I recently had a debate with a credit union board member about the need for branches, as we discussed the changing role of branches in delivering retail financial services to their members. The board member was making the case that perhaps now was the time to stop investing in building new branches.

Anyone who has known me during my 40-year career knows that I’m a believer in branches and the critical role they play in supporting customers. So, if they were listening to this exchange they might have been surprised when I agreed with the board member.

Why the change of viewpoint?

After revisiting recent branch and industry trends the last few months during the pandemic, I’m convinced that the traditional role branches have played as part of a multi-channel delivery system is ending. The question isn’t “if” but “when.” But halting investment in new branches isn’t the end of the strategic discussion.

Branches As We Know Them Are Fading Faster

Branch traffic has been declining for over a decade as first online, then mobile channels were introduced, offering more convenient ways to conduct routine transactions.

First, they offered basic information services like balance inquiries, then came account transfers and bill paying. The next big transaction migration play came with mobile deposit. Each iteration removed more reasons for branch visits, just as deposit-taking ATMs did decades ago.

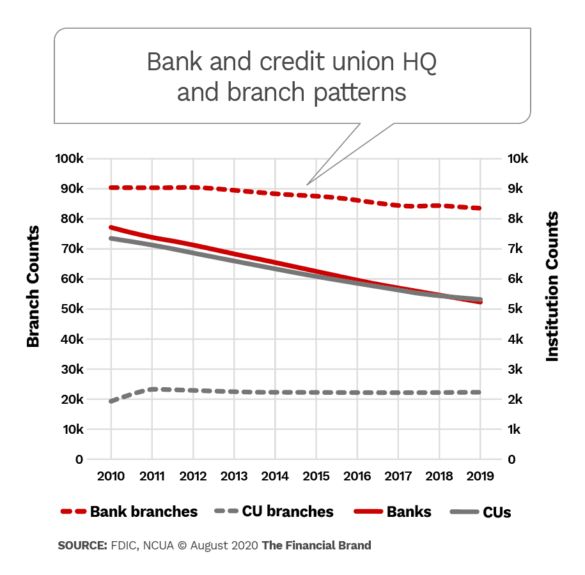

The result of these transaction migration efforts has been a steady decline in the number of branches operating in the U.S. today.

Bank branches have been declining about 2% annually for several years now, while credit union branches are down only slightly. Due to the pandemic, I expect we’ll see a faster decline when the 2020 FDIC Share of Deposit data is released later this year.

But note this: Those low net rates of decline indicate branches aren’t going away anytime soon.

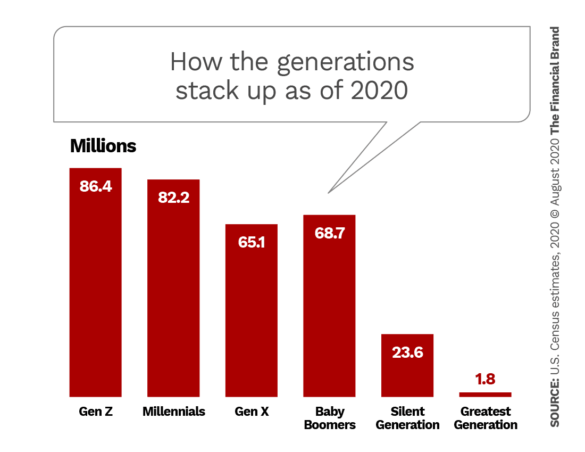

Millennials and Gen Z now represent the largest population blocks in the US, making up 51% of the total country. These two younger generations are the big drivers in digital usage. Many industry experts believe they will define the future of retail banking. It is their heavy usage of digital, especially mobile banking, that is driving boardroom discussions today.

Industry studies show that all generations use branches at some point at nearly the same percentages (70%-80%). The difference between generations is the frequency of usage.

Industry studies show that all generations use branches at some point at nearly the same percentages (70%-80%). The difference between generations is the frequency of usage.

