Artificial intelligence took a monumental leap forward with the launch of ChatGPT on Nov. 30, 2022. In an instant, machine intelligence became useful to the masses, capturing the imagination of the world and sparking the beginning of the next major platform shift.

This type of general-purpose technology — called generative AI — redefines how we create, consume and manage information. Just like electricity transformed every facet of society, generative AI is poised to become part of our daily lives, enhancing productivity in countless ways.

In the past 10 months, my team and I have engaged with hundreds of financial services leaders ready to embark on their generative AI journey. Many are at the outset, thinking through their strategy and figuring out how to navigate their initial use cases and the associated risks. This article serves as a compass, capturing frequently asked questions and sentiments from bank and credit union leaders actively deploying generative AI use cases.

“At the core of banking’s strength lie two unparalleled attributes — our extensive customer relationships and a treasure trove of data. It’s these very facets that set the stage for an unmatched potential in leveraging AI and machine learning. Be it revolutionizing customer support, offering bespoke financial guidance, or enhancing marketing and sales, the horizon looks promising.”

Allan Rayson

Allan Rayson

Chief Innovation Officer and Chief Technology Officer

Encore Bank

The Benefits of Gen AI for Banks and Credit Unions

Question #1: What kind of generative AI technology is available to financial services executives today, and how will it benefit our organization?

What’s available is a type of AI that creates new content based on what it has learned from existing content. Generative AI is applicable to all modes of content, including text, image, audio, code and video.

Text generation, in particular, has sparked the enthusiasm of bank and credit union leaders, distinguishing itself from the buzz that surrounded “chatbots” and “natural language processing” in the past.

The driving force behind this resurgence is the great potential of large language models, or LLMs. These probabilistic systems understand connections in vast quantities of text, an improvement over traditional AI, which doesn’t go beyond regurgitating information that it has been given. When you engage with tools like OpenAI’s ChatGPT or Google’s Bard, they can predict your next words by drawing from the vast corpus of text they’ve been trained on across the internet.

For the first time in history, LLMs enable us to exchange information with machines in our native language. The financial services sector, deeply rooted in data-driven, informational products, is uniquely positioned to benefit from LLMs. The potential exists to dramatically improve the efficiency ratio, a standard industry metric.

One example: With LLMs, customer questions such as, “How does a market downturn affect my portfolio’s projected performance?” can be addressed with a fraction of the effort previously required.

Addressing such a query with LLMs leads to:

1. Reduced operational costs: Swift, accurate responses mean less time and money spent on manual data review.

2. Better customer experience: Rapid query resolution enhances customer satisfaction, potentially leading to greater wallet share.

3. Decreased training costs: Employees can rely on LLMs for initial responses, reducing the need for intensive training sessions.

4. Operational speed: When employees spend less time searching for answers, there are efficiency gains.

5. Increased revenue opportunities: The time saved can be reallocated to revenue-generating activities.

There are countless examples similar to this, and incorporating LLMs for such tasks paves the way for a new era of operational efficiency in the financial sector.

“As an industry, we are still trying to take advantage of all the efficiencies and opportunities the internet and mobile evolutions have provided. I’m confident we can’t afford to take this long, thoughtful approach with AI. This shift in generative AI is poised to move much quicker and requires us to start understanding and considering today’s and tomorrow’s possibilities. Generative AI offers gains in productivity and communication, and quicker analysis of data models, helping us become better at personalization and differentiation from an internal and external perspective. This is the technology we’ve been waiting for!”

Steve O’Donnell

Steve O’Donnell

Chief Financial Officer

One Nevada Credit Union

Envisioning How Generative AI Will Change Banking

Question #2: What can we expect in the next decade?

Ubiquitous intelligence will be accessible to anyone with a smart device. Each of us will have access to a digital assistant — our “Chief of Staff” — to plan our vacations, answer emails, negotiate rates, open accounts, manage our schedules, and perform many other tasks that take up our time today.

Moreover, these intelligent general assistants will grant access to specialized autonomous agents, paving the way for groundbreaking innovations. Autonomous agents are AI-driven programs that can independently initiate, manage, and complete tasks, adjusting their approach based on evolving objectives.

Picture a student ready to open their first bank account. The student merely tells the Chief of Staff, and autonomous agents from various financial institutions offer tailored account proposals, each vying to provide the best terms based on the student’s unique financial profile. The entire process, driven by intricate negotiations between the Chief of Staff and these agents, happens without any human intervention.

In much the same way we couldn’t have anticipated the rise of smart homes from the advent of electricity or Uber from the birth of smartphones, generative AI is poised to unveil unforeseen opportunities that go beyond the realms of tools like ChatGPT, and this progress is accelerating at a rapid pace.

Want to go deep on AI best practices for banks?

Attend our AI Masterclass — Unlocking the Power of Artificial Intelligence in Banking — at The Financial Brand Forum 2024 on May 20-22 in Las Vegas. Led by Ron Shevlin, chief research officer at Cornerstone, this three-hour workshop will be jam-packed with lessons learned from industry leaders and real-world case studies.

