In adverse times, it’s easy to look at the negatives and point out what we could have done — hindsight is always 20/20. Our global marketplace is filled with regrets and I-told-you-so’s of how we all should have better prepared for disruption across every industry.

However, in the midst of the coronavirus pandemic, it’s also important that we recognize the growth in humanity that has occurred. The world is still moving, albeit in a new way. Non-technical industries have completely turned their business structures on their head; other businesses are realizing that partnerships can expedite processes; and working from home has completely lost its stigma as the lazy man’s game.

This forced innovation has demonstrated the dexterity of the modern business marketplace. We know while we can’t predict when business disruption will strike, we have proven that we will rise to the occasion. In the financial industry, while markets are dropping, and consumers are uncertain of how they will afford tomorrow, banks and credit unions have been there.

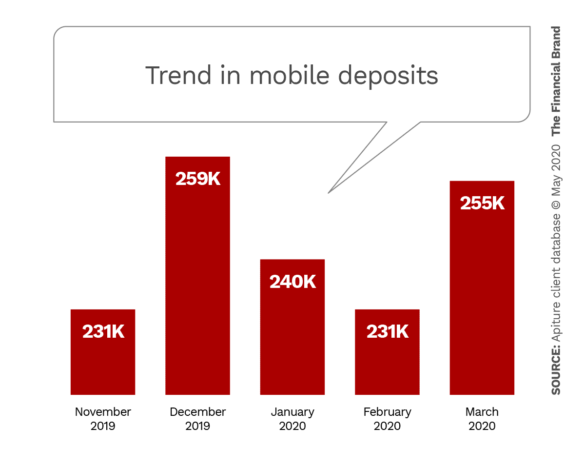

Mobile deposits have seen a dramatic increase rivaling the economic uptick of the holiday season. There was a 5% increase in deposits in March over the prior year.

Through services like mobile check deposit (did someone say stimulus check?), hands-free person-to-person payments, or just having a person to assist in customer service issues, financial institutions have been where their customers and members have needed them. Consumers have taken advantage of financial services anytime, anyplace, regardless of what is going on in the world. The transition for banks and credit unions from routine, day-to-day operations to remote setups has been so seamless that consumers haven’t noticed a single operational change. It’s a testament to the community banks and credit unions putting their customers and members first, and it’s what’s driving our businesses to the new normal.

Keys to Success During Coronavirus Pandemic

Here’s how financial institutions have set themselves for success:

• Supporting person-to-person payments.

When COVID-19 grabbed hold of the economy and shut the doors of many businesses, the self-employed found themselves able to work, but with the threat of spread, found little to no interest in contacted payments. A barrier emerged for all those split rent payments, handyman work, monthly allowances and more. Cash suddenly didn’t work anymore.

Only 14% of consumers are considered to be completely digital — using only digital channels for their banking. The rest fall somewhere along a spectrum, and many find it easier to pay by money order, check or cash. While many institutions were trying to figure out the justification for spending to jump onboard person-to-person payments, their consumers may have been going elsewhere for PayPal and Venmo, or sticking to the physical methods they already knew.

With COVID-19 came something most consumers weren’t ready for: a full seizure on people’s willingness for anything involving potential contact with the virus. Even taping a check to a door posed a risk. For many people, it was the call to adopt digital person-to-person payment structures. For many financial institutions, this was an opportunity to educate and grow person-to-person payment services within their mobile applications. Prepared institutions not only already had the services at the ready, they could teach their users how to use them. Many people who feared being unable to collect payments could rest assured it wouldn’t be an issue.

The sense of a socially distanced community has become one of the strongest forces against the pandemic. Person-to-person payments have enabled family and friends to help loved ones out of difficult times without the need of any physical exchange. With the already deployed services from financial institutions, people focus on what matters and have the power to help at their fingertips, without downloading or opening any other accounts.

• (Mobile) Check (Deposit), Please.

Just ask the 100 million Americans eager for their pandemic stimulus check: Waiting around is not only frustrating, but can be the difference between financial security and stress. Waiting is half the problem, once a check is received — how would a consumer safely deposit a physical check into their account? With the existing restrictions and recommendations in place, just getting to a bank or credit union is not only an additional risk but could be a violation of various mandates set into place to keep us safe.

Banks and credit unions want to keep their staff at lower risk as well. Touchpoints, even if just through a teller window, puts all staff at risk with every transaction.