Visiting a branch used to be a weekly occurrence — or bi-weekly (paychecks) — at worst. Recent research shows some new patterns. For example, 72% of Gen Z consumers visit a physical bank branch at least monthly, more frequently than any other age group, according to a 2019 consumer study by Adobe Analytics. And 60% of Millennials say the same. Surprisingly, older Americans were less likely to visit physical banks monthly, with Gen X (50%), Boomers (55%) and traditionalists (58%) saying they did so.

This doesn’t mean the older generations don’t go to branches, but with direct deposit, well-established accounts and generally more comfortable financial situations they don’t need to visit as often. I speculate that Gen Z visits more often because their financial resources are limited, and they are the least informed about how the industry works.

The online channel, which has been around for 20-plus years, has been adopted across all age ranges at about the same rate at this point. It’s actually become a mature channel. The newer mobile channel is still maturing with older generations who use it at much lower rates than younger generations, though COVID-19 has influenced this as well.

Because of these trends, the focus of branch transformation seems largely on the needs of Millennials and Gen Z. I can see why. They are the future.

Just one issue. They’re not where profits are found today for financial services providers.

Read More: The Future of ATMs in Banking

Balancing Present Profitability With Future Opportunity

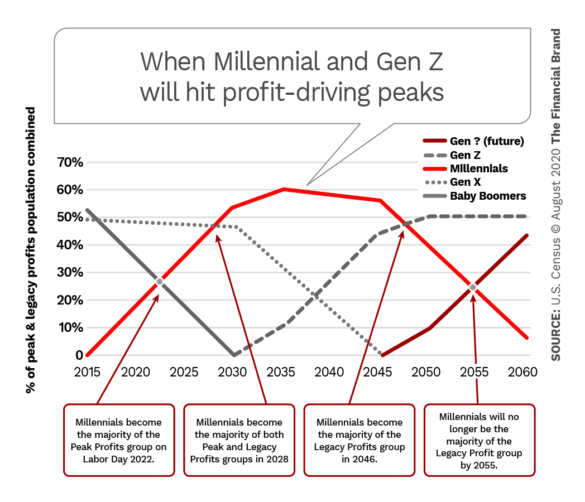

Millennials won’t begin hitting peak profitability until the 2030s, and the younger Gen Z, 20 years later — near 2050. This should prompt some questions:

• What are the risks of redefining your branch experience around groups that are years away from profitability?

• Are you willing to ignore, or at least deemphasize, the segments driving your profits today — Silent, Boomers and Gen X — in order to embrace the profit drivers of 2030-2070?

Read More: Why Universal Bankers are Now the Only Logical Option for Branches

Read More: Why Universal Bankers are Now the Only Logical Option for Branches

The challenge all financial institutions face in the next 10-20 years is how to design the next-generation branch that:

- Better integrates digital channels.

- Meets the needs of today’s customers.

- Can easily adapt to meet the needs of younger generations without completely rebuilding branches in the future.

This is easier said than done. Today, most financial institutions operate branches designed for the late 1970s. Institutions are only building about 1,000 new branches annually so the vast majority of bank branches are old.

Here’s a poser: The average bank branch is 43 years old.

The cost of a major remodeling can be nearly as much as building a new branch. So, what do you do today?

Focus on small wins. Focus on making digital channels work better with branches. “Connect” the channels by allowing branch staff to “see” what customers have been doing on the institution’s digital channel so they can reach out and offer help in completing the interaction or answering their questions.

Let’s get something straight here: Omnichannel isn’t about being able to do everything through every channel. It’s about being able to start an interaction in one channel and finish it in another.

The easiest analogy is shoppers browsing products online or even ordering online and picking up the purchase at their local store. Grocery stores have seen huge growth in this exact behavior during the pandemic.

Now is not the time to be closing all your branches, nor is it the time to stop investing in them. Now is the time to begin planning how you enable your branches to leverage the traffic in your digital channels.