For more information and to register, check out the Forum website.

The financial sector has consistently aspired to shape a future where consumers and businesses can effortlessly manage accounts, conduct money transfers, or execute refinancings, all through a natural language conversation. Look for generative AI to put this aspiration within reach.

Imagine one of your customers posing the question, “How would my monthly payments vary if I refinanced my mortgage with you versus [insert your competition here]?”

A swift, streamlined reply should be standard. But with financial products becoming more commoditized, balancing profitability goals with exceptional customer experience poses a unique challenge in answering such a question. And yet, both retail and business customers seek this level of interaction.

Given the speed of the technological evolution, financial institutions are embracing these capabilities. The mandate is clear for executives: Incorporate this technology into your processes while judiciously weighing its implications.

“The risk of inaction in the age of AI is exponentially higher than in past technological revolutions. Whereas being late to electricity or the internet might have allowed for catch-up, falling behind in AI could be an insurmountable gap. Learning is cumulative; once you’re behind, catching up in AI model learning is not guaranteed.”

Kirk Drake

Kirk Drake

Founder and CEO

CU 2.0

Read more:

- Why AI Projects Often Flop in Banking and What to Do

- 3 Strateges for Enterprise AI Success That Are Tried and ‘Truist’

Protecting Sensitive Data from Gen AI Leaks

Question #3: How do we harness the power of these models on proprietary institutional knowledge without exposing sensitive data?

In our interactions with financial services executives, a major focus has been on selecting use cases that tap into proprietary institutional knowledge to drive workflow enhancements, while simultaneously managing the risks associated with data exposure.

The first reaction at many banks and credit unions was to block employees from using tools like ChatGPT. Yet, this doesn’t address the broader challenge posed by the use of personal devices.

For example, an employee might copy an email from a customer and paste it into ChatGPT on their personal device to gauge sentiment and generate a quick response. This inadvertently diminishes transparency regarding what data might be relayed to providers like OpenAI for model training.

Consequently, financial institutions are taking steps to minimize the risk of data exposure, while still engaging in rapid experimentation across use cases. At the heart of these efforts is a governance framework tailored specifically for generative AI.

Key elements of this framework include:

- Opting for model providers that have strict data retention policies, ensuring data isn’t repurposed for model training.

- Implementing supplementary tools that redact and de-identify personal information without compromising response quality.

- Training and fine-tuning open-source models securely within an organization’s own environment.

Once a financial institution gets comfortable with leveraging an LLM on their internal data and institutional knowledge, a shift in focus to use case selection and mapping out workflows becomes the priority.

“As we deepen our exploration of generative AI, crafting a strategic blueprint for governance becomes essential. Ethical AI is not just a consideration but a mandate, requiring vigilant oversight. A ‘center of excellence’ must be established to develop frameworks that address ethics, bias and risk. Leveraging LLMs on institutional knowledge is a key component of this strategy. AI isn’t a fleeting trend; it’s a cultural transformation requiring collective commitment.”

Mark Rowan

Mark Rowan

Chief Technology Officer

Credit Union of Colorado

Where to Start with Applying Generative AI

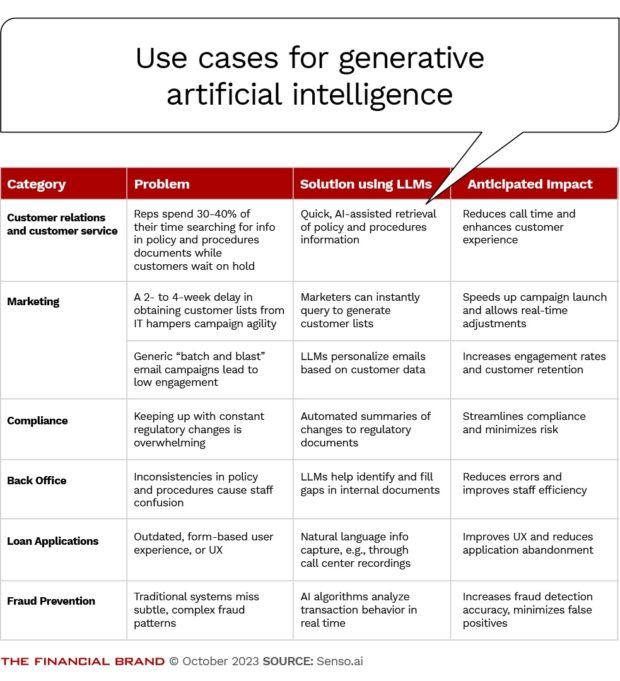

Question #4: Which use cases should I focus on first?

When getting started, banks and credit unions typically adopt a “crawl, walk, run” strategy to the selection of use cases, beginning with those that are low risk and high impact. The initial focus is on workflows utilizing non-sensitive data where the consequences of inaccurate responses are minor. Executed effectively, this lays the foundation for rapid experimentation, which leads to early successes. The freshly invigorated staff then goes on to explore more advanced applications.

