One thing any marketer hates to do is miss a big opportunity to move the needle in a meaningful way instead of the usual incremental gains. Only one thing’s worse: Missing the opportunity and getting clobbered at the same time.

The current retail banking marketplace could be experiencing such a moment. Consumer intent — and actions — to change primary financial institution or to move more of their deposits and financial business to other providers, traditional or otherwise, appears to be rising sharply.

A confluence of evidence suggesting a significant opportunity/threat is unfolding. While not every data source supports this expectation equally — that hardly ever happens — the stakes loom too large to await total confirmation.

Before the pandemic, “switching intent” — meaning people who say they are definitely changing primary banks in the next six months — had been steady at about 9% of households and 14% of businesses for several years, according to Bruce Paul, Managing Director, Banking Research for Rivel. When the pandemic hit, switching intent fell sharply because of shuttered branches and uncertainty, but has since “come roaring back,” Paul tells The Financial Brand.

In Rivel’s latest wave of consumer interviews (104,000 people from November 2020 through January 2021) switching intent shot up to 17% among households and 31% among businesses, almost double the normal levels.

“I have never seen such a dramatic increase in switching behavior in the three decades I have been tracking this,” Paul states. “Even the figures during the financial crisis pale in comparison.”

Big Moment:

For banks and credit unions, there may never be as big an opportunity to quickly capture market share — or lose it.

As always, there is a difference between “intent” and actually doing something. Paul acknowledges this, but points to two additional statistics from their latest research:

- 31% of consumers are unhappy with their current banking provider.

- 15% are saying they’re actually going to switch in the next six months.

Both numbers are historically high, Paul observes. Pre-pandemic the “unhappy” figure would hover around the mid 20%s, while “actually planning to switch” was usually under 10%.

Read More: Does Being a ‘Primary Financial Institution’ Mean What It Used To?

Other Evidence that Consumers Are on the Move

Consumer intelligence company Resonate, which uses interviews plus artificial intelligence modeling to measure consumer banking behavior, finds a similar percentage of consumers with intent to switch banking providers: 16.4% of all U.S. adults (18 or older) as of April 2021. That equates to 36.7 million people, according to Ericka McCoy, Resonate’s CMO.

The company reports that 9.3 million people (roughly 4% of all U.S. adults) say they are actively switching, a much lower figure than what Rivel reports. The companies use different research methodologies, however, so a direct comparison is not possible. Resonate does say that about a third of active switchers (3.3 million people) are planning to change financial institutions by July 2021.

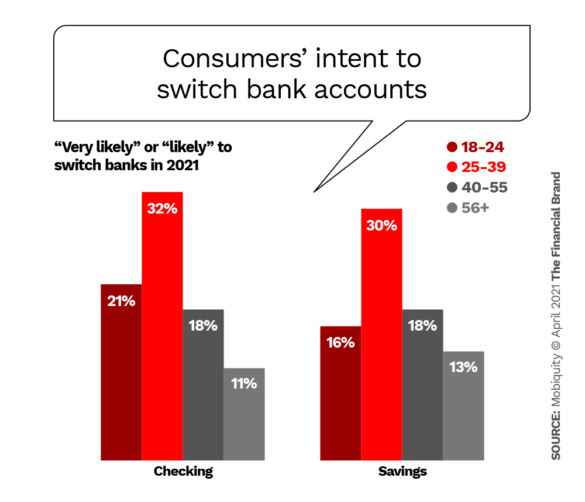

Digital consultancy Mobiquity surveyed about 2,445 U.S. adult consumers in January 2021 and found that 11% of the respondents said they had already made an account switch for either a checking or savings account in the past year. The company also asked respondents to predict their switching behavior in 2021.

In both instances — those who had switched accounts and those who were expected to do so —Millennials were the dominant group.

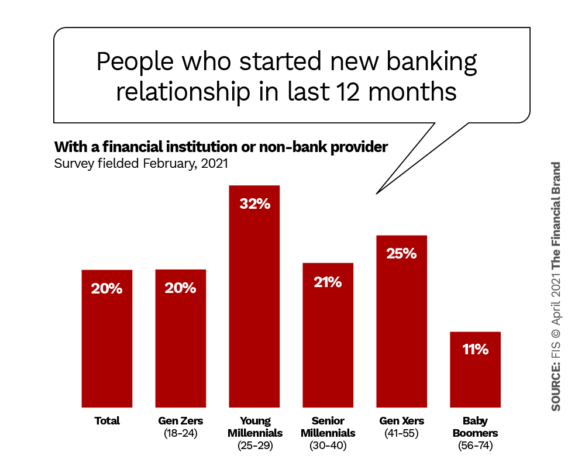

In its latest PACE research, FIS found that one fifth of 1,015 U.S. consumers surveyed in early February 2021 said they had started a new banking relationship in the previous 12 month period.

