Apple CEO Tim Cook told analysts in a third-quarter 2020 earnings call that “contactless payment has taken on a different level of adoption … and I think we’ll never go back.” He said the company was “very bullish about this area,” and believes that there are more things that Apple can do there.

The arrival of the coronavirus pandemic sharply increased consumer interest in using contactless payment methods to avoid using cash or to minimize the touching of surfaces in a physical location. This has benefited both established and emerging digital payments players. As Cook stated, “Apple Pay is doing exceptionally well, as you can imagine, in this environment.”

Although Cook didn’t mention it, in July 2020, 9to5Mac reported that Apple will support QR codes for payment as part of iOS14, the new iPhone operating system. All this points to a rapidly evolving consumer payment system that is creating both competitive challenges and opportunities for incumbent payment system players, including many banks and credit unions that are card issuers and provide payment related merchant services.

The consumer payments ecosystem is a moving target, observes Jared Drieling, Senior Director of Consulting and Market Intelligence at The Strawhecker Group (TSG). “We’re seeing a fluid situation in terms of how consumers are making payments, the tools they are leveraging and where they’re spending,” he says.

The fast pace of change is highlighted by research TSG conducted in partnership with Visa. The study puts some hard numbers on payment trends, particularly contactless cards and mobile wallets. One of the most significant findings is that these changes have proven to be a shot in the arm for fintech players like Square and Shopify. While it is still true that the incumbent providers of payment system services also benefit, the seeds of increasing disruption are being sown as digital payments rapidly evolve.

Cash Down, But Not Out

The TSG/Visa study, conducted in late July 2020, combines data from 569 consumer responses with Visa transaction data. Most of the questions related to how purchases were made — types of payments.

Almost two-thirds (60%) of consumers agree that contactless payment methods (of any type) help manage the spread of the COVID-19 virus. Yet cash isn’t done just yet. Slightly more that a quarter say they will decrease their use of cash after the pandemic ends, but almost half say it will stay the same.

Drieling believes the decrease in use of cash is a trend that was accelerated by, but not created by, the pandemic. The trend will continue, he tells The Financial Brand

because of the demographic factor. Most people between the ages of 16 and 20 for the most part have never seen a check, he says. They use tools like PayPal’s Venmo not only for person-to-person transactions, but merchant transactions.

Contactless Card Use Will Keep Rising

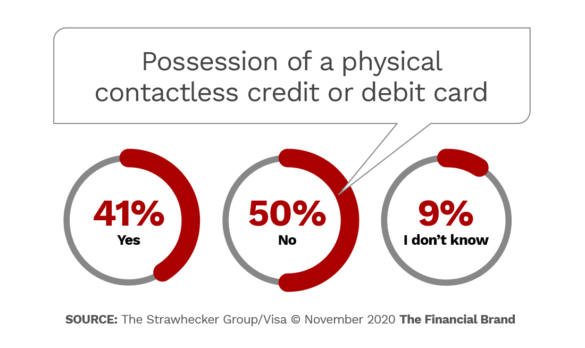

Two out of five consumers have a contactless debit card, according to the TSG/Visa survey. That percentage will keep rising as more financial institutions issue cards with contactless capability in the normal card replacement cycle as the largest issuers have been doing.

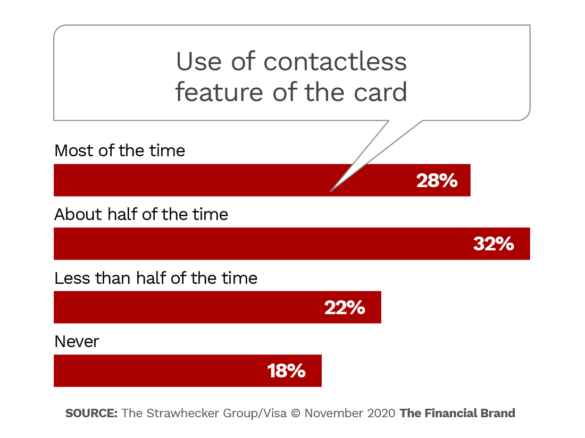

More interesting is the current use of the contactless feature of these cards. Several months into the pandemic the study found that three out of five (60%) consumers who had a contactless card used that capability at least half the time.

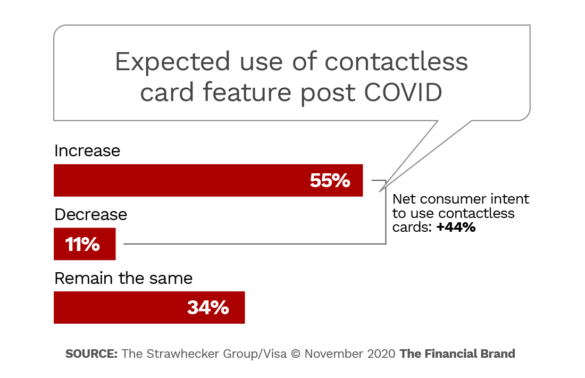

Further, that behavior will likely grow after the pandemic, as 55% of respondents say they expect to increase their use of the contactless feature.

The sharp increase in interest in contactless (card or mobile) has prompted merchants to upgrade their ability to accept these payments. In a study, conducted jointly by National Retail Federation and Forrester, covered in an earlier article, 58% of retailers said they accept contactless cards at the point of sale, up from 40% in 2019.

Drieling says that there is still a lack of knowledge about the newer payment options among merchant checkout employees. The study asked consumers if they had been encouraged by store employees to use a contactless payment option and nearly two-thirds (65%) said “no.”

42% of the respondents who do not have a contactless cards said the reason was “My bank has not sent one.” Another 26% said they didn’t know how to get one, and 27% didn’t want one. Drieling observes that a financial institution that has not yet issued them will be at a disadvantage in terms of remaining “top-of-wallet.”