Each use case requires a different approach and comes with trade-offs in terms of cost, effort, and impact. The table below provides examples of common use cases across financial institutions.

After implementing your first use case, you’ll begin to understand that the pace of change in this space is happening in days and weeks. What seems out of reach today could be achievable in a matter of months.

As an example, consider two trends: First, as advanced models become more affordable, they offer superior analytical capabilities to augment and streamline business processes. Second, open-source models, becoming smaller and more powerful, can effectively run on a device, integrating seamlessly into in-house operations.

As these types of generative AI models become increasingly affordable and the financial services industry gets more sophisticated in its ability to harness them, additional opportunities arise. For example, autonomous agents can be seamlessly integrated into internal workflows to communicate directly with all those Chief of Staff digital assistants working on behalf of existing and prospective customers, much like the scenario we painted with the high school student opening a bank account.

Empowering your staff to continually explore and test new use cases with emerging tools will create a culture that attracts the best talent. This is the kind of workplace that innovative people want to be a part of.

With the help of these empowered and innovative employees, your financial institution will be able to adapt to new developments quickly and gain a competitive edge.

“Our mission in supporting the growth and development of technologies for community banks is founded on solutions that help community banks be more profitable, more efficient and more competitive. New technologies like generative AI check off all of the boxes. How we get there is the question. The ‘crawl, walk, run’ approach not only mitigates risks but also capitalizes on immediate, high-impact use cases. Ignoring this is not an option; we must lead with calculated courage to fully realize the transformative potential of this technology. Your financial institution’s ability to adapt will determine whether you’re setting the pace or playing catch-up.”

Wayne Miller

Wayne Miller

Senior Vice President for Innovation

Independent Community Bankers of America

Read more:

- The Best Way to Implement AI and Avoid Random Acts of Digital

- See all of our latest coverage of artificial intelligence in banking

Talent Strategy for Capitalizing on Gen AI

Question #5: How do I prepare my workforce for this shift?

Unlike past platform shifts, generative AI stands out because its capabilities match, and will eventually exceed, what makes humans unique: intelligence.

If knowledge creates value, and understanding the links between knowledge enhances efficiency, then the notion of condensing all of our collective knowledge into a system that understands these relationships is the pinnacle of humanity’s technological journey.

This radical idea elicits a mix of excitement and hesitation. A huge transition is on the horizon, signaling an inevitable need for a majority of knowledge workers across sectors to adapt and retrain. Undoubtedly, one question many employees have is, “How will this influence my role?”

As with all change, employee reactions will vary: Some will embrace generative AI, while others resist. Effective change management becomes essential for both groups, and it’s paramount for leadership teams to strategize for this transition proactively rather than reactively.

Based on my experiences observing leaders in the financial services space, I believe the approach with the best chance of success is twofold:

• For the enthusiasts: Provide them with resources, education, and tools that empower them to delve into experimentation and explore new use cases. This not only fosters innovation but also retains top talent.

• For the apprehensive: The antidote to fear is deep understanding. Invest in their growth, familiarize them with the new tools, demystify underlying concepts, and pair them with colleagues who have naturally adopted these changes.

Appointing a dedicated leader for this transition is essential. Such a figure should exhibit both empathy and adaptability. Staying abreast of rapid technological advances while inclusively guiding all willing employees on this transformative journey will be indispensable for maintaining a competitive edge.

“Adopting generative AI isn’t just a tech upgrade; it’s a cultural shift that changes how we interact with computers. We’re moving from static inputs and outputs to interacting with AI ‘personalities.’ An internal champion is essential to help your organization through this transition because the real question isn’t if we’ll use AI, but how we’ll integrate it effectively, as it becomes a fixture in our daily lives.”

Joey Rudisill

Joey Rudisill

Chief Information Officer

Central Willamette Credit Union

It’s Already a Generative AI World, Ready or Not

The financial services industry is on the brink of a powerful transformative wave.

Early adopters are poised to reap significant advantages, from sharpening their efficiency ratios to delivering unmatched customer experiences. The road to triumph will be paved by those who adeptly pick use cases that amplify and energize their organizational spirit, all while thoroughly grasping and mitigating associated risks.

The enhanced productivity and service standards we’ve long pursued are now within grasp, and first movers with the right mindset will emerge as leaders in the age of AI.

“The long-term winners in many industries will be those who heard the starting gun fire the moment their leadership used an AI tool and made the bold decision that waiting for consensus is the surest way to ensure mediocrity. We must move forward as leaders to embrace these tools and be thoughtful about our governance and expectations. The power (or weakness) of generative AI is not simply the output that you see today, it is unlocking your curiosity about the promise of tomorrow.”

Jesse Honigberg

Jesse Honigberg

Executive Vice President, Product and Platforms

Customers Bank

About the author:

Saroop Bharwani is the co-founder and chief executive of Senso.ai, which provides generative AI solutions to the financial services sector, and the founder of FirstPrinciplesAI.com, an initiative dedicated to providing financial services executives with the knowledge and skills needed to compete in the age of AI.