Research Predicts All U.S. Bank Branches Could Be Shuttered by 2034

Is the decades-long debate over the future of branching finally coming to a dramatic conclusion? An analysis of years of state and national branch data reveals that physical bank branches could disappear if trends continue on their current trajectory. Consumer data from a concurrent study offers some support, but also a reality check on digital-only banking.

By Bill Streeter, , former Editor-in-Chief at The Financial Brand

Simple Subscribe

Subscribe Now!

Plenty of predictions for the “end of branches” have come and gone and never panned out. At times the branch “dinosaur” defied the prognosticators and not only lived, but increased in numbers. Is this time different?

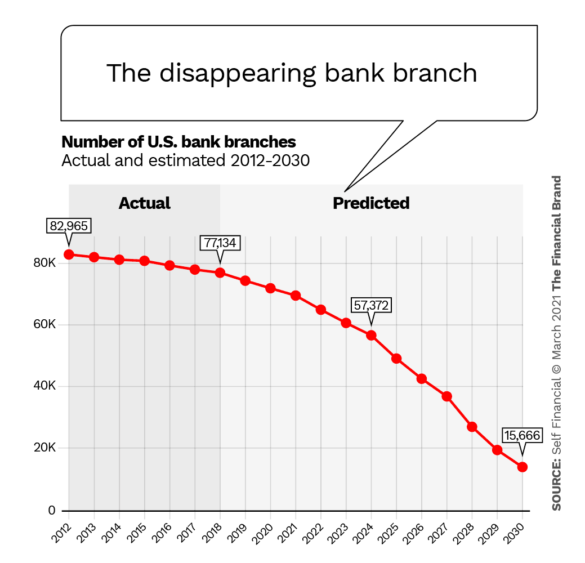

Many factors are different now and a new and detailed analysis of branch closing data by Statista, commissioned by Self Financial, suggests a significant change. According to the report based on the analysis, the number of bank branches in the U.S. fell by 6.5% from 2012 to 2018. That’s an average of 902 a year. For every 15 branches open in 2012, one is now closed.

More importantly, the rate of branch closures has been doubling every three years. Between 2012 and 2015, the closure rate was 0.81% per year. From 2015 to 2018 the rate reached 1.6% per year. Based on that and other factors, Self predicts that by 2027 there could be fewer than 40,000 branches across the U.S. and by 2030 fewer than 16,000 remaining. That would put the number of branches at that point at 1965’s level. From there it’s just a short statistical step to zero.

Since 2012, 40 states have seen a net decline in the number of bank branches. An interactive map in the report shows detailed state-by-state statistics. On a percentage basis, Maryland saw the biggest drop at 12.6% (202 branches). But the largest reductions by number were seen in Florida (529), Illinois (395) and Pennsylvania (379) with Michigan and California close behind.

Counterpoint:

Naysayers will scoff, pointing out that the orgy of branch closures of 2020 was a speedup of a long-running correction, but hardly heralds an abandonment of in-person banking.

To be sure total elimination of branches is hardly likely, especially considering that some institutions continue to selectively open physical locations for generating new accounts, deposits and loans even as they expedite their digital capabilities. Consider, however, that the data used for the Self Financial prediction did not include closure numbers for 2019 and 2020.

2019 saw about 1,400 net branch closures, down from the previous two years, but in 2020 the net closures jumped to 2,284, according to S&P Global data. Some experts predicted that torrid pace would accelerate further in 2021 reflecting the upsurge in digital banking use during the pandemic. But even if it dropped to, say 2,000 or 1,900 net closures, that could increase the pace from what the Self Financial study predicts.

What the Data Means for Traditional and Online-Only Banks

In some respects the industry’s accelerated closure of branches may have moved ahead of consumer preferences. Sure, many more people downloaded apps or signed up for online banking as a result of pandemic-related branch closures. Several of the challenger banks have seen big jumps in new users. But studies show consumers continue to like the ability to meet in person.

