If credit unions had a theme song, the tune for these times might just be Happy Days are Here Again. After all, credit unions’:

- Auto lending volume is at a record level, exceeding $100 billion;

- Share of the mortgage market has quadrupled since 2006; and

- Total income hit an all-time high in 2015.

Not that I’m looking to rain on anyone’s parade (a reference I’m guessing only those of us over 50 will get), but smart strategic planners will always be looking for potential threats and challenges. Here are the three mid-sized banks and credit unions should be planning for:

- Fintech startups capturing the convenience position;

- Merchants attacking traditional deposit behavior; and

- Megabanks capturing the Millennial market.

Together, these challenges are squeezing mid-sized institutions. Escaping the squeeze will be a strategic priority for mid-sized financial institutions over the next five years.

Squeeze #1: Fintech Startups Carving Out the Convenience Position

Consider the following:

- Applying for a mortgage? If you are, you’ve probably seen the ads from Rocket Mortgage, whose tagline is “push a button, get a mortgage.” According to a recent press release from the company, two-thirds of the firm’s volume is first mortgages, and roughly 70% of that is from first-time applicants. Still think online mortgages are only for those who’ve already been through the process?

- Want to refinance your student loan? SoFi touts its 15-minute student loan refinancing process. The five minutes it takes refinancers to upload their documentation is actually the most-time consuming part of the process.

- Need a small business loan? A 7-minute quickie with Kabbage can get you $500 to $50,000. In response to this, American Banker wrote, “speed is one reason why small businesses have been turning to marketplace lenders rather than to banks.”

Are these fintech startups making good business decisions in the blink-of-an-eye timeframes they’re making lending decisions in? I don’t know, although I’m inclined to say no.

But it’s not so much the threat of lost business that traditional financial providers should be most concerned about — it’s market positioning. Fintech startups are capturing a market position that is important to a large and growing number of consumers: the “most convenient” position.

It never ceases to amaze me how delusional traditional providers can be when it comes to the concept of convenience.

One bank in my area claims to be the “most convenient” bank because it has extended branch hours. In all fairness, that probably does qualify the bank as being “most convenient” — in the minds of 0.001% of consumers.

A number of credit unions I’ve worked with recently also claim “convenience” as their point of differentiation. When pressed to quantify (or even explain) that differentiation, the responses were lacking.

Convenience (as a strategic differentiator) is driven by demographics. Younger consumers — without complicated financial lives, without a lot of money to manage and invest — value convenience over service and advice. With the influx (more like tsunami) of Millennials into the market over the past 10 years, convenience has become the dominant basis of competition.

Fintech startups are establishing the bar for convenience. Pundits like to say that firms like Uber and Amazon are the ones setting expectations, but I really believe that consumers’ points of references are those within an industry, not across industry lines.

Are these startups making bad lending decisions? Consumers don’t care. All they see is that the process takes a tenth of the time and effort that it does with traditional financial institutions. And when the “customer experience” is all about the application and onboarding processes — because service and advice aren’t as important to applicant at this stage in their financial life — the firms with the fastest/easiest process become the “most convenient” in the eyes of consumers.

Being perceived as the slow laggard in the market is not an enviable position. But that’s where many traditional financial institutions are these days.

Squeeze #2: Merchants are Attacking Traditional Payments Deposits

The whole Durbin Debacle was about interchange. It wasn’t hard for them to do, but merchants convinced misguided politicians that banks were ripping off consumers with interchange fees. So the rules were changed, and debit interchange fees were limited (for $10b+ banks, at least).

Then, some large merchants decided that wasn’t enough and banded together to form MCX, a consortium who primary purpose was not to provide any value to consumers, but simply to screw over Visa (if you don’t believe me, see this, and scroll to the end of the post).

Didn’t matter, it was short-sighted thinking on both the politicians and merchants parts.

What they seriously missed was the change in consumers’ payments behavior away from debit cards towards credit cards. So much for the benefits of interchange regulation.

One merchant succeeded beyond its wildest dreams (ok, maybe not) in controlling interchange costs: Starbucks. Thanks to the success of their loyalty card, I’ve estimated that they save about a quarter of billion dollars a year in interchange (it’s true they still pay fees on the card loads, but that can’t possibly be more than 20% of the total they’re actually saving).

While other merchants dithered around with that MCX thing, SBUX was saving real money.

But the real — and longer term — impact of what Starbucks did (and is doing), isn’t about interchange. It’s about how it is changing how consumers manage their money.

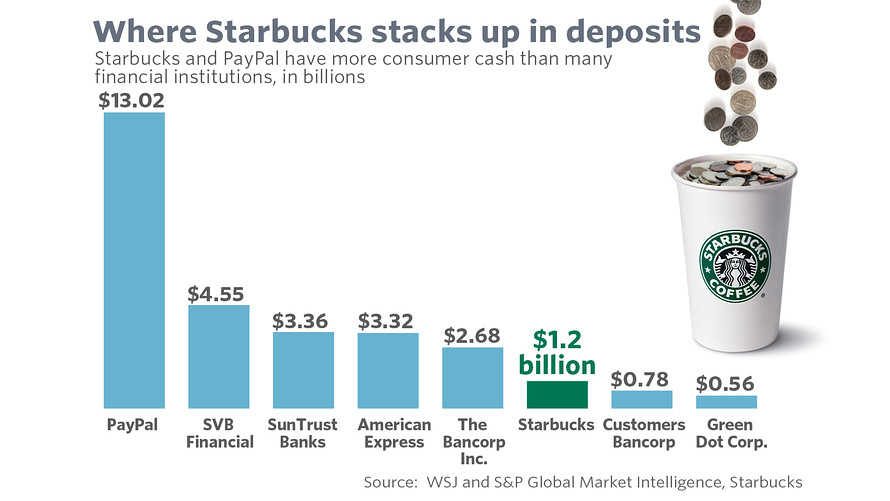

The Wall Street Journal reported that SBUX has $1.2 billion in deposits.

