How consumers research and purchase banking products is complex. More than half start their journey either online or using a mobile device, and most of them end up finishing the process in a branch.

Many banks and credit unions would call that a failure because the online and mobile channels didn’t deliver an entirely digital consumer journey. That’s not entirely true. Banks and credit unions aren’t measuring digital’s impact correctly, according to the ForeSee. They contend that an “all-digital retail delivery experience” is aspirational, but not realistic.

Financial institutions might desperately want people to use digital channels exclusively (even if they aren’t fully capable of delivering such an experience). But consumers are in charge of their own journeys, which is why ForeSee concludes that digital is working even when the journey doesn’t start and end digitally.

For instance, think about how you shop for clothes, or electric toothbrushes, or a new refrigerator. It’s increasingly rare that consumers shop for a product or service using a single channel. Take a refrigerator. If your refrigerator is ready to take its last breath, you go online and start researching different makes and models. You narrow down your search to a few. But a refrigerator is a big-ticket item and you want to touch and feel it before you buy. So, you hop in the car and drive to the nearest big-box store that carries that brand. You open and close the door, check the freezer space, chat with the salesperson. You kick the tires, as the expression goes.

You then sneak off to the lumber section, out of view of salespeople, so you can use your mobile phone to look up pricing for that model at other stores — both brick-and-mortar stores and online retailers. You return home to think about the refrigerator. The next morning while drinking coffee, you use your tablet to order the refrigerator online from the same big box store you visited the day before. You might have been able to get the same refrigerator for a few bucks cheaper, but it was reasonably priced, you trust the big box brand, and they have next-day delivery.

Your path to a new refrigerator was a complex journey involving multiple channels: online research using a desktop computer, a visit to a physical store, mobile price comparisons, and an online purchase. And in all likelihood, you are perfectly okay with that. You don’t think the process is “broken” or that any particular channel “failed” you. Each channel did exactly what it could/should do, and you leveraged each the right way at the right time.

Read More:

- Gen Z Prefers Banks to Big Techs, But Shuns Branches

- Seven Drivers of Successful Digital Banking Evolution

Consumers like charting their own journey depending on their comfort with different channels, and the type of product or service they are buying. The journey for paperclips would look a lot different than, say, a new sailboat. Similarly with services, the journey to plan a family vacation would look markedly different than finding a new accountant or hair stylist. The combination and weight of online reviews vs. word-of-mouth referrals will vary greatly.