Self, a U.S. challenger bank targeting consumers new to credit or without access to traditional financial products, wanted to probe further into the implications of the branch data. In addition to the Statista analysis, the company commissioned a study of just over 1,100 U.S. consumers in mid summer 2020. The results, contained in the same report, present a more nuanced picture of the future of branch banking than the stark prediction above. Traditional and challenger institutions may come away with anxiety, hope or both from some of the data.

For example, almost half the sample (46%) thinks the current banking system needs to change. That statistic indicates much more upheaval to come. Advantage challengers.

However, when asked how much they trust the current banking system versus online-only banks 70% of consumers say they trust institutions that still have a physical presence while less than half (47%) say they trust online-only institutions. Advantage incumbents.

Read More: Why Bankers Won’t Ditch Branches, Despite Digital’s Explosive Growth

Consumers Preferences for In-Person Vs. Online-Only

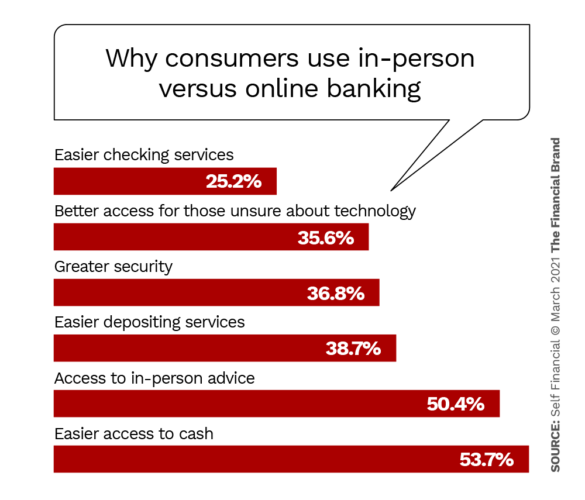

The survey sought the reasons why U.S. consumers continue to use branches. It asked what advantages branches have over online-only banks. Even though the survey was conducted in mid pandemic, the top advantage cited was “easier access to cash,” followed by “access to in-person advice.” (The question period covered a 12-month period that began about six or seven months prior to the start of the pandemic.)

The researchers found the “access to cash response” surprising considering that use of cash has been trending downwards for some time and because cash became a safety issue during the pandemic. So that particular branch advantage may or may not be sustained over time.

The advice point, however, does corroborate what many in the banking industry have stated: that branches are moving from a transaction focus to an advisory focus.

Key Insight:

The one quarter of respondents who found it easier to cash or deposit checks at a branch along with the 36% who are not that comfortable using digital technology suggest online and mobile functionality — and consumer education — still has a long way to go.

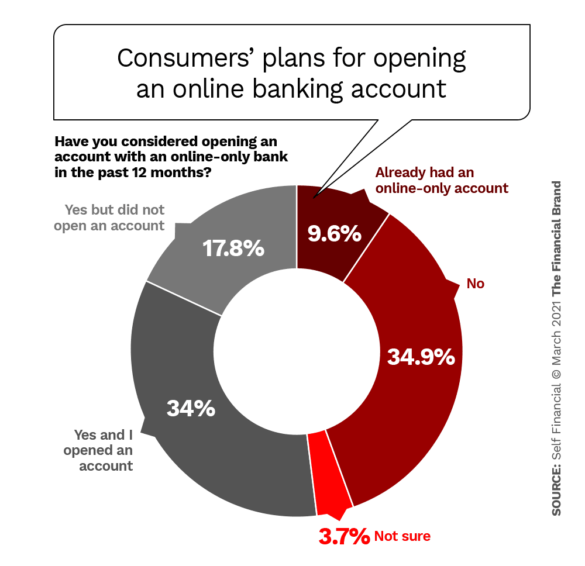

The pie chart below shows strong consumer interest in online-only banking, with more than two in five consumers opening such an account or already having one, and another 18% having at least considered opening one.