Read More:

- Four Trends That Will Finally Make Cashless a Reality

- Small Banks Must Fight Harder to Stay Relevant in Payments Space

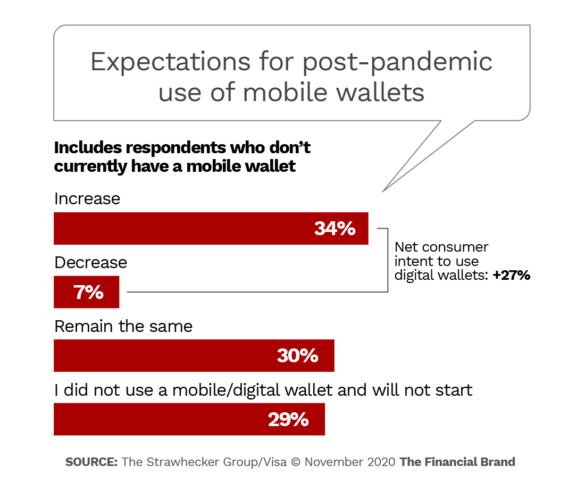

Mobile Wallets Finally on a Fast Track?

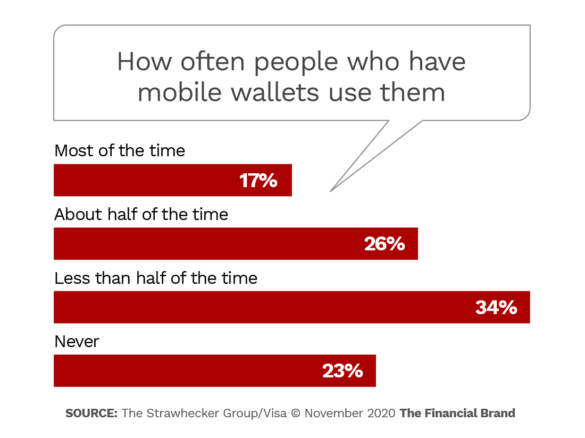

The pair of charts below are revealing about interest in and use of mobile/digital wallets. In the first one, for example, 29% of consumers across all age segments say they don’t have a mobile/digital wallet. That means, of course, that 71% do. That figure is higher than the use of contactless cards among this particular sample of consumers. Further, just over a third expect to increase their use of mobile/digital wallets after the pandemic.

There’s room for growth, however. In the second chart, a sizeable segment of consumers (57%) who have a digital/mobile wallet either don’t use them or use them on a limited basis. Of those consumers who do not have a digital/mobile wallet (the 29%), a large majority, almost seven in ten, simply say “I do not want one” as the reason— about the same as the percentage who don’t want a contactless card.

Another 14% don’t know what a digital wallet is — indicating a marketing slip-up.

Although contactless cards and mobile wallets are sometimes portrayed as competing payment options. Drieling views them as tightly integrated. Using PayPal as an example, he points out that consumers can use either the company’s physical contactless card or its mobile wallet. Either way, he says, all their spending data and purchasing behavior is tracked on one dashboard, giving consumers a centralized snapshot.

Competitive Impact on Incumbents

With the rapid growth of fintechs such as Square, Shopify, Poynt and Clover in the merchant services business, are incumbents at risk of disruption? These newer entrants still rely on the traditional payment system rails — i.e. payment networks, card processors and issuers. As Drieling observes, “Existing players are remaining relevant and are actually receiving some dividends from these fintech partners. But I would say where a lot of these newer technology firms provide value is on the merchant or consumer interface.” Square and others are offering seamless and frictionless tools to merchants, he states.

“Some of the larger payment players in the industry are still relying on technology, quite honestly, from the ’70s,” says Drieling. “That makes it very difficult for them to remain relevant and competitive in this type of environment where we’re talking about integrated software and giving merchants the flexibility to adjust or pivot quickly.”

He predicts that some of these nimbler entities will begin to expand into other related areas and eat incumbents’ market share.

On the other hand, Drieling also notes that banks and credit unions have some significant advantages in the payments space — namely stability and trust. They also lend. It can be difficult for a merchant to untie that relationship, he notes. He labels this combination of factors, “a pretty large moat.”

QR Code Renaissance and Connected Commerce

Two trends suggest that the world of payments will continue to be very “fluid,” to use Drieling’s term.

One is the recycling of an “old” technology, the QR code, into wider use for payments. In Asia, QR codes dominate the mobile payment world. China’s Alipay and WeChat Pay use them to initiate payments, rather than choosing near field communication (NFC). But in the U.S., NFC was considered more secure and became the de facto contactless standard with some notable exceptions, including Starbucks’ payment app.

COVID is partly responsible for a resurgence of interest in QR codes, Drieling points out. Restaurants, for example, have been using them to digitally present menus to diners and let them order that way.

In addition, several major payment players have announced plans to incorporate QR codes in their platforms, including PayPal and Square, according to Scott Harkey, chief strategy officer and Head of Payments at Levvel, in a Forbes blog. He considers Apple’s support of QR codes for payment, mentioned earlier, to be a huge development that could spur increased adoption of these codes by merchants.

Ultimately Drieling believes the whole idea of waving a card or pointing a phone at something in a store will go away in the short term. He believes that stores like Amazon Go that use beacons that track what consumers buy and initiate payment through their mobile phones as they walk out is where things will be in the next three to five years.

He also referenced ExxonMobile’s contactless payment announcement in August 2020. When drivers pull up to the pump their smartphone or car dash display activates that pump and authorizes the transaction including payment. It’s pretty close to a connected commerce environment, says Drieling, and it’s being rolled out to 11,500 Exxon or Mobil fuel stations across the United States.