For years, the banking community has built annual strategic plans by modifying plans made the previous year. No major changes – more iterations than complete rethinking of what needs to be done in the upcoming year. All of that changed as a result of the COVID-19 crisis.

COVID-19 has tested every component of the traditional banking business model. Employees were told to work from home, branches were closed, consumers lost their jobs, and new products and financial solutions were thrust upon the banking ecosystem. This challenged back office operating systems, credit risk models, mobile banking capacity and outdated security protocols. And instead of this change happening over a period of years, it happened overnight – literally.

Time to Hit The ‘Reset Button’

Now is the time to completely rethink how your organization creates a new path for the future. This will require new strategies, tactics and priorities that will support a new workplace environment, enhanced levels of consumer commitment, increased use of new technologies, a renewed commitment to innovation, and a sustainable value proposition that helps the community and the planet.

According to Bain, “Banks should plan for a turbulent period lasting months at least, with actions spanning their entire footprint — physical and virtual — and touching all stakeholders. At the same time, banks should stress-test their capabilities and financial metrics, in order to identify long-term strategic implications and opportunities, and build a bridge from the present crisis to a post-crisis future.”

If financial institutions miss the opportunity to completely reset their strategic plan during this crisis, trust from consumers, small businesses and the community could be at risk. The question becomes: What will it take to get beyond this crisis and be successful going forward? More importantly, what new assumptions and objectives must be put in place now that everything we had assumed only 4-6 months ago is no longer relevant?

Moving Beyond a Crisis Mentality

If not already the case, financial institutions need to move beyond crisis management. By its nature, this form of leadership and management is simply playing a game of catch up. While a pandemic with a complete global shutdown was not imagined in most business continuity plans, many of the components of what transpired when the banking system was forced to hit pause are now working rather smoothly.

The key now will be to move from crisis management to interim and long-term strategic planning knowing what we know today. In a McKinsey & Co. paper, they state that the key to resetting existing strategic plans is a focus on long-term employee wellness, delivering essential banking services to consumers and fulfilling social and financial wellness needs of the community.

Read More: When Opening Accounts in Branches Becomes Impossible

Future of Work Disrupted

Before the coronavirus pandemic, the major concern around the future of work at most banking organizations revolved around fulfilling unmet digital talent gaps, providing advanced workforce training, and encouraging professional development. Today, the immediate concern is around workplace safety.

Regardless of national and regional reopening agendas, financial institutions need to focus on reducing workplace risks for employees and other individuals who may enter a workplace. This is a highly involved process, with guidance coming from several different regulatory bodies. The process may take months beyond the time other businesses resume ‘normal’ activities.

One major benefit from the COVID-19 crisis is that financial institutions were able to determine which functions of their organization can be done well in a remote work scenario. All financial institutions should review policies, practices, and performance metrics that were in place prior to the health crisis and adjust them for the new working environment.

If data security, fraud, cybersecurity, and privacy concerns can be addressed, many organizations may move entire departments to a work-from-home future. For instance, some organizations have already announced that their primary call centers will be remotely based in the future.

Customer Experience Redefined

Financial institutions have long professed a commitment to improved customer experiences. In fact, in the 2020 Retail Banking Trends and Priorities report published by the Digital Banking Report, ‘improving the customer experience’ was the top ranked priority for the seventh straight year.

Many financial institutions relied on face-to-face interactions to improve their consumer satisfaction ratings. At the same time, many financial institutions were investing in improving their digital banking offerings. But, despite this focus, many organizations found themselves completely unprepared for a world with only limited branch access.

In some cases, banks or credit unions could no longer open new accounts or complete loan applications without branch engagement. Many organizations were also unable to personalize important communication when consumers needed timely and specific engagement the most. Most organizations were also unprepared when the government wanted the industry to be the conduit for small business relief loans.

