When people talk about the gender gap with respect to money, they are typically referring to the disparity between what men and women are paid for doing the same basic job. But there’s apparently another kind of gender gap — one related to household finances.

According to research from Regions Bank, women feel like managing the finances is their responsibility to shoulder, even though they express lower levels of financial confidence and optimism than men. The study examined how women approach money management, as well as how their financial knowledge and behaviors might differ from those of men.

44% of women said they are solely responsible for making financial decisions for their household, compared to 35% of men. However, men rated their overall confidence in handling finances higher (6.20 on a seven-point confidence scale) than women (only 5.86). Women under age 50 rated their confidence even lower (5.61).

The largest confidence gap between women and men is in the area of investing, where women respondents showed a confidence level of 4.75 on a seven-point scale compared to 5.42 for men.

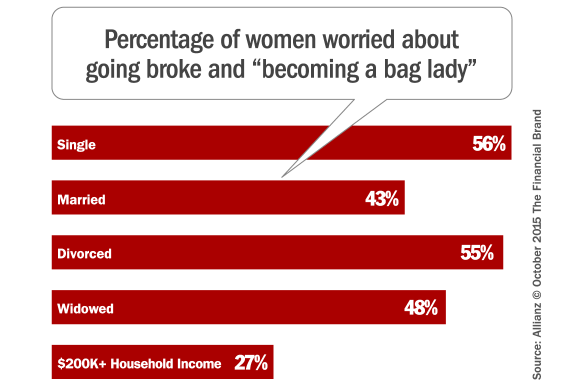

In another study from Allianz, 57% of women said the thought of running out of money in retirement keeps them awake at night — their biggest fear other than losing a spouse. Almost half of all women who responded said they “often” or “sometimes” fear losing all their money and becoming homeless. And this is not just found in lower income levels. Even 27% of the higher income-earners ($200,000+) said they worry about becoming broke and homeless.

“Studies show there is a confidence gap between men and women when it comes to financial matters,” said Anne Copeland, head of Private Wealth Management for Regions Bank. “As women continue to advance personally and professionally, women’s financial opportunities and responsibilities are actually outpacing their financial confidence and optimism.”

The Regions Women & Wealth Study also uncovered differences in how women and men gain confidence to make significant financial decisions, and where they seek financial advice and guidance. When asked to identify one or more resources and tools that helped them in making their last major financial decision, 56% of women identified a financial advisor while 56% of men cited prior education. Notably, 48% of women under age 50 identified their parents as a resource compared to only 30% of men under 50. Women also more frequently identified financial advisors and spouses as resources for making financial decisions. In contrast, men cited financial books, magazines and websites at higher rates than women.

Key Insight: Men prefer the DIY, self-taught method to gaining financial insight, whereas women seek input and counsel from others. Financial marketers should keep this in mind when structuring their financial education programs.

“Women are hungry for financial advice and guidance and are ‘crowdsourcing’ this information from a wide variety of trusted resources,” Copeland added. “There has historically been a lack of financial resources created with women in mind.”

“Women really like to learn,” Copeland said in an interview. “They want information. They want research. They want education. They don’t want to make a mistake. And at the same time, I think they’re pulled in many directions. They have lots of responsibilities in today’s environment.”

Men vs. Women: Two Different Views on Financial Matters

Regardless of gender, respondents clearly indicate the financial advice they would give their younger self would be to start younger and to save more (69%). Women were more likely than men to say they would “seek more advice from professionals” (38% vs. 30%).

The most common activities done by men and women to help improve their future financial security are to (1) review a retirement savings plan (71%) and (2) meet with a financial advisor (61%). Younger females are more likely than others to say they have done nothing in the past year to improve their future financial security (18%).

Just under two-thirds of respondents rate their confidence in their future financial well-being a six or seven on a seven-point scale (where seven is “Very confident”). The mean rating is 5.75. Females (5.62) are slightly less optimistic than males (5.83). And younger females (5.14) and divorced females (5.07) are even less optimistic.

Only one-third of respondents consider themselves financially “wealthy.” Females were less likely than males to think of themselves as wealthy (27% vs. 38%). And younger females were even less likely to say they’re wealthy (9%).

Two-thirds of respondents say a financial planner or advisor assists them in their investment or financial planning. This percentage grows to 72% for females. The next most frequent advisor is “Self” at 65%, and this drops to 54% for females. Married females are twice as likely as married males to seek advice from their spouse (65% vs. 32%). Younger females often look to their parents for advice (46%).

Nearly 60% of respondents would not accept a lower return on their investments to invest in companies that have social values consistent with their own. Females are more likely than males (47% vs. 38%) to say they would accept a lower ROI to invest in companies with social values consistent to their own. And this acceptance is even higher (51%) for younger females.

In terms of risk tolerance, respondents skew slightly toward being more conservative when making investment decisions for their retirement plans. Nearly half say they are “moderate,” 31% say they are “conservative” or “extremely conservative,” and 21% say they are “aggressive” or “extremely aggressive.” Females are more conservative than males (41% vs. 24%).

“The wealth gap is a much more meaningful gap both in terms of overall economic stability and how well women are able to provide for their own future and their family’s future,” said Mariko Chang, a former sociology professor at Harvard University and author of “Shortchanged: Why Women Have Less Wealth and What Can Be Done About It.”

Another survey from Blackrock encompassing 4,000 investors in the U.S. found that 53% of women had started saving for retirement, compared with 65% of men. And among those who had started saving money, women had accumulated less than half the amount men had: $34,900 vs. $76,800. The BlackRock survey also noted a divergence in savings behaviors. While 45 percent of men surveyed said they were willing to take on a high risk in order to achieve a good return on investment, just 28 percent of women felt the same.

[tfbpromo

The ‘Women & Wealth Initiative’

The study was commissioned in conjunction with the launch of the Regions Women & Wealth Initiative, a comprehensive effort to educate, equip and empower women financially.

As part of their Women & Wealth Initiative, Regions has introduced an enhanced online resource center with articles, videos and financial calculators developed specifically to meet the unique money-management needs and concerns of women. The bank says its website for women is consistently updated with fresh content.

Regions will also be expanding its Women & Wealth educational event series in 2016. These events are specifically geared for a female audience and provide information to Regions clients and community members on money management topics spanning everything from investing and the economy, to spending habits and retirement.

Regions says its Private Wealth Management division is focused on advising, training and engaging with women clients. Inasmuch, the bank has deliberately diversified its workforce, with the percentage of women who are private wealth advisors topping 40%.