I had heard that the company had $5 billion loaded on their cards, but no matter. What’s important, here, is that this represents the new behavior in how consumers manage their money. Paychecks get deposited in a bank account, then some portion of it quickly gets moved to loyalty and closed loop prepaid cards.

Regardless of how much SBUX has in deposits, one thing is for sure: It’s money banks don’t have to lend out.

And more and more merchants (see the recent announcement from CVS) are playing this game.

Community banks that look at the retail business as just a funding arm to gather deposits for their commercial lending business should be the most concerned financial institutions. I don’t know how easy it was for them to gather deposits in the past, but the new — and future — reality is that retail deposit gathering is, and will be, an increasingly tough game.

Merchants started off attacking the traditional payments model. The result is (and will increasingly be) a change in deposit behavior — squeezing mid-sized banks’ and credit unions’ deposit-gathering efforts.

Squeeze #3: Megabanks are Winning the Millennial Market

Banker from mid-sized banks or credit unions who believe that young consumers still hate big banks should get (playful and gentle) slaps upside their heads. It’s not 2008 anymore, delusional bankers!

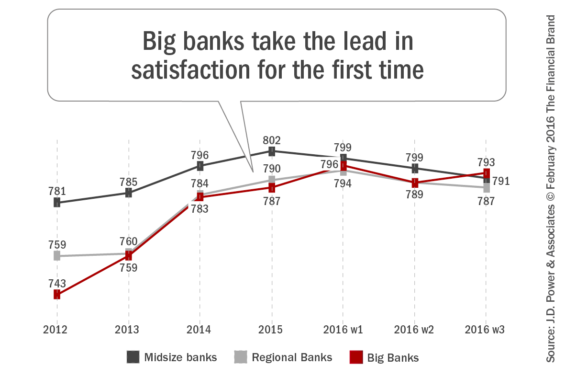

In JD Powers’ tracking of Millennials’ satisfaction with banks, score for big banks now exceed the score for mid-sized and regional banks.

But satisfaction isn’t the only way that megabanks are winning this game.

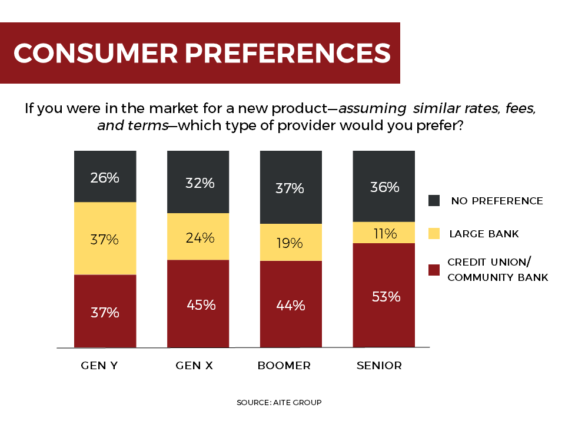

When asked what type of FI they’d prefer to do business with, Gen Yers were just as likely to say they’d prefer to go with a big bank as they would a community bank or credit union. It’s actually the older consumers who prefer the smaller institutions.

What’s driving satisfaction and preferences with and for large banks? For the first time, the answer is not branch proliferation. It’s mobile. And mobile = convenience.

What’s driving satisfaction and preferences with and for large banks? For the first time, the answer is not branch proliferation. It’s mobile. And mobile = convenience.

Mid-sized financial institutions relying on their supposed superior service capabilities will find themselves squeezed by megabanks.

Escaping the Squeeze

Unstrategic strategic planners are “planning” for 2017. They’re focused on how to maintain the growth in loans and checking accounts they’ve experienced over the past year or so.

Strategic strategic planners are looking further out and asking “what could screw this up?” and “what do we need to do about it now so we’re positioned for it when hits?”

If this weren’t already a post that has gone on for too long, I’d spend more time and space answering the question: “What do mid-sized financial institutions need to do to escape the squeeze?”

There’s not enough room here to elaborate, but here are two responses to that last question:

1. Reinvent marketing. Another thing that never ceases to amaze me is how mid-sized financial institutions think they can compete — from a marketing perspective — with the larger financial institutions. A good rule of thumb in banking is that financial institutions spend about one-tenth of one percent of assets on marketing. That means the typical megabank has a marketing budget of $1.3 billion. Do you really think you can out-market that kind of spending? You can’t. You have to use other tactics.

2. Own the financial health position. I know it’s hard to believe, but 10 years from now, the oldest Millennials will be in their mid-40s. And a huge chunk will be in their mid-30s. What that means is that they’ll be moving of the life stage that puts a premium on convenience and into a stage where advice and guidance becomes more important. That trend has always been a boon for brokerages, financial planners, and asset managers. The new opportunity is how to capture that business from a banking (vs. investment) perspective. I’ve been harping on the notion of measuring/managing financial health as a basis of competition for a while now. Get with the program mid-sized financial institutions!