With unemployment in the U.S. reaching near historic lows, financial institutions are struggling to fill critical positions essential to their digital transformation strategies. Demand for talent now outstrips supply when it comes to openings in several key roles, from data analytics and user experience (UX) design, to artificial intelligence (AI) and software engineers. Sure, there may be lots of IT talent out there, but those people aren’t lining to take a job at your local bank or community credit union. They are knocking on doors at Google and Amazon — hot companies with deep wallets.

Indeed a study by Capgemini found that 62% of senior leaders in the banking industry believe the digital talent gap has been widening in the past couple of years. That’s more than any other industry surveyed — retail, auto, utilities, even insurance.

So the question is, how can today’s banking provider compete? How do they convince IT professionals to work for in the financial industry… for less pay and fewer perks like “Free Beer Fridays”, ping pong tables and in-house “massage technicians”?

“This isn’t just a human resources issue,” says Capgemini about the staffing challenges facing retail financial institutions in the Digital Age. “It’s an organization-wide phenomenon affecting all areas of the business.”

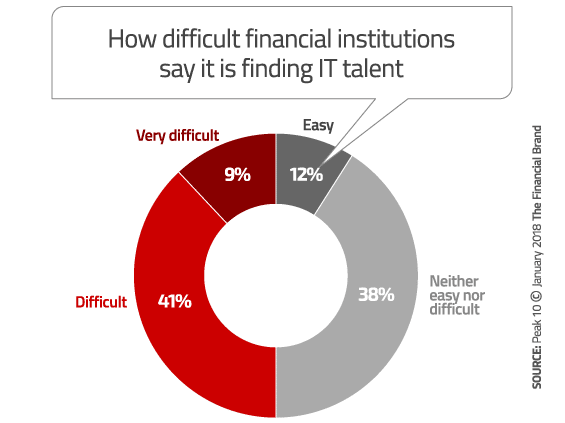

Banks and credit unions desperately need IT talent, and a lot of it. More than three-quarters (76%) of financial institutions report that they have created new IT roles in the last two years, but they are having a hard time finding the IT talent they need. Half of all financial institutions say that hiring IT staff is either “difficult” or “very difficult.”

In an informal poll of HR executives working in the financial services industry, Cornerstone partner Terrance Roche found that two biggest areas of need for talent were business lending experts and IT professionals, particularly those specializing in data management and business intelligence.

An Ugly Reality

Why would a smart, well-educated college grad with a degree in software engineering, computer programing or IT management want to work in banking? It’s a tough question for an industry with a reputation that’s less than stellar. There’s the financial crisis that vilified financial institutions. Movies like Wall Street and The Wolf of Wall Street depict the rampant fraud and boorish behavior. There’s the subprime lending crisis that brought the world’s economy to its knees. And more recently the Wells Fargo account fraud scandal.

In 2011, 27% of Columbia University MBA graduates went into banking. By 2016, that percentage had fallen to 14% — half the number seen only five years earlier. Compare that the number of MBA graduates choosing technology careers in Silicon Valley. In 2013, 13% of MBA graduates had accepted a job in the tech sector. In 2016, 33% took a job at a technology firm.

Banks and credit unions are not known as hotbeds of technology or innovation incubators. Other industries (any industry!) are seen as more technologically savvy and therefore more attractive to job seekers. The jobs may not be more interesting, but the employers are. And it is these industries that are absorbing all the IT talent that banking providers need.

Making matters worse, few banks or credit unions can afford to pay the salaries that qualified IT staff command. According to Glassdoor, the average salary for a data scientist is $128,549 a year. Even an entry level data scientist makes a hefty $118,748. But if they go to work for a tech giant like Google, Amazon or Airbnb, they can expect to earn much more.

Quinlan & Associates says the problem isn’t just about attracting young graduates into banking, but also retaining existing employees and stopping what Quinlan & Associates calls a “hollowing out of financial institutions and a critical shortage of executive leadership.” If finding good help wasn’t hard enough, financial institutions now have to worry about a talent exodus, compounding the headache. As IT professionals flee the financial industry, HR directors are left struggling to fill even more positions.

