No term has been more used (and misused) in the banking industry over the past three years than the word “fintech”. Sometimes used as a shortened version of “financial technology” solutions, the term is also used to describe a sector of start-up competitors that are using digital technology, analytics and mobile platforms to make daily banking easier.

Interest in fintech has escalated due to heightened consumer expectations around the digital delivery of financial services, with this interest resulting in massive investments in the sector during the past three years. But the history of fintech goes much further back than just the last three years, with many arguing that some of the industry’s largest providers have been delivering financial technology solutions for decades.

To review the current state of the fintech marketplace, the potential impact on the industry, how consumers will respond, and business models that may prevail, Capgemini and LinkedIn, in collaboration with Efma, conducted a survey of over 8,000 consumers in 15 countries, along with 100 interviews with senior-level executives guided by an Executive Steering Committee. The result was the World Fintech Report 2017, that is considered to be the most extensive review of the sector to date.

The Rise of Fintech

The rise of interest in fintech has been caused by increasing unmet consumer demands for digital banking solutions fueled by digital advances in many other sectors (retail, hospitality, travel, etc.). These demands, combined with reduced barriers to entry in some markets, have improved the availability of funding for the sector, which has driven growth even further.

According to the study, 50.2% of banking customers across the globe are using the products or services of at least one fintech provider. In addition, it was found that tech-savvy consumers are supplementing traditional banking services with fintech solutions at twice the pace as less tech-savvy consumers (67.3% vs. 33.6%).

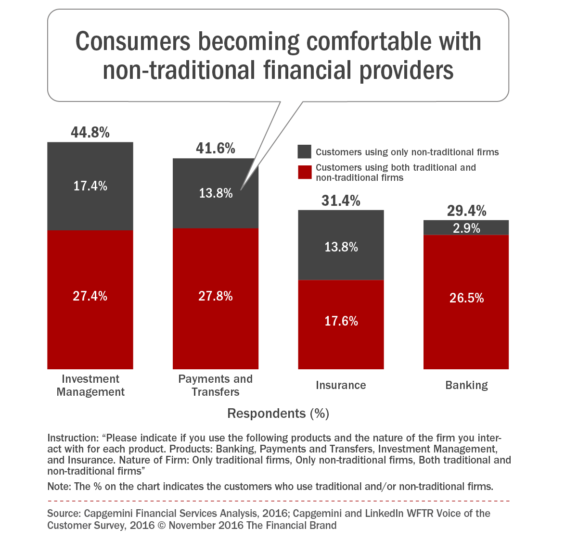

As shown above, fintech firms have made the greatest impact in investment management, where 17.4% of consumers use only fintech providers and another 27.4% use them in addition to a traditional provider. With so many fintech solutions, the report also found that 46.2% of consumers are using solutions from more than three fintech providers. This disaggregation of financial solution providers could threaten traditional banking loyalty or provide an opportunity for bringing together multiple solutions under one roof (platformification).

As would be expected, fintech providers are the most popular with younger, tech-savvy, and affluent customers. This is because fintech firms are viewed as being easier to use and a better value for the money. That said, most fintech providers operate within a narrow slice of the value chain (lending, investing, PFM, etc.) with only a few providers trying to take on the entire banking relationship

Finally, emerging markets have some of the highest adoption rates, with China (84.4%) and India (76.9%) having the highest acceptance, ahead of the UAE (69.6%). Usage by consumers in the UK (48.8%) and the US (45.8%) was about average for the more developed countries surveyed.

The Legacy Banking Advantage

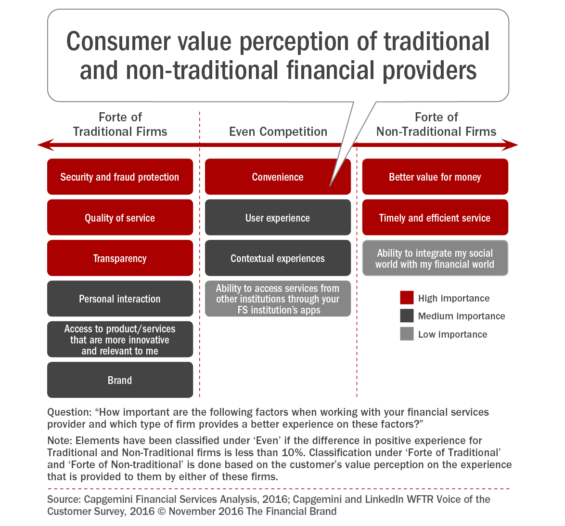

While fintech firms usually have the “first mover’ advantage, delivering customer-centric solutions at a low cost, without the burden of legacy infrastructure, they still lack scale in most cases. This is because traditional financial organizations continue to be viewed positively by consumers in the some of the most important foundational areas such as trust.