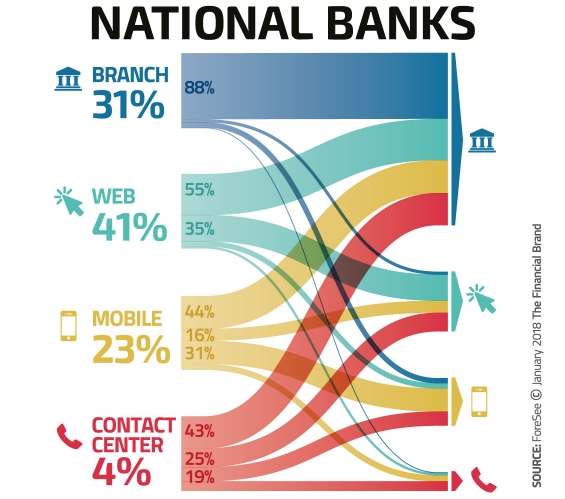

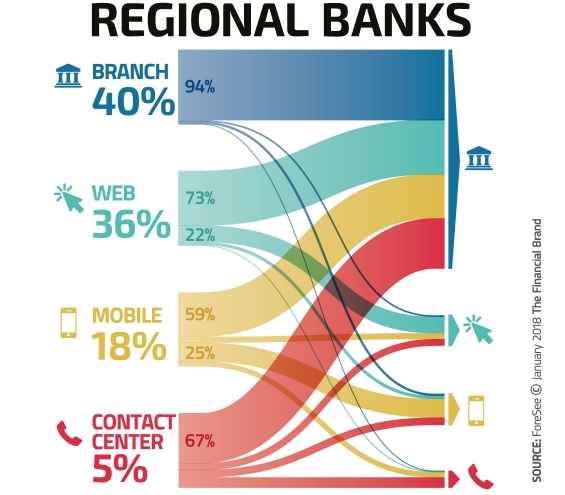

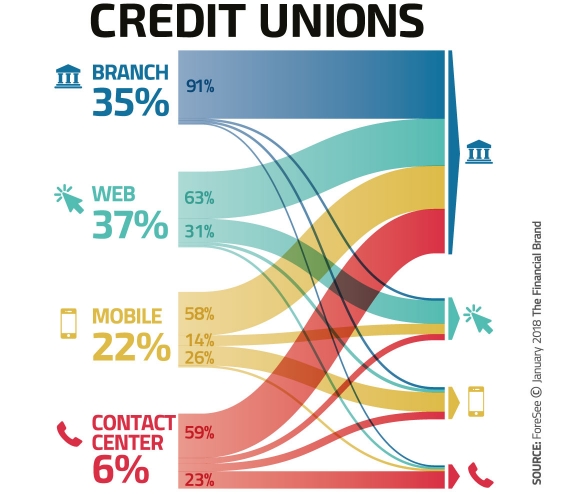

Bank and credit union consumers are no different. Their journey is complex and almost always includes multiple touchpoints. Consumers that start their journey digitally don’t necessarily complete their transaction digitally. In fact, according to the ForeSee Experience Index, Overall, nearly two-thirds (61%) of consumers start their journey in a digital channel when opening a new account, while more than half (58%) of those end up in a branch.

Where Financial Consumers Start and End Their Journey

As part of their analysis, ForeSee broke down the customer journey, comparing the starting point and end point between national banks, regional banks and credit unions. Their resulting illustrations are among some the best infographics The Financial Brand has ever seen — telling a rich, complex story in a simple, visual format.

Read More: The Rise of the Hybrid Consumer in Banking (And Why It Matters)

Consumers May Actually Like It This Way

So why does the consumer journey include multiple touchpoints? Is it because the online or mobile account opening process is so poor that people get frustrated, hop in the car and drive to a branch? Or is it because they just feel more comfortable opening an account face-to-face?

Not long ago, there was much chatter in the banking world about the “omnichannel experience” — that consumers could choose whatever channel they were most comfortable with. But the general assumption was that digital natives (e.g., Millennials) would be thrilled if they could do everything in digital channels. This, of course, is what banking executives were hoping for — that consumers would eventually migrate to digital self-service channels so those costly branch networks could be pared back. Turns out that ultimately it doesn’t really matter what you want them to do. What matters is that they are using multiple touchpoints by choice.

The mistake that banks and credits unions make is thinking that “omni-channel” is predicated on offering a consistent experience in every channel. But consumers will — and indeed many prefer — to bounce around from channel to channel, depending on where they are in the journey. Or time of day. Or even mood. They’ll select the channel that, at that particular time, seems the easiest or most convenient.

In fact, notes Jason Conrad, Vice President of ForeSee’s retail banking business, consumers who stay in one channel are actually less satisfied than those who use multiple channels. Conrad could be more blunt: “Consumers like having multiple channels.”

And according to ForeSee’s data, the particular channels they start or end with doesn’t impact satisfaction.

Measuring Digital’s Impact the Right Way

Banks and credit unions tend to approach the consumer journey as a logical progression from point A to point B, and therefore assume that consumers want to remain in the channel they started in. If a consumer starts opening an account online, financial institutions consider the consumer experience a failure if the consumer then finishes opening the account in a branch. Banks and credit unions work feverishly to figure how they can improve the digital account opening process so that consumers stay online.

Sure, you can (and should!) improve account opening; many consumers would be thrilled to finish opening and account digitally. But others would prefer to start the process online and then visit a branch to seal the deal.

Read More: Branches Still Dominate, But Banks Won’t Need as Many to Compete

So you shouldn’t measure success based on how many consumers start and end their journey digitally. Those consumers who research an auto or home loan online but who abandon their session before completing an application doesn’t necessarily mean that something is wrong with the digital experience. Digital could very well be doing what digital should be doing: allowing consumers to research products and services before buying… either online or in a branch.

“Measuring online conversions just isn’t as important as banks and credit unions like to think it is,” says Conrad. “Instead, they should measure and quantify digital’s contribution to conversions in other channels.”

When a consumer walks into a branch, you need to ask them about their journey, says Conrad. Did they conduct some research online? Did they look at reviews on their mobile device? Did they talk with friends or family? And what prompted them to come into the branch? Would they have preferred to complete the transaction fully digitally, or were they happy to research first and then come to the branch?

These questions will allow you to better gauge the success of your digital channels. And the answers enable you to determine which products and services consumers want to complete fully digitally vs. those that require face-to-face interaction. You can then focus on improving the digital experience for those products and services, and tailor your brick-and-mortar experience accordingly. If consumers want to complete a mortgage face-to-face with a lender, don’t spend time and money trying to fully automate the process when you could focus on a different product, such as online checking accounts. Using the right benchmarks lets you properly allocate resources to each channel.

Conrad believes that as long as banking providers manage and measure the experience wherever consumers interact with them in a standard and scientific way, the journey will take care of itself no matter how complex it may be.

“The consumer journey can be infinitely complex with an unlimited number of variations,” he says. “Just remember, branches still matter… a lot.”