During an early June investor call, Gordon Smith, Chase’s Co-President and COO, who runs the megabank’s 4,900-branch network, addressed a question about branch-based versus digital banking during the pandemic. Gordon observed that in the March-to-May period, the number of mobile and digitally active customers edged up “minimally.” While those who were digitally active did much more on their devices, he said, the majority of Chase customers are still not digitally active, “even as we go through this pandemic experience.”

Smith expects to see branch traffic stay down for some period of time. “We’ll obviously watch,” to see at what level it normalizes, he said. “But I still think we’ll see meaningful traffic through the branch network. I really do.” An interesting takeaway from this, Smith said, is that “consumer behavior can sometimes take a long time to change.”

At the other end of the size spectrum, Michigan’s Community Choice Credit Union, with 22 branches and assets just over $1.2 billion, has seen much the same slow-to-change behavior. Branch traffic during the pandemic was down sharply at first and is gradually coming back, but is likely to remain lower for an undetermined time, according to Brian Wilson, Vice President of Retail Delivery. Still, many people still showed up in person — by appointment or drive-through.

“It takes more than a pandemic to disrupt peoples’ behavior,” Wilson observes. “If we give them the opportunity — i.e. reopen our branches — they will behave as they want to behave.” For the majority of members at Community Choice, that means coming to a branch to do transactions, despite the fact that the credit union, like Chase, has advanced digital capabilities to open accounts and apply for loans.

As further evidence of why branches have proved to be so resilient, a study of about 1,100 consumers by consulting firm Simon-Kucher & Partners — released in mid June — found that more than half (54%) would prefer to only open an account with a financial institution that has physical branches. That compares with 43% who are okay with an institution that either does or doesn’t have branches. Only 3% preferred a digital-only bank.

A Cautious Reopening Not Much Different from ‘Closed’

The gradual easing of the coronavirus lockdown has enabled many financial institutions to begin reopening their lobbies to customers. The process varies greatly by location and by institution.

A group of community banks and credit unions participating in a mid-June Rapid Action Research survey conducted by Rivel’s CXLign – Banking unit found that nearly half (46%) had at least three quarters of their branches currently open for in-lobby banking, while about one-third (31%) had yet to reopen any. By July 1, however, only half as many (15%) expected to have no branches open.

“We have taken the approach to reopen slowly since we have had no complaints from customers,” one retail banking executive observed in the survey’s verbatim section. “We want to protect our employees and customers alike.”

A widespread practice among banks and credit unions at the beginning of the lockdown period was to close branch lobbies to walk-in traffic, but allow customers to come in by appointment, often with limitations on how many people could be in the branch. Various government guidelines on use of masks, distancing, etc., were also followed. For the most part, “reopening” doesn’t change that situation except that some banks and credit unions now allow walk-ins.

Community Choice, for example, has “unlocked our lobbies,” says Wilson, but is limiting entry to maintain a one-to-one ratio (customer to on-site staff). A staff member is at the door to encourage customers to wait in their cars rather than congregate, and texts them when they are able to come in.

“It’s not our permanent solution,” says Wilson, “but for the time being it is what we’re doing.”

The staffer at the door also advises people that rather than wait they can use the drive-through or one of the credit union’s digital alternatives. Community Choice completed an upgrade of its online banking system in 2019 so that consumers can open accounts or apply for loans digitally. There is very little reason for them to come into a branch, says Wilson. Yet many still do.

The Michigan credit union also continues to actively promote and use appointment scheduling. Customers can set appointments on their mobile phones or a contact center agent can do it for them. Wilson says branch staff review the appointment lists to see what the purpose of the visit is. They reach out to the member on the day of the visit and in a number of cases are able to handle their needs remotely.

