At a time when the number of strategic challenges facing the banking industry seem overwhelming, prioritizing what needs to be focused on is an important exercise. To find out what the most important priorities will be in 2017, the Digital Banking Report surveyed over 500 financial institutions globally as part of the research done for the 2017 Retail Banking Trends and Predictions report, sponsored by Kony, Inc.

At a time when the number of strategic challenges facing the banking industry seem overwhelming, prioritizing what needs to be focused on is an important exercise. To find out what the most important priorities will be in 2017, the Digital Banking Report surveyed over 500 financial institutions globally as part of the research done for the 2017 Retail Banking Trends and Predictions report, sponsored by Kony, Inc.

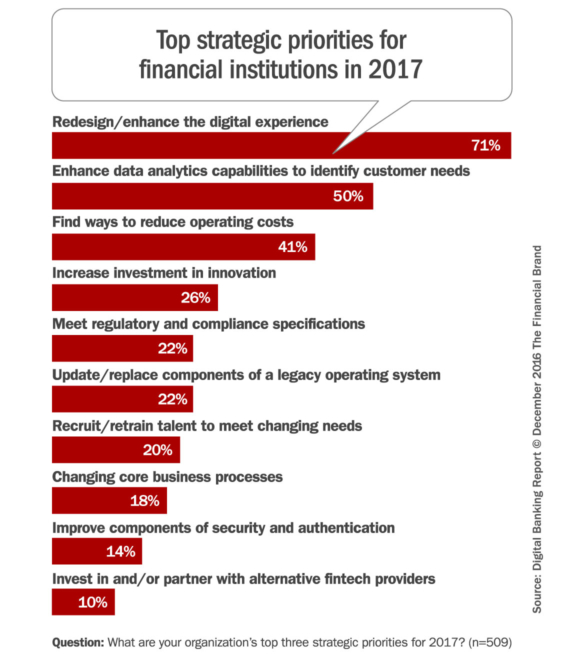

The respondents included included banks and credit unions in every asset range from Asia, Africa, North America, South and Central America, Europe, the Middle East and Australia. Each respondent was asked to provide their top 3 strategic priorities for 2017. Despite the wide variance in both asset size and geographic location of the respondents, the ranking of the top priorities named by the majority of organizations were surprisingly consistent.

Overall, the top three priorities mentioned were improving the digital experience (mentioned by 71% of the respondents), enhancing data analytic capabilities (50%), and finding ways to reduce costs (41%). The rest of the priorities mentioned were at least 15% less likely to be mentioned. Interestingly, despite a great deal of coverage in industry publications, the desire to partner or invest in fintech relationships is a low priority for all but the largest organizations.

1. Improve the Digital Customer Experience

As was mentioned in Are Banks Really Committed to the Customer Experience, “As consumers increasingly make decisions based on the ease with which they can interact with their financial institution, competition around the customer experience is giving rise to new roles and titles within the banking industry.” The challenge has been that, while a majority of financial services firms are in the process of expanding their CX projects – especially as it relates to both digital and mobile engagement – there is still difficulty in gaining resources to pursue new projects.

In addition to applying resources towards improving the customer experience, institutions will need to determine how they will measure success. To date, there is a wide variance in methods used, including measurements around satisfaction, retention, loyalty, engagement and/or some form of revenue metric.

More than any other priority, improving the customer experience was the most consistent in level of mentions across asset categories, type of organization and location.

Get the 2017 Retail Banking Trends Report

2. Enhance Data Analytics Capabilities

Customer insight and data analytics is at the foundation of virtually every retail banking trend in the coming year. From removing friction from the customer journey, to improving multichannel delivery and exploring the use of open APIs, data is the fuel that will power these initiatives.

Despite the vast amount of data available to financial institutions, most organizations are having a difficult time determining what data will have an impact and how to harness the full potential of insight collected. According to research from the Boston Consulting Group, some of the reasons for falling short of potential include:

- Competing priorities. As noted above, there are a lot of priorities … some of which may change over the course of a short period of time.

- IT complexity. Because of multilayered systems and siloed data, FIs rarely use the full breadth and depth of data at their disposal (or know what data to use).

- Lack of coordinated vision. This can result in a sub-optimal allocation of human and technical resources and limited interaction and exchange of ideas.

As noted in the article, Data Analytics Critical to Success in Banking, The risk of falling behind in leveraging consumer insights has never been greater since consumer expectations are rising. The majority of these expectations are being set by non-financial competitors.

In the survey, credit unions were the most likely to mention data analytics as a strategic priority. Community banks were the least likely to mention this as a priority.

3. Reduce Operating Costs

Due to razor thin interest rate and operating margins, a lot of time and effort has been spent by financial organizations to cut costs wherever possible. Sometimes these efforts have been done without understanding the impact on the customer experience or without fixing underlying process flaws,

According to Bill Heitman, founder of The Lab, “Installing new digital banking technology (in the interest of cost savings) doesn’t help much unless the routine processes that are being automated are first closely examined and streamlined – applying the principles of “industrialization” and efficiency management to processes and operations.” Without a review and revamping of underlying processes, any digital banking initiative will fall short of full optimization and, at worst, simply automate already dysfunctional processes.

While all types of organization found the reduction of costs to be the third most important priority, large national banks and community banks ranked this higher than other types of organizations.

4. Increase Investment in Innovation

While investing in innovation was the fourth most mentioned priority by financial institutions internationally, the frequency of mention was 15% below the mission of reducing operating costs and 45% less than the emphasis on improving the customer experience. This is reflected in the 8th Annual Innovation in Retail Banking Report from Efma and Infosys Finacle, where the proportion of banks with an innovation strategy increased only marginally in 2016.

