Banks and credit unions increasingly grasp the importance of open banking, but the term is not at all understood by consumers, especially in the U.S. Yet people want easier ways to manage their money and that often involves the use of third-party apps that access consumer financial data. The potential of open banking won’t be reached without efforts to educate consumers on its benefits.

“Open banking” is a simple term, but its meanings range all over the place depending on the context and the continent. It can quickly get esoteric, even for banking professionals. And for consumers, even though the phrase seems like it ought to conjure up positive thoughts, it actually scares the heck out of them.

One reaction: “What do you mean ‘open?’ Open to whom? You’re talking about my personal banking information….”

A survey by the consulting firm Simon-Kucher & Partners put some sobering numbers on this phenomenon. The survey covered three major global markets, but the firm broke out the North American results separately.

Simon-Kucher defines open banking simply enough as sharing bank resources such as data, capabilities or processes with third parties including fintech firms, technology providers and other institutions through an Application Programming Interface (API). Even so, the term open banking makes U.S. and Canadian bank consumers nervous.

When told they were using a product or service where their banking provider allows a third party to access its database in order to provide the feature, nearly two out of five (39%) consumers said they would re-think their feature selections.

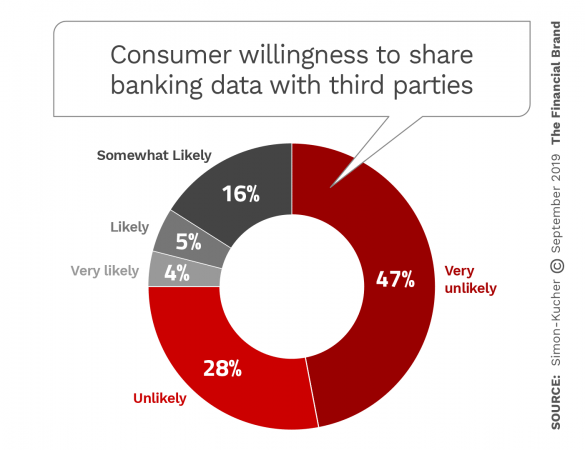

The consulting firm probed further and found that three quarters of consumer respondents in the U.S. and Canada say they are unlikely or very unlikely to allow their banks to share their account information, transaction history, funds overview and other data with third parties.

Consumers in Europe and Singapore — the other markets studied — are somewhat more open about sharing their data, but still, a majority of consumers (53% in Europe, 57% in Singapore) say they are unlikely to allow their bank to share their data.

That’s pretty startling given that financial institutions in Europe are required by regulation to provide access to customer data to third parties when they request it, with customer approval. Europe also has very stringent data protection rules under the General Data Protection Regulation.

How to Ease Consumers’ Qualms

While there are no federal open banking regulations in place in the U.S., many financial institutions already share customer data with third parties, such as core processors and digital banking providers — and, increasingly, fintechs — to enable the fulfillment of a service, basic or advanced.

One possible reason for the negative consumer reaction to open banking could relate to the frequency of data breaches and well-publicized examples of social media data-sharing abuse.

Whatever the cause, reassuring consumers about data security is a must as more competitors and more nontraditional arrangements become the norm. “By thoroughly vetting potential API partners, banks and credit unions can ensure their consumers aren’t subject to unwanted advertising or predatory lending,” states Zafin founder Al Karim Somji.

How best to communicate with consumers about third-party relationships and open banking isn’t immediately clear. David Chung, partner at Simon-Kucher, tells The Financial Brand that a couple of options are viable. A bank or credit union can simply explain that the bank is partnering with third parties in an open banking approach. Or it could leverage the institution’s brand and use “white-label” third-party solutions, not directly advertising the open banking arrangement. Many examples of white-label partnerships currently exist. SigFig, the wealth management and investment platform, is used by several banking providers on a white-label basis. Online lender OnDeck’s relationship with JPMorgan Chase (now being phased out) is another example.

Chung believes that consumers will become more receptive to third-party data sharing as they recognize its benefits. As for their views on the more nebulous “open banking” term, “We expect that regulations will help boost awareness and openness of consumers towards open banking,” Chung states. “Our study showed that European end-clients generally are more aware of open banking than North American end-clients.”

Read More: Will ‘Open Banking’ Sizzle or Fizzle in the U.S.?

Use of APIs and Data Sharing Are Not Options

Why would any U.S. financial institution want to implement open banking voluntarily, rather than by government requirement?

Ironically, part of the reason is because it’s a means to meet changing consumer expectations, despite the fact that consumers don’t connect the dots between secure data sharing and improved service.

People increasingly expect that the third-party apps they use for budgeting or saving can easily access their financial account data, notes Susan McLaughlin, Senior Manager of Virtusa’s BFS Division. On top of that, the big tech companies like Google, Amazon, Facebook and Apple are rapidly, if indirectly, breaking into financial services.

For community financial institutions in particular, open banking offers a way to partner with fintechs to fill in the gaps in their financial offerings. The use of APIs, McLaughlin points out, whether it’s labeled open banking or not, allows traditional institutions, with the customer’s consent, to provide access to specific and protected data to multiple entities.

In addition, payment transaction fees are a diminishing stream for legacy institutions, and the data-access fees in an open banking model can help offset that. New revenue streams from third parties include commissions, fees, subscriptions, and advertising.