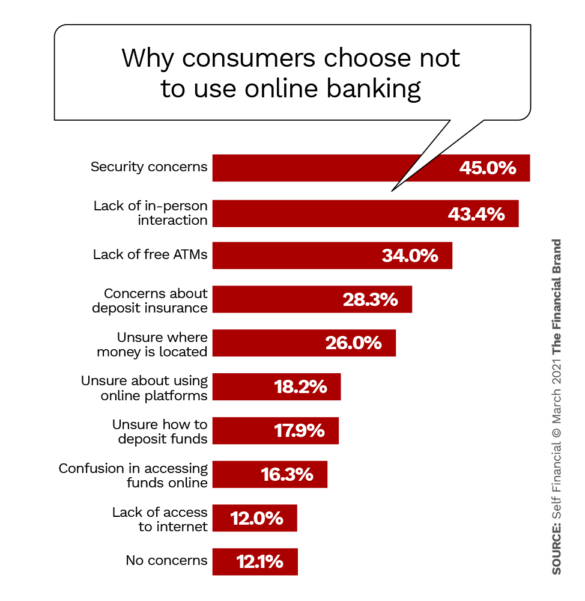

As a challenger bank, Self naturally was interested in seeing why more consumers don’t use online-only banks. They asked people what “puts them off” about this option. The responses, below, give an indication of why traditional institutions are still used by 89% of the respondents.

With the exception of “in-person” interaction, most of the rest of the online-only negatives can be addressed through education and increased security measures. In other words, there is not much standing in the way if traditional institutions don’t measure up digitally.

What Consumers Want from Financial Institutions

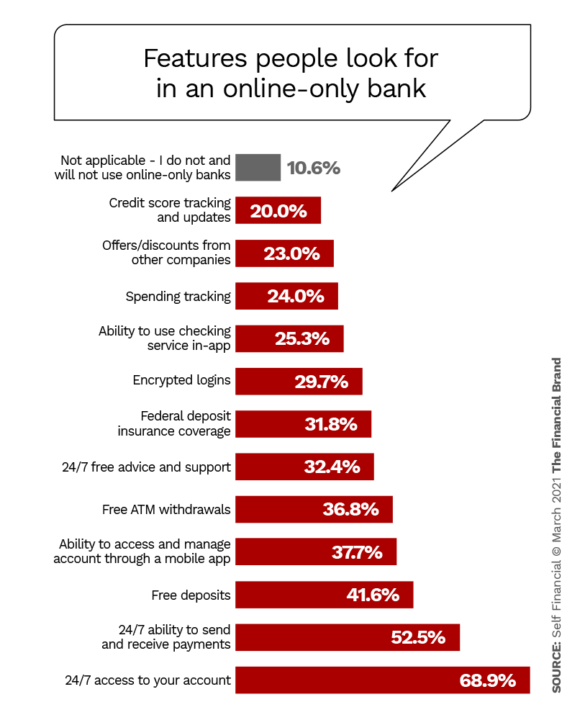

The survey also sought to uncover what people want in an online-only institution. The results, shown in the chart below, provide insights not only for the relatively small (but growing) number of such institutions, but are also a roadmap for banks and credit unions as they seek to enhance their digital banking capabilities.

While some of the features shown above are fairly basic, it’s clear that immediate and convenient access to financial data and payment capabilities is an expectation, along with several forms of tracking and advice.

Self couldn’t resist asking consumers if they expected online-only banks to outnumber traditional financial institutions within 20 years. 55% said “yes” and another 28% said “maybe.” Two decades is a bit of a stretch perhaps, but the question did at least flesh out the fact that consumers expect the digital banking trend to not only continue, but expand.

Citigroup’s new CEO, Jane Fraser, in a comment cited at the end of the report, offers one response to the data reflected in the study:

“We believe we have the model of the future – a light branch footprint, seamless digital capabilities and a network of partners that expand our reach to hundreds of millions of customers.”