All this evidence doesn’t necessarily mean that consumers are moving their primary banking relationship. MetaBank, the big prepaid card issuer (and one of the banks backing SoFi Money), found in a survey conducted with Visa that more than a quarter (27%) of the banking population are what it calls “hybrid consumers,” i.e. people who have both digital-only and traditional accounts.

Consumers in this segment are six times more likely than average to have three or more bank accounts. However, they are also highly unlikely to give up their traditional accounts: 77% said they would never do so, according to MetaBank.

Banks and credit unions don’t always acknowledge the fact that even though they may still have “John H.” as a customer, the relationship has shrunk from six accounts and total deposits of $50,000 to two accounts with less than $1,000, observes Rivel’s Bruce Paul.

Read More: The Secret Financial Lives of Consumers Banks Don’t Know About

Where People Are Switching to (and Why)

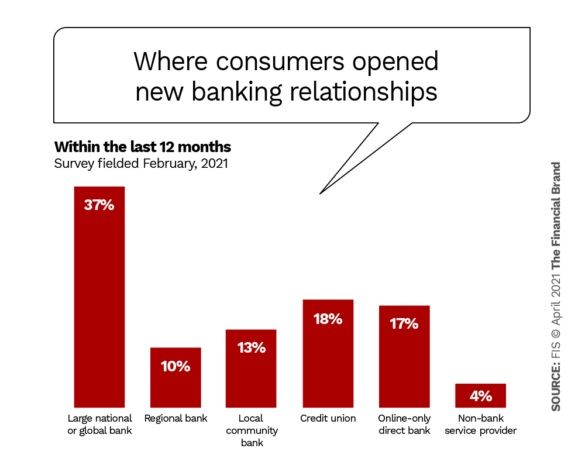

Because it measured actual behavior rather than intent, the FIS study asked consumers where they had opened new accounts in 2020 and what prompted them to do so.

The power of the largest U.S. banks as new account magnets is clearly seen in the chart above. In fact, among younger adults (18-29), the percentage of new accounts moving to big banks was even higher — 43%. The losers in this switching battle were mainly regional banks and community banks. Credit unions and online-only banks did somewhat better, but still trailed the big banks by a large measure.

Online-only (or direct) banks came in about even with credit unions, but were a strong second (at 23%) among the 18-29 set. Bruce Paul says awareness of this segment is “still pretty low,” however, because they’re more narrowly targeted and don’t do much national advertising (Ally Bank being an exception). Also, he says, customer satisfaction dropped for many of them during the pandemic.

Between the Lines:

So even neobanks like Chime and GoBank as well as direct banks like Ally and Discover may not be immune from consumers looking for something better.

People were willing to be patient with their institution in the early stages of the pandemic when responsiveness “fell off the cliff” because branches weren’t open and call centers were overwhelmed, Paul notes

“What we’re seeing is that for some financial institutions, it never got better,” the researcher continues. “People are not giving these institutions the benefit of the doubt anymore.”

“There are some financial institutions where our research indicates that more than 30% of their customers are on the way out the door.”

— Bruce Paul, Rivel

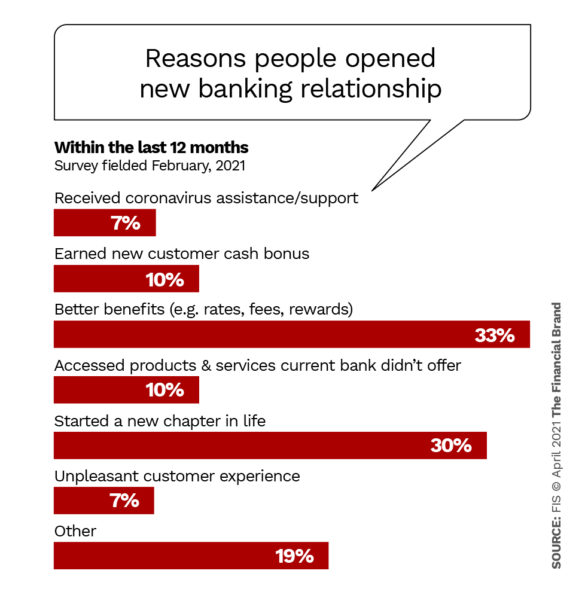

Somewhat as a counterpoint, FIS found that the two biggest reasons for opening a new account at another institution were not based on frustration, but mainly on two long-standing reasons for switching: life changes and better rates and fees.

For Gen Zers and younger Millennials, as well as for Baby Boomers, better rates and fees were the number one reason. For older Millennials (30-40), “a new chapter in life” was by far the largest reason for starting new banking relationships.