Not every financial institution closed their branches during the lockdown. Frontwave Credit Union in San Diego, for example, kept all but three of its 14 branch lobbies open, but would limit access to between one and five customers at a time, according to Chief Marketing Officer Todd Kern. It has since reopened two of the three closed branches. However, Kern says that all the safety precautions implemented earlier remain in place, even as California has gradually reopened.

“We continue to take a conservative approach, and utilize all of our ‘new normal’ processes,” says Kern. “With signs of a potential fall resurgence [in the coronavirus], we are prepared to take this approach through the year, if necessary.”

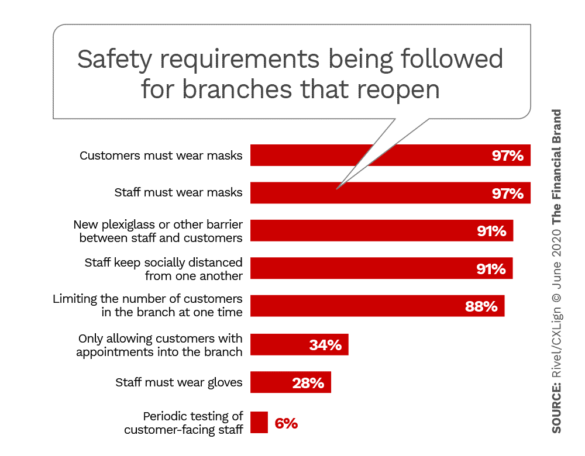

The chart below, from Rivel’s Rapid Action participants, indicates a significant uniformity towards in-branch safety.

Read More: The Future of the Branch Experience

Traffic Report: How Many Are Returning?

Simon-Kucher asked consumers if after lockdowns were lifted they would change the frequency of their visits to financial institution branches. Just over two in five (42%) expected to reduce branch visit frequency compared with half (52%) predicting no change and 6% planning to visit more often. The younger the age group, the more likely branch visits were to decrease.

What are institutions actually seeing? Frontwave, which has assets of close to $1 billion and about 110,000 members, saw a 7% decrease in branch traffic in March, followed by a 31% drop in April. COO Randi Brooke says branch traffic returned significantly in May, but was still 9% below pre-COVID levels. Brooke notes that by remaining open, Frontwave saw members of other credit unions that participate in shared branching services migrate to its facilities.

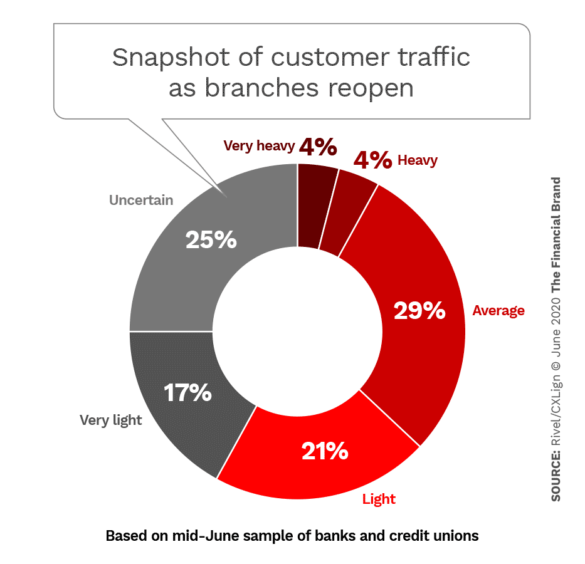

As can be seen in the chart below, the returning branch traffic among the banks and credit unions responding to a Rivel poll, was split almost evenly between “normal”/”heavy” and “light.” It’s based on a small sample, but does give a sense that even with continuing branch restrictions in place, consumers have not abandoned their branch habits.

Brian Wilson ran some numbers in response to a query from The Financial Brand and found that branch transactions (closely correlated with branch traffic) dropped 50% in April and May from the January and February levels. He notes, however, that there was only a 36% decrease in the number of new accounts opened in-branch in the same period, excluding Paycheck Protection Program accounts.

