At the same time that most traditional financial institutions are trying to rebuild legacy products for digital delivery, the biggest banking firms and non-financial companies are partnering to embed banking services in non-financial brand apps. This includes deposit services, payments, lending and other services that were only offered by banks and credit unions directly in the past.

The appeal of embedded banking is to provide an easy and seamless way to deposit, save, pay or borrow without leaving a non-financial company’s app. The result is the ability for non-financial firms to retain customers and increase the overall value of the relationship. According to McKinsey, “Companies of all types and levels of maturity – including retailers, telcos, big techs and software companies, car manufacturers, insurance providers, and logistics firms – are considering and preparing to launch embedded financial services to serve business and consumer segments.”

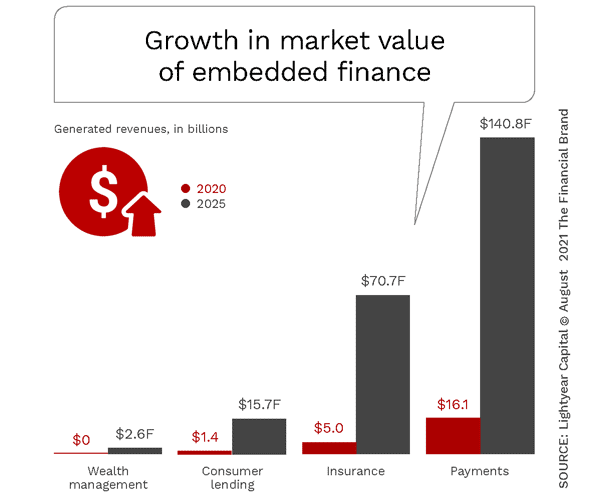

In response to the desire to embed finance within apps outside banking, leading financial institutions are working with fintech firms and non-financial companies to provide banking-as-a-service (BaaS) offerings. While some institutions see embedded finance as potentially threatening traditional banking models and control of current customer relationships, there is also the potential to participate in an estimated $230 billion market opportunity.

In the future, embedded finance will reposition financial institutions as software and product providers, often giving control of the customer relationship to consumer brands. According to a research report from Plaid and Accenture, there are four key ways embedded finance may change how financial and non-financial companies do business:

- Re-arrange relationships between financial providers and consumers with potential of shared relationships.

- Create new revenue streams for both banking organizations and non-financial firms.

- Reset competitive ecosystem, forcing companies to rethink existing business models.

- Build new partnerships between fintech and banking firms on behalf of non-financial brands.

What is Driving the Growth of Embedded Banking?

Embedding banking services within non-financial brand offerings is not new. From white-labeled airline credit cards to captive auto financing options to Amazon embedding payment options into their eCommerce app, non-financial brands have often provided access to banking products. What is different today is the scope of the offerings and the number of organizations that are expanding the integration of banking services within their apps.

The primary reason for this trend is that consumers want simple and seamless digital experiences that won’t require leaving their favorite app. They enjoy being able to pay for a ride within the Uber app, rent a vacation home without leaving the AirBnB app, and finance larger purchases without going to their bank or credit union. According to Ben Brown from Accenture, “Embedded finance is all about the contextual offering of financial services in a way that’s relevant to consumers and with an understanding of what their needs are. And that could apply to almost any or maybe literally any section of the financial services industry.”

Consumers Want Simplicity:

“Consumers want to stay within an app to research, engage, buy and share experiences.”

Beyond the impact of consumer behavior, non-financial institutions and fintech firms want to expand the penetration of financial services to increase average order size, expand engagement, improve customer satisfaction and increase loyalty. According to Accenture, 47% of U.S. businesses said that their companies are investing in, and plan to launch, embedded finance offerings in the near future. In fact, one of the fastest areas of embedded finance growth has been with buy now, pay later (BNPL) offerings.

Deeper penetration of financial services within non-financial brands is happening with Google, Apple, Walmart, PayPal and other brands that have no desire (right now) to ‘become a bank’, but want to deepen the relationship with existing customers by embedding financial services. Access to open banking APIs and new regulations are supporting this growth.

Finally, traditional financial institutions see an opportunity for new revenues with embedded finance. The ability to facilitate transactions that have a relatively low incremental cost, but significant scale is appealing.

Opportunities for Traditional Banking

For much of the past five years, the embedded banking movement has had mostly a negative impact on traditional financial institutions. As more consumers use payments, lending and banking services that are part of non-traditional banking apps, the traditional banking relationship had been increasingly fractured. More importantly, the details of each transaction reside with the non-financial (or fintech) brand and not with the legacy bank or credit union. This has a lasting impact on the ability to build a more robust dataset and relationship.

“Seventy to eighty percent of banks see embedded finance as a threat,” says Amit Mallick, Global Open Banking Lead at Accenture. “They are very worried that it will disintermediate them.”

But, the future of embedded finance can have positive implications. According to the research by Plaid and Accenture, “Embedded finance can not only provide access to new markets, it can also reduce customer acquisition and servicing costs. In addition, an underlying benefit of embedded finance is that it offers ways to monetize without charging customers more, and therefore enables companies to eliminate barriers to adoption of their core offerings.”

Open Banking Revenue Opportunity:

“The ability to leverage open APIs for expanded platforms increases revenue opportunities from outside the traditional financial ecosystem.”

In addition, financial institutions understand the intricacies of offering financial services, which gives them an essential role to play in the embedded finance trend. This includes an understanding of risk, compliance and regulations that most non-traditional providers and non-financial firms do not completely grasp. Banks and credit unions have also invested heavily in technology that may be prohibitive for non-bank entities.

“If an organization has the primary bank account for somebody, and that bank account is being connected to a lot of the financial and non-financial apps that exist across the ecosystem, the consumer is much more likely to continue using that organization as their primary bank account than if that’s not the case, stated Eric Sager, COO of Plaid in an exclusive interview on the Banking Transformed podcast.

In fact, the Accenture research found that for those already implementing embedded finance solutions, 70% said they are using partners, buying, or licensing technology as part of their embedded finance strategy. This illustrates the desire by non-financial firms to partner with legacy banking organizations.

Contextual Banking With the Bank

The ability to engage with banking services without going to a bank is what more and more consumers and businesses desire, especially for transactions. The pandemic made consumers aware of how digital engagement and new technologies can provide the right financial solution, on demand, integrated into non-financial applications. While most of these solutions are in the payments and lending space right now, they are rapidly expanding to improve overall consumer experiences.

“Across every segment there is a market transition — consumers want to do everything digitally,” says Sager from Plaid. “The toolkit to help brands be part of the next-generation changes is rapidly expanding.” Financial institutions must decide if they want to be a provider of financial services ‘in the background’ or whether they prefer to be the hub of both financial and non-financial services for their customers as well as the customers of varied services.

JPMorgan Chase CEO Jamie Dimon said his $3.4 trillion bank should be “scared s—less” about fintech and other digital-native companies expanding their market share. As organizations embark on their upcoming strategic planning journey, there needs to be an analysis of how embedded banking will fit into the future business model of the organization.