Brian Solis

You know what the biggest disruption to the banking industry is? If you answered, “block chain”, you are only partially correct. The other looming threat is human.

Like block chain, Millennials and Centennials represent one of the greatest disruptive threats to the banking industry. I hear from executives all the time, “Yeah Brian, we know that younger generations think differently…we get it.” I believe they believe and that they do get it.

These executives are concentrating on managing a variety of products, assets and customer segments. Yet every day, financial executives make decisions that place brands on a path of legacy-based iteration models over the investment in innovative models that deliver new value to customers who represent the future of banking.

Iteration and innovation require intentional balance. The recipe between iteration and innovation determines the fate of any organization and whether it is the disruptor or the disrupted.

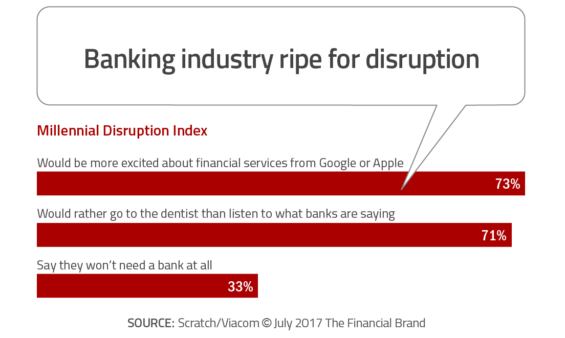

In an ominous research project, “The Millennial Disruption Index,” a three-year study conducted by Viacom, banking ranked highest for risk of disruption ahead of household goods and discount retail. Over 10,000 Millennials were surveyed about 73 companies across 15 industries. Of those who participated, 53% don’t think their banks offer anything different than other banks. Worse yet,, 71% would rather go to the dentist than listen to what banks are saying.

Here’s where things become very real and serious. One in three surveyed are open to switching banks in the next 90 days. This will happen with no love lost. And all banks are at risk if they don’t listen to what this generation is asking for.

The change will be seismic. 68% and 70% believe that in five years, the way we access our money and pay for things respectively will be completely different. Furthermore, 33% believe that they won’t need a bank at all.

What will they need? Millennials believe that innovation will come from outside the industry. Nearly half of participants are counting on tech start-ups to overhaul the way banks work. In addition, 73% would be more excited about a new financial offerings and services from Google, Amazon, Apple, Paypal or Square than from their own bank.

Out of Touchness Prevents True Innovation

I want to believe that decision-makers want to do the right thing. I just think that oftentimes, the center of reference in planning for the future, and the steps to get there, are out of touch with the centers of reference in how consumers and societies at large are actually evolving.

This is why work toward innovation is critical in that it forces alignment between your work and new generations of banked and unbanked customers. While many companies believe they’re investing in innovation, the truth is that they are “innovating” on top of legacy mindsets, processes and risk thresholds.

Oftentimes, this leads to iteration at best. At least it’s progress, but innovation, many a time, it is not. What’s the difference between them? Without diverting the conversation at the highest level on such a frequent basis?

- Iteration is doing the same things better, faster, at scale, etc.

- Innovation is doing new things that introduce new value.

- Disruption is doing new things that eventually make old ways obsolete.

To innovate takes iteration. But it needs to be iterating in previously uncharted paths, developing new expertise, experience, models, and policies in the process.

Whereas common corporate iteration pushes forward in already familiar or known paths. They’re both necessary to create new value and improve services (and margins) over time. But there’s a balance to thwart disruption and to become the disruptor.

Banks Must Prioritize Design Thinking, UX and Experience Architecture for ‘Generation-C’

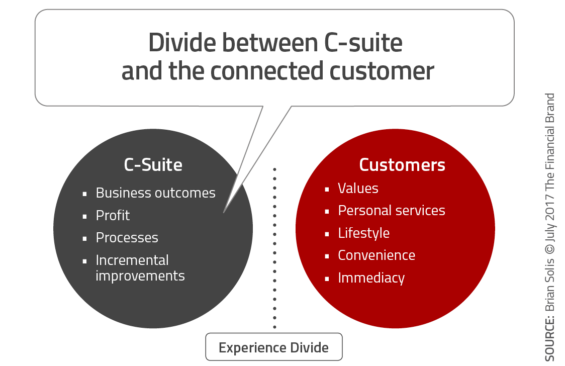

Decision-makers aren’t ‘connected’ customers. This is at the heart of out of touchness.

Innovation takes design for digitally connected generations. And by innovation, I don’t mean developing mobile apps, responsive websites, or remodeling branches into pseudo retail branch fused with co-working spaces.

Younger generations are learning to think differently about value and service. It’s simply how they’re programmed. I refer to digital consumers as ‘Generation-C’ where the “C” represents connected.

As digital natives, they grew up already connected. They have to learn how to think and act analog whereas executives largely grew up analog and have to learn digital trends as they go.

Measuring the overlap in any Venn diagram that compares the two is not as productive as measuring the divide between what banking executives think Generation-C wants or what they will love vs. what they need, want or what they couldn’t live without. This creates an experience divide that, without intentional, investment only widens.

Generation-C is moving in new directions, and as they do, their behaviors, preferences, and values also transform. Every time they use Snapchat, they learn how to communicate differently.

Whenever they swipe in Tinder, Bustle or Bumble, they learn to date differently (while boosting self-confidence). Every time they use Uber or Lyft, they experience on-demand services where transactions are transparent, intuitive and frictionless. Every time, they watch videos on Youtube or they listen to music on Spotify, they’re rewarded with entertainment in real time wherever and whenever they want (many times for free).

This is just a cursory glance of what consumes their attention now, but as they consume differently, traditional industries that don’t mirror these new experiences will find themselves only that much further behind.

But make no mistake, each app, device, and service now and as they change tomorrow, further conditions them away from the center of banking gravity that your C-suite understands (“C” in this case does not mean ‘connected’).

Can You Captivate Generation-C?

Your unbanked or underbanked customers will remain that way until they’re captivated otherwise. And to captivate them takes innovation beyond iteration rooted in legacy values. That starts with a shift in perspective to learn and unlearn, and to see and do what you’re not considering or investing enough in today.

That’s the thing about iteration based on legacy value models and exploring innovative opportunities. It’s the difference between out of touchness and being in touch. How you define value … how you work toward delivering that value … the rules you play by and the guardrails you lean on, are counter intuitive to how society is evolving.

Generation-C is telling you what they think, want and how they’re changing explicitly and also implicitly in the apps and services they value outside of your industry. Are you listening?

Brian Solis is Principal Analyst at Altimeter Group, a Prophet company. Solis studies the effects of disruptive technology on business and society, and humanizes these impacts to help people see differently and understand what to do about it. He is an award-winning author and avid keynote speaker, globally recognized as one of the most prominent thought leaders in digital transformation and innovation. Brian has authored several best-selling books including “X,” exploring the intersection of where business meets design to create engaging and meaningful experiences. You can also follow Brian on his website, Twitter, LinkedIn and Facebook

is Principal Analyst at Altimeter Group, a Prophet company. Solis studies the effects of disruptive technology on business and society, and humanizes these impacts to help people see differently and understand what to do about it. He is an award-winning author and avid keynote speaker, globally recognized as one of the most prominent thought leaders in digital transformation and innovation. Brian has authored several best-selling books including “X,” exploring the intersection of where business meets design to create engaging and meaningful experiences. You can also follow Brian on his website, Twitter, LinkedIn and Facebook