital Lending War With Fintechs

- 5 Digital Strategies to Boost Mortgage Lending in a Red Hot Market

New Tools for New Customers

While the demand for owning a home is there, the nature of that demand has changed radically, as well as the need to adjust. Paringer, in the bntouch.com blog, provides this partial rundown:

- Virtual loan officers and lenders will use text messaging and online live chat features more often to provide on-demand service.

- Borrowers using electronic devices increasingly are talking to smart home devices like Siri and Google Assistant using terms such as “near me” and “similar to,” and not typing into search engines. The savvy response by mortgage representatives is to create a seamless presence connecting, for example, a YouTube ad that could prompt the buyer to do a Google Home search for a branch near them, and then read previous customers’ reviews on their text apps.

- Automated follow-up calls are essential, since potential customers now can hop around to dozens of competing options and won’t stick until they get personalized and quick attention.

Other industry observers have noted it has become more common for people to buy a house without physically seeing it first. 3D virtual tours allow buyers to see a lot, although it’s still important to have a trusted agent or friend be on site, giving a home the smell test, figuratively and literally.

Being confronted with, and signing, a huge stack of paperwork is going away too. Younger buyers especially want the closing experience to mirror their house-hunting experience — digital and on their timeline.

The mortgage industry has been pursuing digital transformation for years, “just not always with a sense of urgency,” as Infosys observes. That is changing. “The pandemic has sped up this often-slow corporate metabolism. Out of necessity, companies have accelerated their shifts to new technologies as the global pandemic penalized the physical and rewarded the digital.”

Read More: Banking Must Digitally Transform Consumer Lending

Not Every Mortgage-Related Trend Is Obvious

Some technological imperatives seem unintuitive at first glance, such as the adaptive use of Internet-of-Things. The Infosys survey offers this perspective:

“When property is real-estate owned, the responsibility of maintaining the property falls on the servicer until it is sold. This includes activities such as paying taxes and insurance, adjusting the temperature of the property, and maintaining the water pipeline and gas. The installation of IoT-enabled sensors that connect to energy optimization systems will help the servicer monitor the heating, ventilation, and air conditioning. Better maintenance allows the servicer to sell the property quicker.”

Creative Partnering:

In the fast evolving mortgage business, traditional players and fintechs are hooking up in unexpected ways.

Recognizing the ongoing demand, mortgage-related fintechs are finding new ways to tap into the market. One interesting (and unintuitive), example: American Express announced partnerships with Rocket Mortgage by Quicken Loans, and Better Mortgage, two online mortgage lenders. American Express will give a statement credit of $2,000 to eligible customers who obtain a conforming mortgage from either of these companies. The credit goes up to $6,000 for jumbo mortgages.

According to CNBC, there is no revenue-sharing agreement between the credit card company and the mortgage company — it’s simply a way for American Express to add value to its fee-based card, and thus keep the customer. Meanwhile, presumably, the fintechs get a direct avenue to a broad base of creditworthy potential borrowers.