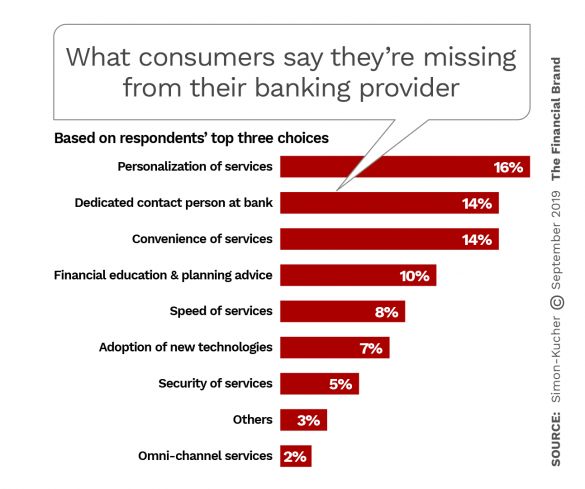

In its research, Simon-Kucher asked consumers what services they feel they are missing from their banking providers’ current product and service offerings. Respondents were asked to select the top three from a list.

The four highest responses were a combination of high-touch and personalization. The latter typically is derived from use of sophisticated data analytics, artificial intelligence and related software. The survey report concludes that open banking development should primarily be centered on these services.

Read More: 5 Pivotal Technology Trends in Retail Banking

Don’t Call it Open Banking and Maybe They’ll Pay for it

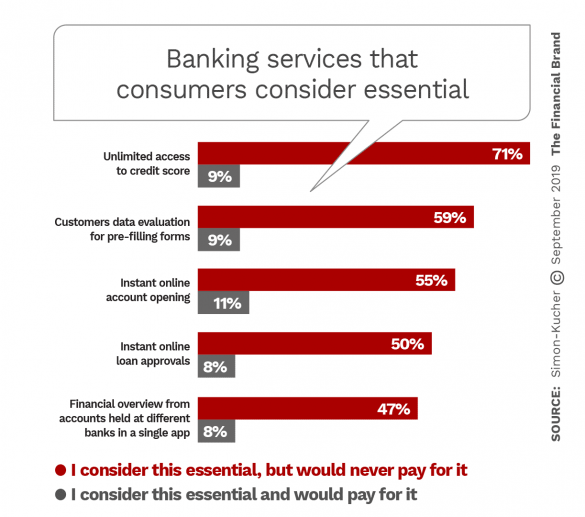

Simon-Kucher listed 14 banking services and asked consumers which they considered essential for their daily banking needs. The firm also inquired about which of these essential services consumers would pay for.

Overall, compared with consumers in Europe and Singapore, U.S. and Canadian consumers are far less willing to pay for essential services.

Unlimited access to credit scores was cited as “essential” by almost three quarters of North American respondents, but less than one in ten would pay for that. Free credit score access has become a common add-on feature for many institutions, including nonbank companies.

Banking customers are somewhat more willing-to-pay for instant online account opening and pre-filled forms. By contrast, in Europe and Singapore, about one quarter of consumers almost across the board are willing to pay for a variety of essential banking services. A change in regulations in the U.S. might shift the prospects for monetizing some new banking capabilities. On the other hand, consumers everywhere are more accustomed than ever to free services. The new Apple Card is a good example.

What Third Parties Want from Banking APIs

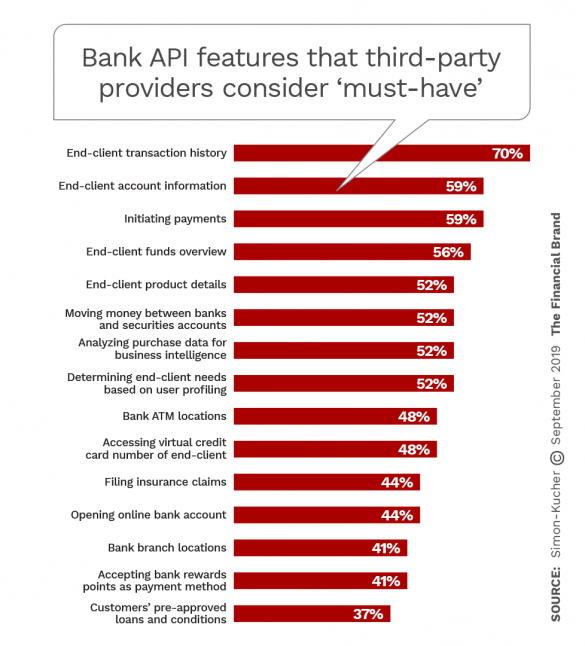

Fintech-banking partnerships are thriving and likely to continue ramping up as financial institutions realize partnering is, for many, the best way to transition to a modern digital institution. Part of the Simon-Kucher survey probed the views of third-party providers about what they most value in terms of bank-provided APIs, and what most challenges them.

Third parties’ use of financial institution APIs primarily for payment purposes and to enhance or enlarge their product or service offering, the consulting firm states. They most highly value APIs that provide consumer transaction history and account information, and APIs that enable payment initiation.

The biggest challenge cited by third-party developers was “setting up required security precautions,” mentioned by 28%. Instability and scalability issues were mentioned by 14% each.

Just over half of third-party partners considered the following API-related features to be not only essential but worth paying for:

- Explanations of API attributes (56%)

- Sandbox capabilities (52%)

- Support for advanced application certification (52%)

Given all the above, David Chung is optimistic about the potential for both bank and consumer benefits from open banking over the next two years.

“We view open banking as an opportunity,” Chung states. “Financial institutions should invest in open banking initiatives to keep up with the competition. Our study shows that there is potential for a narrow segment of end-client services that can be monetized. In addition, the need of third parties for APIs and associated services such as development/sales support can also be monetized.”