Read More:

- Five Ways Marketers Can Get People to Switch Banking Providers

- Overcoming Inertia: Getting Consumers to Switch Banks

Account Tenure: Loyalty vs. Inertia

So far, the average length of time consumers maintain their primary banking account has not declined significantly.

Rivel, which tracks how long consumers stay with their primary institution, puts the average figure at 17 years, down slightly from around 16 a decade ago.

Bankrate.com has studied the question for several years. In its latest survey (2021), the consumer-focused site found that the average checking account holder had been with the same bank or credit union for about 14 years. That was almost the same the year before — 14.3 years — but down from 16 years in 2017.

Of note going forward, Bankrate said in 2020 that Millennials kept their checking account for “just over nine years” on average.

Even the older demographics may be more open to change now, however. “Older generations were a little bit more hesitant to switch banking providers before because they weren’t as technically savvy,” observes Resonate’s Ericka McCoy. “Now they’re more comfortable with digital because they’ve had to be. People are not necessarily rushing to go back into bank branches and they realize that switching banks is not such a big deal.”

“Loyalty is down, comfort with digital banking is up. That’s the biggest takeaway from the last 15 months.”

— Ericka McCoy, Resonate

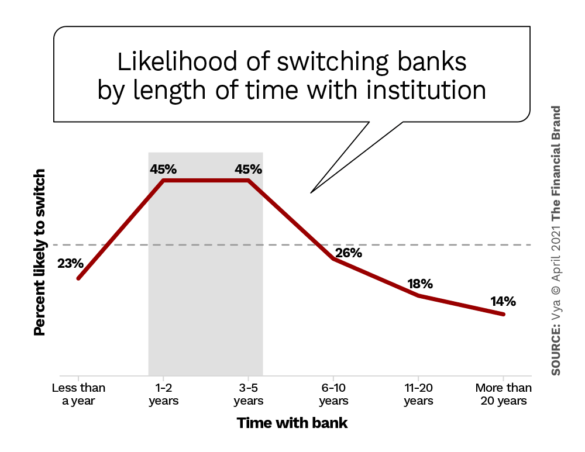

An interesting angle on the matter of account longevity shows up in data from a targeted survey by marketing company Vya.

Consumers who have been with a financial institution between one and five years are significantly more likely to leave the institution. Many of these consumers, Vya observes, will likely be younger adults. These folks tend to know more about the latest products and services, and keep closer tabs on new or competing offerings.

Read More: Survey Reveals a Hidden Customer Exodus in Banking

Marketing Tips to Attract Consumers on the Move

All of the above presents financial marketers with both a challenge and a potentially huge opportunity.

“You could make a good argument that in 2021 and 2022, marketing may be most important factor in determining the success of banks and credit unions, even more than technology, branch footprint, or customer service,” Rivel’s Bruce Paul asserts.

One approach to sizing up the switching market

Just how big is the market for switchers for your institution? The analysis below, prepared by Jeffry Pilcher, Founder and CEO of The Financial Brand offers marketers a good place to start.

If one in 14 people change banks every year (based on the data from Bankrate.com), that means 7.1% of the market is up for grabs annually. Banks and credit unions can set their baseline acquisition benchmarks off this number.

For example: One market has 100,000 people with three institutions. That means 7,143 people in this market will be changing financial institutions. Bank X has 50% of the market, Bank Y has 35% of the market, and Bank Z has 15% of the market. That means Bank X should expect to see 3,571 new accounts (50% of the 1 in 14 switchers), Bank Y should see 2,500 new accounts, and Bank Z 1,071 new accounts. That’s the baseline. If Bank Z wants to expand their market share, they will need to add more than 1,071 new accounts in the next year.

Complicating this analysis is how many people are opening their first bank account. The size of the pie everyone is fighting over really includes both net new accounts and switchers.

Forget about being the friendly bank

The typical community bank and credit union marketing message, says Bruce Paul, is “We’re not a big mean national bank, we’re a nice friendly local bank.” But that’s not why people leave the big banks, he adds.

“Customers of big banks don’t say, ‘Oh, the people at Bank of America are really unfriendly’,” Paul explains. “They may not be knowledgeable or good at responding, but they’re friendly. It’s not like in Peoria, Ill., all the unfriendly people go to work at Bank of America and all the friendly people work at First National Bank.”

Keep This in Mind:

Like politics, all banking is local, so marketers need to build their messaging around the local market conditions and opinions.

Successful financial marketers are much more specific in their messaging, Paul maintains. They’ll say, “This is what you will get when you move here” as opposed to “We’re nice, consider us.”

To illustrate the need for targeted messaging, Rivel’s data shows that in Houston a relatively high percentage of households think the staff are not well trained at their bank — no matter what the institution size. So a marketing approach emphasizing superior expertise will work well there, Paul suggests.