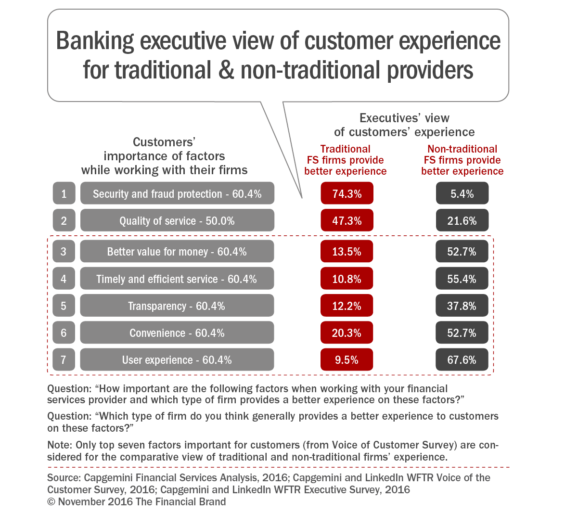

Only 23.6% of consumers say they trust their fintech provider compared to 36.6% for traditional firms. Consumers also noted that legacy financial institutions hold an advantage over fintech providers when it comes to fraud protection, quality of service, and transparency.

“Rising customer expectations for more personalized and advanced digital experiences, advancements in technology, greater access to venture capital, and lower barriers to entry have created fertile ground for growing fintech firms,” said Penry Price, Vice President, Marketing Solutions, LinkedIn. “Fintech firms are largely gaining momentum by meeting needs traditional players have yet to address, but many fintech providers lack the transparency required to earn the trust of their consumer audiences to capitalize on these opportunities. ”

It should be noted that both traditional and non-traditional financial service providers are struggling to keep up with the demands of the increasingly digital consumer. It is thought that using advanced analytics to better understand the consumer and deliver personalized solutions will ultimately determine the winners and the losers.

Delivering Positive Moments of Truth

While the CapGemini/LinkedIn research found a disappointing level of overall consumer satisfaction (31.1%) with both legacy and emerging fintech solution providers, the mobile channel was seen as an opportunity for improvement and differentiation. Overall, the computer was deemed the “most important” channel (56.8%), followed by the phone (45.4%), branch (43.4%) and mobile (40.1%). The mobile channel also had the lowest rated experience.

There is an opportunity though, since mobile was found to be the second most important interaction channel (after the computer) for the important Gen Y (47.6%) and the tech-savvy (56.5%) consumer. This illustrates the importance of making development of the mobile channel a high priority.

The study suggests that one way to increase satisfaction and loyalty is to capitalize on Moments of Truth. These are best represented by both life events (marriage, new child, house purchase) as well as important day-to-day interactions. These include the ease of opening an account digitally or the seamless way a transfer of money occurs. In the research, these moments of truth also included contextual engagement and proactive advice.

The top 5 Moments of Truth identified were:

- Transparency of fees (74.6%)

- Quick account opening (71.8%)

- Ability to update account details digitally (70.6%)

- Anytime, anywhere access to aggregated account/relationship information (66.9%)

- Real-time updates on problem resolution timetable (66.7%)

These moments of truth differed between retail banking, payments, investment management and insurance customers.

Traditional Organizations Struggling with Innovation

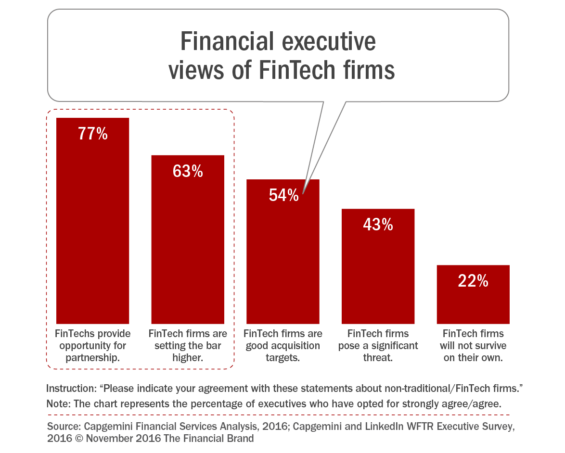

Close to two-thirds (62.7%) of executives at traditional firms said that fintech firms are setting the bar higher for all financial institutions. While 43.1% of these executives thought fintech firms posed a “significant threat”, 22.4% believed fintech firms would not survive on their own. More than three-fourths (76.7%) of those interviewed believed fintech firms provided strong partnership opportunities.