The areas where most banks are increasing innovation investment are customer service/experience (84%) and channels (82%), followed by processes (67%), products (63%) and sales and marketing (56%), according to the Efma study.

In research fielded by the Digital Banking Report, the percentage of mentions was almost uniform at 25% among the different organization types and asset sizes.

5. Meet Regulatory and Compliance Requirements

In the past, many organizations have operated in reactive mode regarding regarding regulations and compliance, only changing in response to regulatory orders, examination comments, or other types of intense regulatory pressure. However, a many organizations have begun a shift towards a more proactive approach to regulatory strategy – establishing a stronger link to business strategy.

According to Deloitte, “By identifying connection points between your regulatory and business strategies – instead of managing regulatory strategy as a side activity – an organization can discover ways to achieve common objectives more efficiently and align compliance activities with your organization’s broader goals.” This strategy creates a win-win, answering compliance issues while improving business performance.

While only 13% of credit unions mentioned regulations and compliance as a priority, 30% of large regional banks and 27% of community banks mentioned regulations as a priority.

6. Update or Replace Components of the Core Operating System

Now more than ever, there is a need to organize each financial institution around customer data, and then to leverage that data through the cloud to mobile devices and apps. The only way to achieve this is to completely rip out the old systems and replace them with a new core banking system that can support the bank, and the customers.

To quote a good friend and financial industry scholar Chris Skinner, “Changing core systems is like changing the engines on an aircraft at 15,000 meters … you just don’t do it. But, more and more banks are doing just that.” What is interesting about this quote is that it came from a great article he wrote… in April of 2013!

“You cannot restructure a bank around customer data if you have that data locked into heritage systems that are product siloed and channel hand-cuffed,” continued Chris. Bottom line, it is not a question of if banking organizations will be changing core operating systems, but when. And, if you follow Chris’ writings, you are probably at least a few years late getting started if you aren’t doing so already.

Not surprisingly, the largest national and regional banking organizations were 10% more likely to indicate that replacing or updating their core operating system was a high priority in 2017.

The largest organizations were the most likely to mention updating core operating systems as a priority, with 25% or large national banks and 28% of regional banks indicating an emphasis. Only 18% of community banks or credit unions found this as a priority for 2017.

7. Recruit and Retrain Talent

The banking industry is changing quickly, with a requirement to meet the needs of a digital consumer. Unfortunately, most legacy bankers, who have long established careers, are not familiar with many of the nuances of the digital banking consumer. There is a need for a new wave of digitally aware and technology adept employee.

Banking’s ability to recruit the ‘best and the brightest’ has never been tougher. Candidates want to work with innovative companies, with the desire for training and development being placed ahead of money. To succeed in the future, banking must win the talent wars.

Banking organizations need to have a cultural shift that requires a buy-in from the board and senior management. Executives will need experience in transformational change and boards must have non-executive directors who understand agile cultures.

According to Stuart Hall from Tyzack Partners, “Building a focused and flexible workforce will enable banks to seize the opportunities that will come from developing an organization that is not only customer-centric and digitally capable, but also flexible enough to regularly re-tune its brand both internally and externally.

The largest organizations appear to be ‘winning the talent wars’, with less than 10% mentioning talent as a top 3 priority in 2017. Alternatively, 36% of community banks and 23% of credit unions believed this to be a top priority.

Get the 2017 Retail Banking Trends Report

8. Improve Business Processes

As mentioned earlier, installing digital banking technology to improve front and back office operations will not lead to optimal results unless the routine underlying processes that are being automated are first closely examined and streamlined. Although many organizations have been successful in automating applications, fewer have achieved high levels of automation in middle- and back-office processes.

Many organizations have embraced lean process redesign. More needs to be done to achieve completely paperless processes, improved workflow tools, and automated task management. Going beyond just converting paper to digital, organizations need to rethink all steps to maximize and optimize process improvement.

All organization types and sizes ranked “Improving Business Process” roughly the same.

9. Enhance Security and Authentication

For financial institutions, the key component of improving the digital customer experience is to improve the simplicity of banking. One of the challenges around simplification has been the password authentication process needed to access mobile banking. Combining the need to improve the security of accessing accounts, with a desire for greater ease of use, is a difficult balancing act.

According to Deloitte, “Organizations can begin their journey by starting to invest in non-password-based authentication solutions now as part of their digital transformation efforts, such as the rapid adoption of software-as-a-service platforms and omnichannel customer engagement initiatives. These new solution areas can serve as the foundation for broader enterprise authentication initiatives, which may take time.”

It is safe to say that the banking industry is only one data breach away from making this a much higher priority.

Large regional banks, community banks and credit unions ranked security and authentication as a top 3 priority roughly 18% of the time, while large national banks indicated this as a top 3 priority 10% less often (8%).

10. Partner With Fintech Providers

While a lot has been written, and will continue to be written, about the opportunity of fintech partnerships, indicating how the benefits of banking can help start-ups and visa-versa. the reality was best brought forward one year ago when Ron Shevlin stated that it is not partnerships that are needed, but platforms, where banking organizations provide a range of traditional and non-traditional services to their customers. In his article on the subject, he compared the opportunity for banking with what Amazon currently does. As he notes … he knows Amazon, and the banking industry is no Amazon.

The key will still be how to innovate and move the digital banking needle to respond to the needs of the consumer. This may be done through investment, partnership or simply becoming the center of a consumer’s financial relationship, brokering solutions for the benefit of the consumer.

National and regional banks were significantly more likely to indicate partnering with fintech firms as a strategic priority (10% and 18% respectively) with both community banks and credit unions only listing this as a top 3 priority 5% of the time.