Capgemini asked employers which digital roles they will need to fill in the next two to three years. The top ten are:

- Information security/privacy consultant

- Chief Digital Officer/Chief Digital Information Officer

- Data architect

- Digital project manager

- Data engineer

- Chief customer officer

- Personal web manager

- Chief internet of things officer

- Data scientist

- Chief Analytics Officer/Chief Data Officer

There are the hard digital skills that everyone thinks of such as data analytics and programming. But then there are also soft skills that banks and credit unions will need as they continue their march toward digital transformation.

Think about it… Most people have — at some point in their life — had the misfortune of having to interact with that crabby, cantankerous, irascible tech guy. You know the one. You cringe when you ask him a question about anything. He sighs and gripes. He will rant about the most obscure aspects of IT infrastructure (e.g., “Ruby on Rails is yesterday’s joke”). As financial institutions try to navigate the delicate digital path forward, the last thing they need is an army of tech divas marching around making life more difficult. Banks and credit unions need people with both the tech chops and the people skills that it takes to be an effective manager.

Cultivate IT Talent From Within

Few financial institutions are aggressively, proactively training current staffers in the areas that matter most, such as machine learning, data analytics and business intelligence. This is a big mistake, according to Roche at Cornerstone. He says banking providers shouldn’t even try to compete with the likes of Google and Amazon for talent. Instead, banks and credit unions should cultivate talent from within.

Now you may be thinking, “We already send employees to training programs.” You may be even sending them to hone their skills in something specific to their role, such as database management. But in the financial industry, more than half of those in tech roles say that their organization’s training programs aren’t helpful. They also say they are not given the time off to attend classes. In a Capgemini study, 45% describe their company’s training program as downright “useless and boring.”

But according to Roche, financial institutions need to change this. They should pull smart, ambitious employees who are interested in pursuing an IT career from other areas of the organization and get them into a formal training and certification program. The rationale? It’s easier to teach someone the tech skills they need than it is to find someone willing to work in banking. If you can convince someone to work in the financial industry, the hard part is over.

Capgemini also has some similar suggestions to get, develop and retain IT professionals:

- Think laterally and get creative. It’s tough to compete against Google and Amazon for top IT talent since you won’t be able to match the salaries that these tech giants can afford to pay. Diversify your recruiting approach and look for smart people coming out of non-IT focused programs who you can train in data analytics, business intelligence, and other skills.

- Prioritize learning. More than half of IT talent say they will jump ship to an organization that offers better digital skill development. Don’t just give lip service to training but create an environment in which learning and training is a priority. Reward employees for completing training.

- Get leadership to take a talent strategy seriously. Remember, this is not an HR issue but a strategic issue that affects the entire bank or credit union and its ability to achieve its digital transformation strategy.

One Bank’s Novel Recruitment Perk

A short drive from Silicon Valley, First Republic Bank in San Francisco knows all too well how difficult it can be to attract young IT talent Millennials. They also recognize that many of these new graduates are saddled with student loan debt. These young employees aren’t thinking about retirement, so they don’t place as much value on benefits like a 401(k) savings plan. They are more concerned with how they are going to pay back tens of thousands of dollars in debt

First Republic decided to add student loan repayment as a benefit to all full-time or part-time employees. The program, which is also available to First Republic employees who have taken out education loans on behalf of their children, offers:

- $100 per month of loan repayment during the first year of enrollment in the benefit

- $150 per month of loan repayment during the second year of enrollment in the benefit

- $200 per month of loan repayment thereafter while enrolled in the benefit until the debt is repaid

it may not seem like a lot of money and it doesn’t cost the bank much, but First Republic believes that the promise of whittling away at student loans makes the bank more attractive for recent grads who would have taken jobs elsewhere in the region that they serve — Cupertino, San Jose, Mountain View and Palo Alto.