With a growing number of banking services, there is now a distinct first-mover advantage. Digital account opening is an example. But who wants to be the first to move away from a long-running, up until now successful business model?

Such is the dilemma retail banking institutions face in the U.S. and elsewhere regarding their reliance on fee-based revenue streams, particularly overdraft fees and other penalties assessed, often for sloppy financial habits. Similarly, many financial institutions greatly benefit from poor credit choices made by consumers — using credit cards as a financing option, for example, when another option would be much more economical.

For all the talk about supporting the consumer, financial literacy and sustainable growth, financial institutions benefit significantly from revenue generated by poorly informed or less-than-optimal consumer decisions. Accenture calls this “bad revenue” in its report, “Purpose-Driven Banking.”

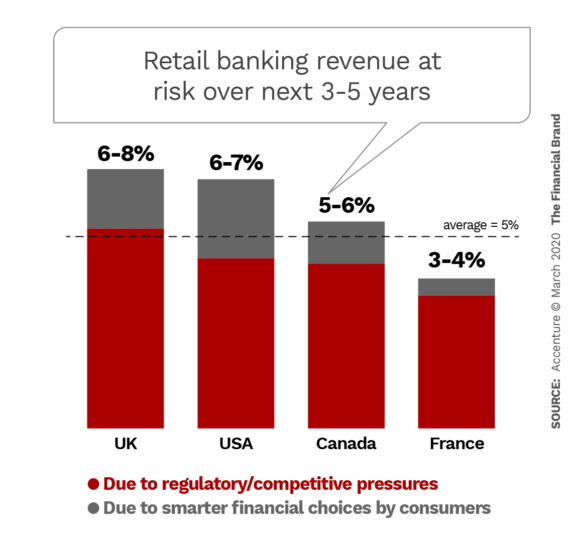

Two massive forces are acting like a giant vise squeezing these revenue streams: increased regulatory scrutiny and fintech competition. The result over the next five years will be a loss of billions in overdraft and other fee income, according to Accenture, representing between 6%-7% of total retail revenue of U.S. financial institutions and about 5% globally.

“Whether in one year or five, the billions in revenues that traditional banks collect annually for basic services and penalties, like overdraft fees, will erode,” says Alan McIntyre, Senior Managing Director and Global Head of Accenture’s banking practice. He maintains there is a way for financial institutions to overcome the lost revenue and set themselves up for a better and more profitable business proposition.

“Whether in one year or five, the billions in revenues that traditional banks collect annually for basic services and penalties, like overdraft fees, will erode,” says Alan McIntyre, Senior Managing Director and Global Head of Accenture’s banking practice. He maintains there is a way for financial institutions to overcome the lost revenue and set themselves up for a better and more profitable business proposition.

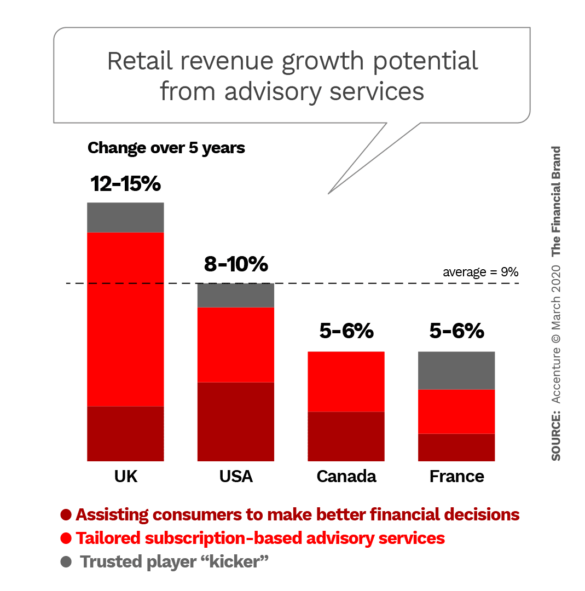

“Banks that proactively cannibalize this diminishing revenue by helping customers manage their money better will earn their trust, which benefits both parties.” Better advice leads to better customer decisions, McIntyre explains, which create more wealth over time — more wealth for banks to help manage.

Accenture estimates that this trust-based revenue increase can amount to a 9% gain on average, more than making up for the decrease in fee revenue. Supporting that estimate is the fact that 55% of the 15,000 retail banking customers the firm surveyed worldwide would pay for additional services from their financial institution if the services helped them with their financial situation. That figure was slightly lower (48%) for U.S. consumers.

Long Road from ‘Soulless’ to ‘Meaningful’

There is work to be done to get there, however, as nearly three in ten U.S. consumers say they have difficulties with their financial institution. Some of these difficulties include unfair product fees, lack of pricing transparency, and lack of help with financial questions. As the Accenture report notes, consumers have grown skeptical that banks always provide advice that is in their best interests.

New fintech competitors pounced on this opportunity, emphasizing a collaborative “we’re in this together” brand position, Accenture states, which has led to considerable success. Banks and credit unions need to “find ways to connect with their customers that go beyond efficient-but-soulless digital transactions and create meaningful digital relationships.” Institutions that do this will be viewed as trusted partners.