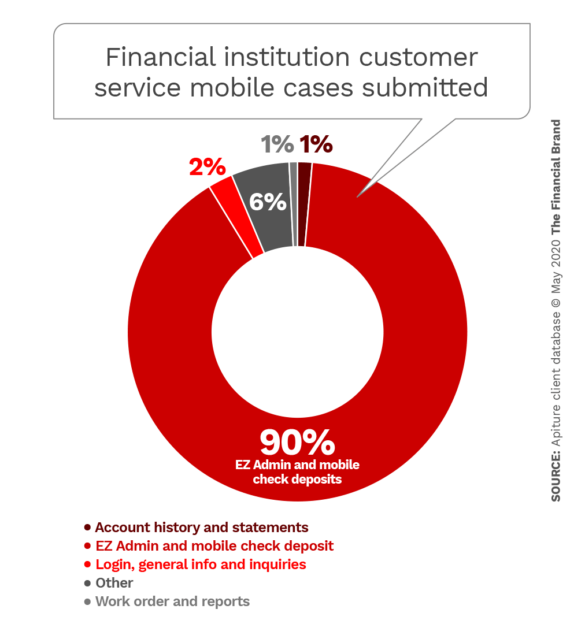

Mobile check deposit is a dominant driver of customer support inquiries.

It’s precisely these reasons why banks and credit unions have risen to the occasion to provide services such as mobile check deposit so their consumers can skip a trip to a branch. In fact, this is so commonplace for customers and members that it’s not even a question of how a check will be deposited — successfully solving a consumer need before it’s even recognized.

Imagine a high-risk individual having been issued a stimulus check to deposit but being unable to deposit it safely. Institutions that have deployed mobile check deposit have not only put their customers and members first for convenience, but have also safeguarded their health and wellbeing, and that of their own staff.

Digital Banking Adoption Advances Amid COVID-19 Period

Banks and credit unions have long been faced with the trends of online and mobile banking adoption. Up until now, there has been little that financial institutions could do to encourage specific groups of non-actors to change the way they bank in adoption of digital services. This wavering among demand has seen many financial institutions choose not to offer services like mobile check deposit and person to person payments. Not being able to justify the spend for the segment of customers that demand these services has been the scapegoat for non-innovators.

Without a doubt, we are living in a world ruled by digital services. Whether this was realized before or as a result of COVID-19, all sectors of industry are facing how our world truly turns. Virtual collaboration and innovation are our new reality. With these realizations comes a greater responsibility for institutions to educate their users.

Forced adoption comes with unique challenges. Adoption, albeit aided by necessity, is frustrating for consumers — change is hard and resisted. Financial institutions have found their successes in displaced tellers and greeters becoming stewards for customer success.

Strong customer service serves to make this new forced adoption a guided and eye-opening opportunity for users. It turns the frustrations of unknown processes into recognition of value-adding services. This customer service goes beyond the expected hotline of password reset questions and empowers a relationship beyond Q&A.

In the case of many financial institutions, newfound digital services mean members and customers are banking at all hours. Increased growth of transactions after dark warrants an increased need for institutions to be there for users at all hours for support. While this 24/7 support is needed, these unprecedented times also come with budgetary needs to reduce labor hours, putting stress onto an already stressful situation. Institutions have been able to have exceptional service and support by employing low-cost user-direct outsourced support. User-direct support employs a secure and expert team to provide branded support outside of a financial institution. These services can be hired 24/7 or anytime when a financial institution’s staff is unavailable.

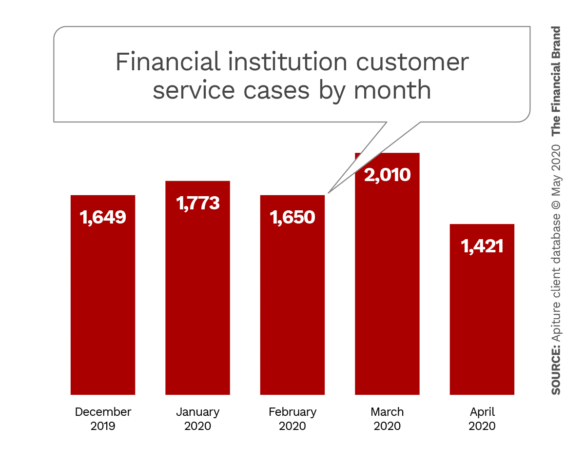

End-user support is seeing a significant increase during the COVID-19 pandemic’s onset. There was a 16% increase in March from the prior year.

Further, successful financial institutions have refocused their customer service team to provide tools and content that helps their users complete digital services with ease. Videos, guides and dedicated expert staff identify and deliver top-notch support services to support adoption and continued use of these digital services.

A New Frontier for Financial Institutions

The pandemic-induced developments in digital banking services are not fleeting. While the impacts of the coronavirus will lessen over time, the lessons learned for consumers and institutions alike will only deepen the reliance on digital services across all industries.

Most banks and credit unions were ready for this type of need. However, these ever-changing innovations continue to require the best-in-class technology and support.