“We’re not encouraging people to come in, and not discouraging them. We’re just informing them.”

— Brian Wilson, Community Choice Credit Union

After being open for a week and a half in June, Wilson says that compared to the same period in 2019, branch transactions had risen to about 69% of the previous year’s level. It’s not an opening of the floodgates, he says, but people are coming back. The credit union is using its website, Facebook page and email to let customers know about the reopening.

“We’re not encouraging people to come in, and not discouraging them,” says Wilson. “We’re just informing them.”

Who’s Coming Back … and Why?

Wilson ran other numbers regarding branch activity during the height of the pandemic and into the reopening period and found some surprising trends.

“We saw virtually zero change in the percentage of Baby Boomer members that were visiting us before or during the pandemic.” He expected the percentage to be higher and the percentage of more tech-savvy Gen X, Y and Z members to decrease. But the percentages stayed almost the same for each demographic.

Frontwave’s Randi Brooke notes that during the pandemic period they are beginning to see a “slight shift” at some branches to younger consumers.

“Younger members who want advice and are looking to develop a relationship with their institution,” are coming in. She adds, however, that deposits, withdrawals and other transactions are still the primary reasons for branch visits.

Likewise Wilson says that even though the total number of branch interactions declined, the percentage that were deposit/withdrawal transactions didn’t change as he expected it would.

Read More: 5 Reasons to Think Twice Before Closing Branches

Branch Changes, Short- and Long-Term

Despite the fact that traditional branch transactions continue, and probably will for some time, there was no disagreement that what had been a steady rise in digital transactions clearly spiked as a result of the pandemic. At the peak, Frontwave’s Todd Kern says digital money movement jumped 38%, powered by significant increases in mobile remote deposit capture.

“The COVID crisis opened our eyes to move even faster toward digital self-service member solutions.”

— Todd Kern, Frontwave Credit Union

“The COVID crisis opened our eyes to move even faster toward digital self-service member solutions,” says Kern. “We saw a significant change in member behavior during the crisis. Although we expect a right-sizing to occur when it comes to branch traffic — to what extent, time will tell —we do expect member reliance on the branch for transactions to continue to decrease.”

The marketing exec says the institution’s leadership is reviewing the efficacy of all its branches. Yet long term he says, “We continue to view the branch as a place for consultation, guidance, advice, and ‘brand-width’.” As a result the institution is moving away from large-square foot transaction-based layouts.

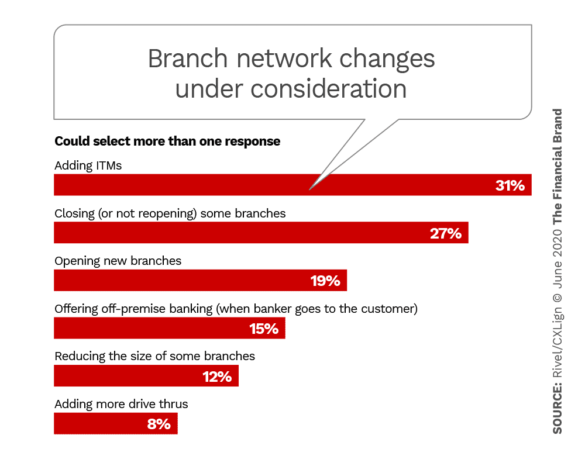

Changes planned by other banks and credit unions to their branch networks as a result of their pandemic experiences are shown in the chart below.

Community Choice doesn’t spend a lot of energy worrying about the cost effectiveness of the branch channel even as transactions keep declining. “Our approach is to let the market guide us,” says Brian Wilson. “We’re not going to dictate to the members what the definition of convenience means to them.”

“If you’re looking at banking as strictly transactional you can make a really good argument for going 100% to not having branches. But it’s not just transactional. There’s more to it. It’s social. It’s psychological. It’s part of a routine. We believe electronic banking enhances the experience, but doesn’t replace it.”