Right now, though, the survey found that just 43% of consumers worldwide trust their financial institution to look after their long-term financial well-being. Add to this that more than half of surveyed consumers say they are unprepared for such life events as divorce, loss of a job, or the need to provide support to a loved one. Only one quarter say they have enough savings to cover six months of living expenses.

Read More: How to Build Banking Products Consumers Will Love

How to Help the ‘Neglected Middle’

Accenture says the greatest need — and greatest opportunity for banks and credit unions — lies with the 1.7 billion adults with a net worth in the $10,000 to $100,000 range, which it labels the “Neglected Middle.”

McIntyre says these are the people who are basically treading water. They need to be taught how to make the right choices financially. One persona McIntyre describes is a software engineer living in Brooklyn, N.Y., and making $130,000 a year.

“You would think, ‘He should have a good financial life’,” McIntyre states. “But when you look at how much it costs to live in Brooklyn, including sending a child to private school, the money runs out very, very quickly.”

That persona represents a group that is badly underserved at this time, McIntyre tells The Financial Brand. That’s because on the one hand the cost to advise that group face-to-face is too high to make it worthwhile to financial institutions, while on the other hand the digital advisory (robo) platforms tend to be more investment oriented at present.

“Credit product choices are badly served because banks and credit unions have no obligation to tell a customer who’s borrowing on a credit card, they’d be better off using a home equity line.”

— Alan McIntyre, Accenture

Credit product choices are especially badly served at the moment, according to McIntyre. “Banks and credit unions have no obligation to tell a customer who’s borrowing on a credit card, they’d be better off using a home equity line or an installment loan,” McIntyre states.

Also important for this “Neglected Middle” is how to manage cash flow on the liability side. In that area, at least, McIntyre says “We’re beginning to see a lot more notifications and information. You also have fintechs saying ‘We’ll stop you getting into overdrafts and making bad transaction decisions’.” The consultant believes there is a great opportunity in both these areas for banks and credit unions to come up with solutions.

For example, while the many mortgage disclosure and suitability rules that were put in place after the financial crisis help consumers understand “What’s a good mortgage for you,” that’s leads to a very different discussion than: “Why are you buying a house?” It’s the latter type of financial advice that many people need, McIntyre maintains.

Read More: Digital Banks Forcing Financial Marketers to Revise Checking Strategies

Will People Really Pay for Advice from Banks?

Probably not right away, McIntyre states. There’s a need for the industry to reestablish the permission to charge people for the type of advice just described. “If consumers trust that paying will get help them more help, they’ll pay,” he adds. “But only if you’ve built a trusted relationship with them.”

That will come from the efforts of financial institutions to carry out the first phase of the transition to what Accenture calls “purpose-driven banking” — i.e. walking back from penalty fees and proactively helping consumers manage their money better. That will, over time, earn their trust.

Beyond the policy changes required to do this, these initial steps will be delivered primarily through digital apps using AI-driven advisory tools, McIntyre states.

The second phase of the transition is the value-added part, similar to the “freemium” model used by Spotify and others, according to McIntyre. The basic Spotify service is free, but has ads. The premium service is subscription-based. “If Spotify had started charging out of the gate, it would never have gotten the customer take-up it has,” he states.

Getting to the point where consumers are convinced that the actions taken by their financial institution are intended to be mutually beneficial will take years, McIntyre states.

Accenture’s report identifies three approaches to getting paid for advisory:

1. A Digital Financial Helper improves consumers’ financial literacy relevant to their immediate need. Tools like AI assistants can enable banks and credit unions to make sense of “information everywhere” and answer consumers’ queries in plain human language.

2. An Online Advisor provides personalized customer recommendations on a regular basis. Probably subscription-based, this service would give consumers full access to their data and maintain a dialog about their needs and goals. The consumer acts (or authorizes actions) based on the advisor’s recommendations.

3. A Financial Wellness Visit would conduct financial “health checks” and provide advice based on a customer’s circumstances. Engagements would be human-led, repeated a few times a year, and provided affordably and at scale.

Read More: Branches Should Become Financial Health and Wellness Centers

Will Banks and Credit Unions Have to Ditch Sales?

Financial institutions have spent decades building a sales mentality and approach. McIntyre believes that the sales culture clearly has been at the root of some of the erosion of trust in banking — either by pushing products consumers don’t need or products that get them into trouble like a 100% LTV mortgage. He doesn’t see the need to banish sales. However, the sales effort needs to present the right thing at the right time. “Financial institutions need to realize that the kind of margins that they make through bad customer choices will ultimately be avoided,” states McIntyre.

The alternative to the old model is for banks and credit unions to think in terms of lifetime customer value. Often this will result in a trade-off of short-term revenue to build long-term relationships where both the institution and its customers benefit over time, McIntyre states. The benefit for consumers is the best financial life they can have, he continues, while benefit over time for the institution is an increased depth of relationships.

“That is not how most financial institutions are set up at the moment,” McIntyre states. Most are organized by product sales, which means that the person running the credit card business has no incentive to restrict credit card growth in order to grow the unsecured personal loan business.

“Becoming more focused on lifetime customer value is going to be culturally challenging for many financial institutions,” the Accenture executive states. But if the firm’s research is correct, the trend in that direction is inevitable.