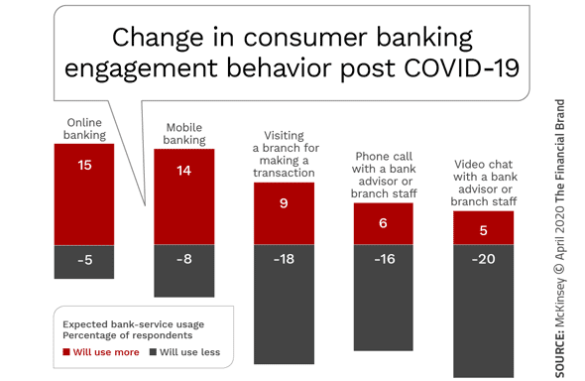

COVID-19 completely redefined the parameters of a positive consumer experience. The simplicity of digital engagement, the intuitive nature of mobile banking and the real-time access to relationship insights are front and center. In addition, real-time personalized solutions that reinforce financial wellness are now considered a requirement for a lasting relationship.

Now more than ever, human outreach, combined with a strong digital platform user experience are basic necessities. Consumers need to know that their financial institution knows them, understands them and empathizes with them at this time of need.

In the post COVID-19 world, financial education will be desired more than ever as will insights into how to take best advantage of digital options. According to McKinsey, “To encourage customers to use existing remote channels and digital products, institutions can launch positive and safety-oriented messaging aimed at reducing reliance on branches for services that are digitally available — while also providing tutorials online and by phone and increasing remote support options.”

Finally, we are already experiencing an increase in new savings account openings. This is a response to the realization that few consumers had adequate savings available for a crisis where employment is interrupted. Financial institutions must create new services that can help consumers along their path to financial security.

Economic Support for Consumers and Communities

The COVID-19 crisis took a significant toll on the physical and emotional health of consumers, small businesses and entire industries. Many will take years to recover and will need the support of government and outside organizations to survive. Financial institutions worldwide are at the center of the recovery efforts.

Beyond being the distribution point for government loans or the check cashing point for relief check recipients, financial institutions will be asked to help people and organizations recover through grants and loans. But,as Citigroup CEO Mike Corbat recently noted, “Banks walk a fine line between supporting customers through the crisis and loading them with loans they will not be able to repay.” That could threaten the solvency of a bank and the broader financial system.

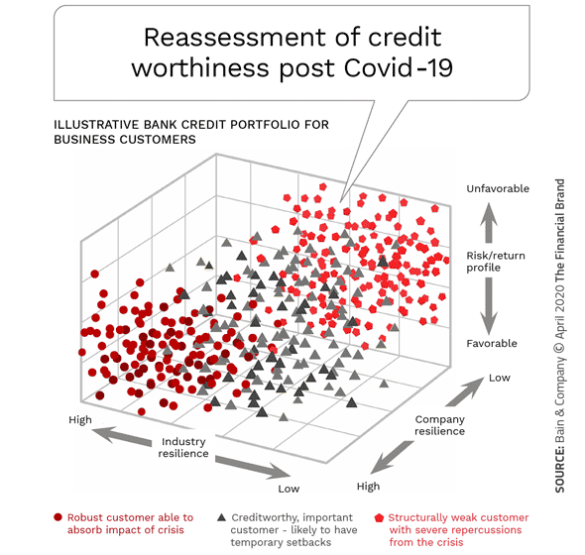

According to Bain, the key to being able to provide credit will be to reassess the way credit worthiness is evaluated, beyond traditional credit scores, to include the ability to absorb the impact of the crisis. This analysis needs to be overlaid against the financial condition of the bank or credit union itself.

A similar analysis must be conducted as it relates to the support of communities post COVID-19. There will be no shortage of need in most communities. The objective will be to allocate any available funding to those initiatives that can be parlayed into even greater synergistic wins in the community.

Building a Revised Strategic Plan

When we review the retail banking trends over the past several years, it appears that most of the aforementioned trends remain intact. The change to strategic plans will most likely be in the resource commitment and prioritization of trends that were previously set in motion.

The impact on the strategic plan of banks and credit unions will most likely be correlated to the extent and duration of the COVID-19 crisis. The movement to remote work, the commitment to retraining for digital needs, and the focus on the well being of employees will take a higher prominence as the crisis lingers. “As the workforce settles into their new routines over the next weeks or months, banks should consider this as a testing ground for what does and does not work and draw implications for their HR, organizational, governance and culture transformations,” stated McKinsey.

The same is true with regard to consumer behavior with digital products and engagement. The longer the crisis, the more likely the ‘move to digital’ will become permanent. According to McKinsey, “It should be expected that customer routines and expectations will shift further in meaningful proportions, both in terms of digital adaptation and the expectation for proactive communication and care.”