Even though debit cards remain highly profitable for banks and credit unions (at least those below $10 billion), the same forces of change disrupting consumer banking and payments could spoil the party.

But if financial institutions take steps now to adapt the product and its marketing to mobile-focused consumers, this retail payment stalwart can continue to grow. In fact, there is still a lot of untapped potential in the basic product, according to Dr. Kathy Snider of CO-OP Financial Services.

Millennials in particular represent an enormous potential market for debit cards. As Snider observes, more affluent consumers are less likely to use debit cards because credit cards, with their generous reward programs, are more available to them. But the huge Millennial generation, she says, is well-matched to debit cards.

“Millennials overall are more likely than older individuals to use debit,” says Snider, SVP of Debit, Prepaid and Shared-Branch Products at CO-OP Financial. She suggests banks and credit unions should market debit cards and their features to these entry-level checking account holders. Snider also observes that credit and debit card use goes up and down inversely with the economy’s strength — credit cards up in good times, debit cards up during the down periods.

New Life For a Mature Product

Despite existing in some form for more than 30 years, debit cards remain a core payment product. Debit transaction growth has been in mid single-digit range over the last four years and currently totals 70 billion transactions worth over $2 trillion. According to the Federal Reserve, 70% of electronic payment transactions occur using debit cards.

Based on a survey of credit union customers conducted by CO-OP Financial, the top two uses for debit cards continues to be getting cash from an ATM and paying for things in a store with a PIN debit card — both at 72%. Signature debit usage at stores comes in third at 57%, followed by paying for products or services online at 51%.

Furthermore, the debit card continues to evolve. “We’re seeing the key role it’s playing in push payments that Mastercard Send and Visa Direct are relying on to facilitate person-to-person payments,” Snider points out. “And other P2P services like Zelle are often tied to a person’s debit card. That’s why debit is so important and why we’re continuing to talk about it.”

The traditional building blocks for debit card success are penetration of checking account base, activation, and usage. However, banks and credit unions need to consider three additional success factors today, Snider maintains:

- How to bring the debit card to the mobile platform

- How to tie the debit card to enhanced security experiences through card controls

- How to manage the marketing and incentives — things like debit card rewards

Read More: Key Trends Reshaping Credit Card Marketing

How to Integrate Debit Cards And Mobile

With society at large in the midst of what some call the fourth industrial revolution, banks and credit unions must find and build on the intersection of mobile and debit if the venerable payment product is to continue to grow. P2P payments, as noted, are one example of what’s possible.

CO-OP’s survey probed what consumers thought were the most important features to have included in a mobile banking app. Not surprisingly 80% said “Balance inquiry.” 73% said “Transferring funds between accounts,” while “Making payments” came in at 68%, followed by “Using mobile for bill payment” and “Debit card alerts” both at 54%.

Notably, however, one quarter of consumers felt that mobile payments, mobile account opening and P2P payments were the most important features for a banking app. Snider believes that indicates a growing marketplace acceptance of mobile wallets and digital payments. She also feels the digital payments market is crowded with solutions which can lead to confusion among consumers. This presents opportunities for banks and credit unions if they focus on two points: Ease of use and security.

“What consumers really want is the ability to choose from different payment options and have them all integrated into one mobile banking solution.”

— Dr. Kathy Snider, CO-OP Financial

Regarding ease of use, Snider reports that 68% of credit union customers polled say they would do most of their banking and payments on a mobile device if they had access to a single app handling it all. “What consumers really want is the ability to choose from different payment options and have them all integrated into one mobile banking solution,” says Snider.

Another point to consider, regarding ease of use: If you have instant issuance capability, you can not only put a debit card in consumers’ hands but help them activate it and then help them set it up in their mobile wallet before they leave the branch.

“You want to encourage them to put that card at the top of the wallet,” Snider emphasizes. That’s an increasingly important consideration given the rollout in 2019 of the Apple credit card, which will likely be top-of-wallet for every iPhone user that signs up for it.

Self-Service Security Builds Engagement

“Card not present”(online) fraud is the fastest-growing type of debit-card fraud, which deters many consumers from using debit cards online. Mobile or online card controls help consumers feel more secure and engage them directly in the fight against fraud, Snider states. These controls in a banking app allow consumers to turn a card on and off; set transaction limits; control the type of merchants where the card can be used, and more.

“Card controls go deeper than fraud prevention. They give consumers the ability to personalize the mobile experience.”

— Dr. Kathy Snider, CO-OP Financial

But these controls go deeper than fraud prevention, Snider maintains. “They also give people the ability to personalize the mobile experience. Yes, they are helping keep things secure, but they also help engage the consumer. And engagement equals relationship which drives transaction usage.”

CO-OP’s survey found that only 40% of credit unions offer card controls. Further, those that do offer them have difficulty getting members to use them. Fewer than 10% of respondents have been able to get a quarter or more of their debit card holders to use the controls. The most common ways to encourage use of the controls, Snider reports, is when a member contacts the credit union about suspicious activity (60%); actively promoting card controls through digital channels (52%) and talking about them when the account is opened (40%).

Snider stresses the importance of more effective communication of this capability. “Self-service, personalized controls create emotional connections to consumers.”

How Debit Rewards Create a ‘Halo Effect’

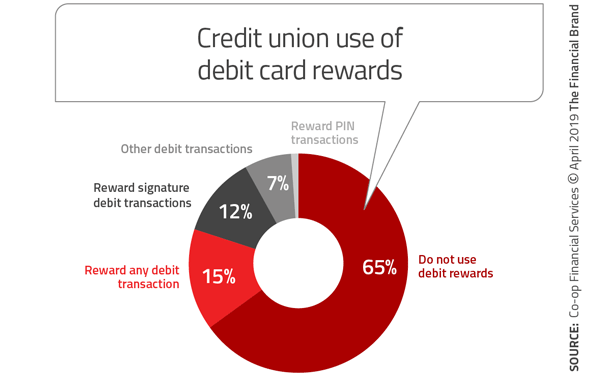

Debit card rewards are another powerful tool to build an emotional connection and engagement with customers. Snider cites Mercator research that says 85% of young-adult debit card users who have debit-card rewards are more motivated to use their cards. About 35% of the credit unions CO-OP Financial surveyed are using rewards programs with 25% considering them, according to Snider.

“According to our survey, 75% of the credit unions that offer a debit-card rewards program say they are effective or very effective at driving card usage,” Snider states.

The impact of rewards is greater than simply boosting usage among a few cardholders. Here’s how:

“Suppose you set up a program that says, ‘Use your debit card 20 times in 30 days to pay for your groceries, buy gas, etc., and you will earn 10,000 points.’ There will be a percentage of members that hit the goal and get the 10,000 points,” says Snider. “But there is also a ‘halo effect’ with these programs. There is a another group of members that won’t hit the goal, but they will have done five, ten, maybe 19 more transactions in the process of trying. And it doesn’t end there. You’ve created a habit and behavior that is sustained once that campaign is over.”