Why are some consumers loyal while others are more likely to switch? What drives consumer satisfaction in banking today? According to a report from Bain & Company, the answers to these questions are largely dependent on the delivery channels a consumer chooses to use.

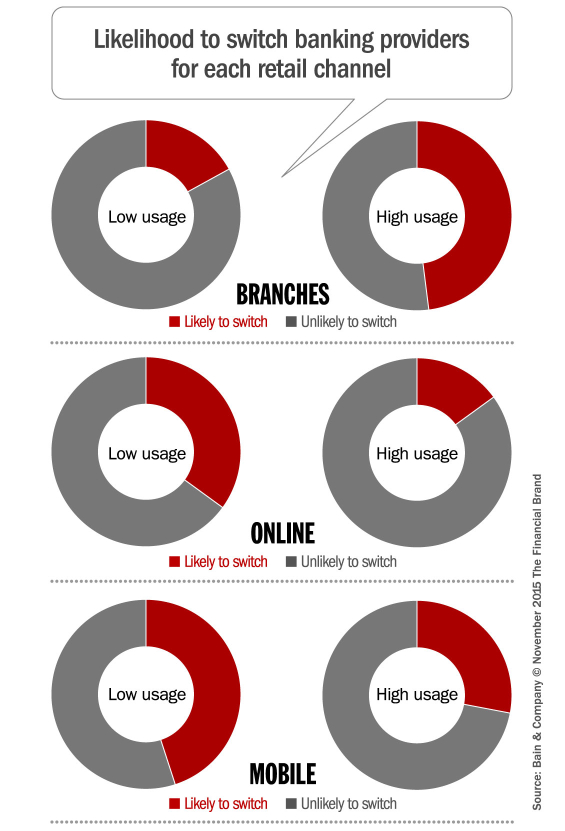

In its sixth annual report on consumer banking behaviors, Bain found that consumers who rely on digital channels for their banking needs are 40% less likely to switch vs. those who use mobile rarely or never. Conversely, those who frequently use branches say they are three times more likely to switch compared to those who rarely use branches.

In simple terms, the more people use branches, the more likely they are to switch.

Gerard du Toit, lead author of the research and a partner at Bain, blames this on the outdated branch model still used by most institutions.

“In the U.S., 60-70% of branch interactions in a typical bank are either bad or avoidable,” du Toit says. “Most of the time, a branch visit results in an inferior customer experience and comes at a higher cost for the bank. Clearly, the branch as currently configured is headed for extinction.”

He could be right — the branch experience might be the source of consumers’ aggravation. Or it could be a symptom of broader issues. Perhaps financial institutions provide poor service and inadequate support in other channels for the (unnecessarily) complex products and processes they offer. When consumers get frustrated in other channels and need help, they head to a branch. In other words, frequent branch usage could be a reflection of an institution’s overall experience. If your products suck and your service sucks, of course people will need help more often, and they will often seek that help in a branch. Eventually, they may throw up their hands in despair and ultimately switch providers. But when an institution provides a seamless and intuitive experience — in any channel — there will be less friction, and thus less need for service and support.

Bain found that higher mobile usage generally correlates with less branch usage, but it’s not a one-to-one relationship. Although routine interactions through mobile channels have increased dramatically over the past two years, routine branch interactions declined much more slowly as it takes time and effort to change customer habits. For every 100 mobile interactions, on average, there’s a decline of only about 16 interactions at the branch.

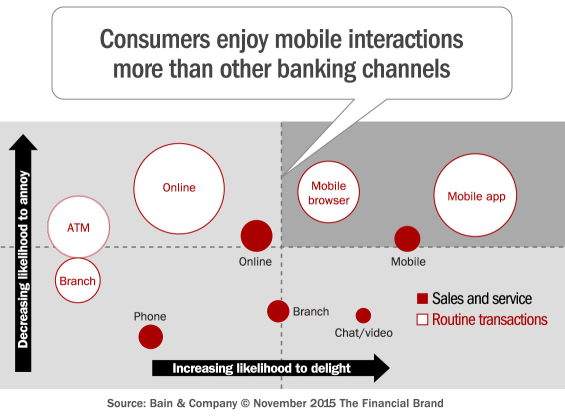

In 10 of the 17 countries surveyed, Bain’s research reveals mobile banking interactions now exceed interactions in the more conventional online banking channel. And mobile apps used for routine transactions are one-third more likely to delight consumers compared to similar transactions in the branch, whereas a routine branch visit is 2.4 times more likely to annoy.

But most consumers — including Millennials — still use a combination of both physical and digital channels. These omnichannel consumers tend to give their primary banking provider higher loyalty scores than branch-only or digital-only customers, and they are more likely to buy a product from their primary bank or credit union. Also, the more interactions that omnichannel customers have with their institution, the higher their Net Promoter Scores.

Most banks and credit unions are trying to shift routine transactions — such as deposits and cash withdrawals — away from their branches and into digital self-service channels instead. As branches shed transaction volume, the prevailing wisdom says financial institutions should increase sales and service activities in their brick-and-mortar locations. Yet, even as more banking activities go mobile, a major challenge for institutions is identifying the right sequence of moves for satisfying consumers through a great mobile experience, while funding the investments in digital channels through cost reductions in the branch network.

For the average bank, Bain says the most critical first step is to focus on improving the mobile experience — make it fast, intuitive, convenient and capable of handling consumers’ basic needs. In many cases, this means eschewing a mobile website in favor of a mobile app. Why? On average, Bain found consumers were using mobile apps twice as often as mobile web browsing for routine interactions, and apps were consistently more likely to delight.

The next step is to increase awareness and drive adoption.

“Just because you build a mobile app doesn’t mean customers will come,” says du Toit. “Banks need to take deliberate actions to inform customers about the app’s benefits and encourage adoption at every opportunity.”

Next, banks must improve on their product sales capabilities in digital channels. Nearly 30% of consumers are already using mobile channels to research or purchase banking products, and roughly 60% of buyers are using a combination of both digital and traditional channels for their research and purchase.

But marketing alone isn’t going to fix the problems banks and credit unions face. There’s more to the sale and marketing equation than just effective messaging. Bain says financial institutions must fundamentally retool their banking products and processes to make them simpler.

“To make the product research and purchase experience shine on a mobile device, the products themselves must be reworked to make them easier to understand. The internal processes must also be overhauled to simplify the chain of activities,” said du Toit. “This is essential to stemming the ‘hidden defection’ issue we detailed in last year’s report – more than one-third of existing customers bought a product from a competing bank during the year.”

To succeed, Bain identifies six new capabilities that banks and credit unions must embrace:

- Extraordinary design discipline, with special consideration given to the small screen and slow typing speed of impatient users.

- Radical simplification of products, processes and communications.

- Personalization powered by good data and analytics so that only relevant information is displayed to the user

- Contact methods that allow for anytime, anywhere chat and video calls with fast authentication

- Much faster development cycles to keep pace with new functionality and consumer expectations

- A new operating model that provides organizational agility, based on breaking down barriers that divide internal departments and a willingness to collaborate externally

To download a PDF copy of report, “Customer Behavior and Loyalty in Retail Banking: Mobilizing for Loyalty,” you can click the following link (instant download — no registration required). You can also play with a nifty interactive chart showing which channels annoy or delight consumers in 17 different countries by clicking here.