Consumers, small businesses and the banking industry are facing times that have no precedence. There is no guidebook for how to respond to a complete shutdown of an economy, or the actions to take to help support post-pandemic economic survival. With the prosperity of only a couple months ago already a distant memory, how will financial institutions respond to the needs of entire communities as loan losses mount and margins are thin?

Recent evidence appears to illustrate that, once the government-guaranteed PPP loans are distributed and stimulus checks are cashed, financial institutions may be unwilling (or unable) to support the same consumers and businesses they were fighting to do business with before COVID-19. In addition, there may be no appetite for supporting new businesses that were the foundation for much of the economic growth over the past decade.

We are approaching a time when the role of the community bank and credit union may take the spotlight, despite the continued consolidation of assets among the largest banking organizations globally. These local and regional financial institutions have the most to lose if neighborhood restaurants and shops close, or consumers can no longer afford to live in their houses.

There is no doubt that the biggest banks will need to lead the charge, but the industry as a whole will need to assume much of the responsibility for the recovery efforts beyond what the government provides directly.

Credit Availability Decreasing

Over the past couple weeks, Chase and Wells Fargo have announced the curtailment of home equity lines of credit while many other financial institutions have indicated that loans for small businesses will not be available after the SBA PPP loans are distributed. This is just the beginning of what is expected to be a lack of credit available in the marketplace for an indefinite period.

As banks and credit unions do an in-depth assessment of their credit portfolios in the wake of the pandemic, more financial institutions will avoid anything but the most secure of lending opportunities. Given that many small businesses have been shuttered for as much as two months and unemployment is at an all time high, this does not bode well for consumers or businesses hoping to recover.

In an excellent article from Dallas Wells, SVP of Strategic Innovation at PrecisionLender, it was found that most organizations have stopped the vast majority of business lending beyond the SBA PPP loans. “I’m afraid the chaos of PPP is masking some real underlying ugliness for the industry,” stated Wells. “We’re seeing complete breakdowns in parts of the [business credit] market that make even the financial crisis of 2008 pale in comparison. Outside of the federal government, credit markets have essentially ceased operating over the last few weeks.”

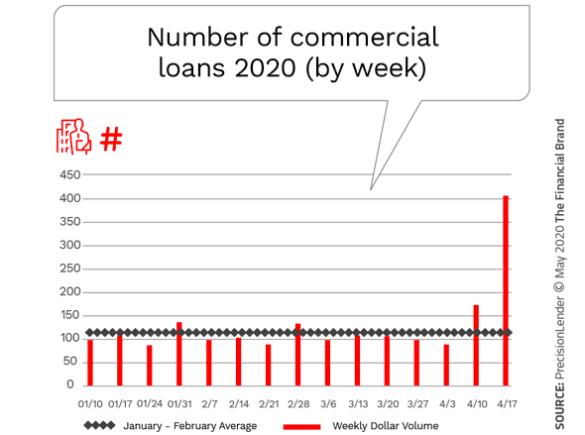

An illustration of the dynamics of PPP lending and traditional business lending can be seen below. A simple loan count for small business and middle market deals booked by week during 2020 show the dramatic change of composition of loans in April. These trends become even more pronounced recently.

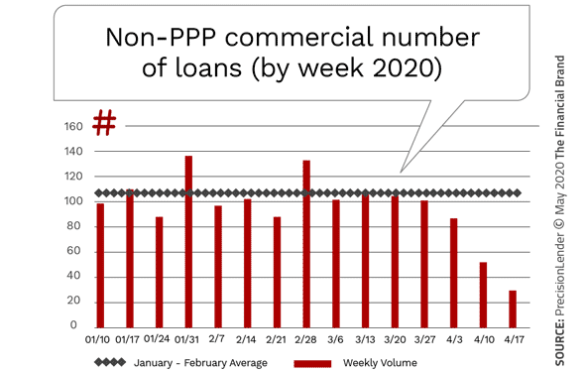

What is concerning from a go-forward basis is that PPP loans completely dominated loan activity, with traditional lending all but drying up. This is against the backdrop that the PPP loan program began on April 3, and non-PPP volume was already 19% below the January to February average. The declines got worse over the following two weeks, at -52% and -73% and are even more pronounced in recent weeks.

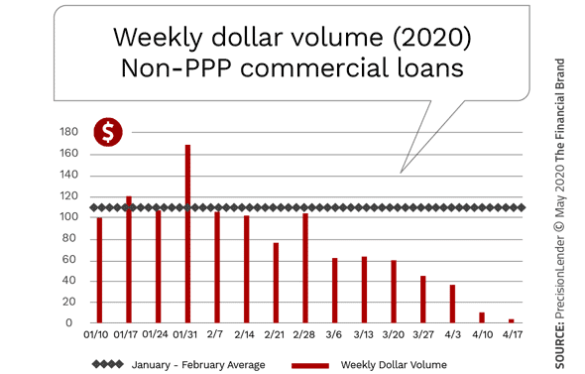

If that wasn’t startling enough, the dollar volume of lending outside of government PPP loans is almost non-existent. Dollar volumes of loans in March started the downward trend, with loans already at 50% of pre-March levels. Once the PPP program was introduced, virtually no traditional loans were funded.

Of greatest concern is that the majority of the lending being done right now is to fund payrolls and not ongoing business operations. Once loans for payroll funding run out, there is little evidence that financial institutions will have a willingness to provide further funding.

Initial Efforts Not Enough

There is much evidence that financial institutions have made significant efforts to not exacerbate the financial hardships already being felt by consumers and small businesses. From fee waivers to loan payment deferrals, a great deal has been done by financial institutions of all sizes not to add more pain to an already stressful situation globally.

While every institution’s response has differed, the creativity and quick responsiveness to unique situations has beeen exceptional for the most part. In fact, the American Bankers Association has created a website for consumers to see what programs are in place on an institutional basis in response to the coronavirus.

Unfortunately, the vast majority of these efforts only prevent a consumer or small business from losing a life’s savings or going bankrupt in the short term. Many will be suffering for months or years to come, without the resources to rebuild credit, continue life as it once was or build a “new normal.”

Much more must be done by the banking community.

Early Community Efforts Must Continue

According to a brief published by the Federal Reserve Bank of San Francisco, it was found that community development officers responded quickly to the early economic impact of COVID-19, such as giving to local nonprofit organizations to address basic needs in their communities. Many financial institutions were leveraging existing relationships with community partners to better understand short- and longer-term need.

The support for community organizations was not universal, however, as some institutions were hesitant to take action in the short term in the midst of uncertainty. The concern was that, as uncertainty increases, the support for organizations that are key to community outreach may not be enough.

The Federal Reserve Bank of San Francisco provided guidance to organizations in a post COVID-19 economy.

- Leverage pre-existing partnerships. Established partnerships and relationships provide the foundation for economic support that can be leveraged in times of need.

- Continue proactive communication with consumers. There is a need to reach out to consumers through various channels using clear and proactive communication.

- Embrace new approaches. Banks must employ their resources to address the unique circumstances of this moment. There is no precedent for this crisis.

- Address immediate needs while looking at systemic issues. Banks must work to leverage resources not just for immediate needs, but to enable a supportive long-term strategy as the crisis unfolds.

- Leverage what exists. Determine how new resources can be deployed using existing infrastructure.

- Develop a systematic approach to understand community needs. Banks need to develop an approach that works for their unique markets.