The report found that traditional firms are increasingly pursuing a wide range of strategies in response to fintech firms. A majority of financial institutions (60%) now view fintech firms as potential partners, but nearly the same percentage (59.2%) are also actively developing their own in-house capabilities.

Beyond partnership and in-house development, executives are exploring a full range of models, whether it be investment in fintech (38%), partnering with educational institutions (34.3%) or setting up accelerators (29.6%), while a much smaller percentage (18.6%) are acquiring fintech firms.

Executives at traditional financial firms believe their fintech counterparts provide a better experience in most areas of interaction. This includes areas such as convenience, ease of use and transparency, and value.

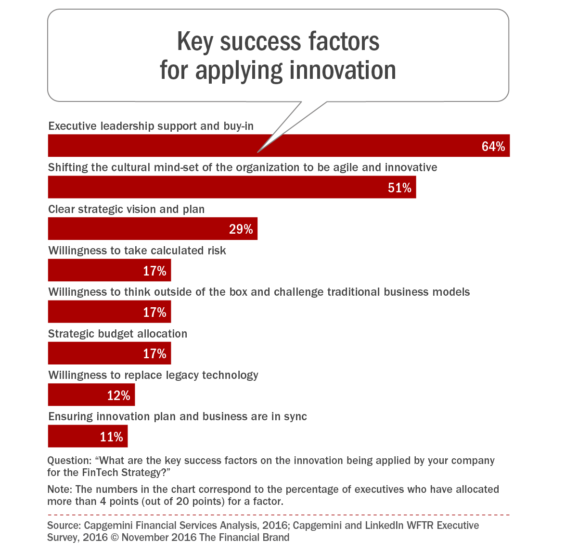

Traditional financial institutions continue to face challenges, with less than half (44.0%) of executives at legacy financial firms confident in their fintech strategy. This is not surprising given only about one-third (34.7%) affirmed they have a well-structured or proactive innovation strategy in place that is embedded culturally. The risk-averse nature of traditional firms also makes it difficult for them to create cultures that prioritize innovation, and 40.3% of executives said that theirs is not conducive to innovation.

“Financial services senior executives are seeing fintech firms in a whole new light as they see greater opportunities to collaborate, but are also making significant headways in building more agile, in-house fintech capabilities.” said Thierry Delaporte, Head of Capgemini’s Global Financial Services Business Unit. “With the exception of a handful of industry leaders, most firms are struggling to achieve positive results from their innovation initiatives with only 10 percent of executives stating they have been very effective at achieving desired innovation results.”

Nearly 90 percent of executives report they are most focused on implementing big data and analytics, followed by the Internet of Things (IoT) (55.8%), blockchain (54.7%), robotic process automation (52.3%), and open API technologies (50%). Blockchain technology has numerous applications including enhanced transfers of digital assets, identity management, and better management of reward and loyalty solutions.

The Uncertain Future of Fintech

“Both fintech and traditional firms still have work to do on delivering a better customer experience,” said Vincent Bastid, Secretary General, Efma. “The arrival of fintech firms has accelerated the improvement of overall customer experience in the industry, but it is still not at the level that customers perceive that it should be. It is only a matter of time before the big technology companies and players in e-commerce and telecommunications join in to stake their claim to benefit from this industry disruption.”

According to the report, traditional financial services firms can unlock innovation by:

- Discovering new technologies

- Devising ideas and insights into business models

- Deploying aligned executives to support innovation

- Sustaining innovation by improving efficiency and implementing best practices

As stated above, one of the most important keys to success in the future will be a change in legacy culture and the buy-in and support at the top of the organization. This is a major paradigm shift for an industry that has taken pride in moving slowly and meticulously. This does not mean that organizations should not understand risk and security elements, but it down mean that they need to become much more agile and open to change.

In the end, it is most likely that “fintech” as a segmented concept will be absorbed within the overarching category of innovation in the banking industry. This is not to diminish the importance of financial technology, but to acknowledge the importance of providing a seamless integration of solutions for the consumer benefit. As the concept of open APIs and “platformification”of the industry continue to gain momentum, it will be more and more important for all financial organizations to focus on the digitalization of delivery using advanced analytics for an improved customer experience as opposed to worrying about nomenclature.

About the World Fintech Report 2017

The World Fintech Report 2017 was guided by an executive steering committee from a mix of biggest traditional, non-traditional and industry expert firms. It was developed by Capgemini and LinkedIn, in collaboration with Efma and includes deep insights into “Moments of Truth” for customers on their customer experience with traditional firms and fintech firms using the results of a survey of 8,000 customers in 15 countries. The report utilized executive roundtable discussions, Agents of Change interviews, as well as numerous other interviews to discuss the impact on the industry as it faces disruption along with opportunities for new collaboration and innovation.