Early in 2013, Credit Union Central of Canada published its annual report on the health of the country’s credit union system. While the organization understandably tried to put a happy face on the data, much of the information contained in the study paints a less rosy picture.

There are many similarities in the ways that Canadian and U.S. credit union systems have evolved, and the issues they now face: member growth, an aging membership, loss of special tax status… and big credit unions get bigger while small ones struggle for survival. But the impact of these issues seems to be more pronounced in Canadian credit unions.

Should credit unions in the U.S. interpret the turmoil in the Canadian credit union industry as an accelerated and exaggerated prophecy for rough times ahead? Is Canada foreshadowing the future for American credit unions?

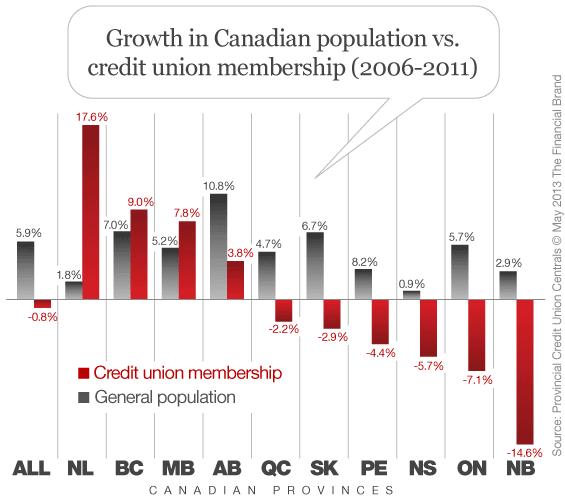

Population Growing Faster Than Membership

According to census data, Canada’s population grew by 5.9% between 2006 to 2011. During the same period, the combined credit union/caisse populaire (Desjardins) system recorded a 0.8% decline (85,700) in membership between. When the Quebec and the Desjardins system are excluded, membership in credit unions in the rest of Canada increased by 2.8%.

Alberta, Manitoba, British Columbia and Newfoundland & Labrador were the only provinces reporting gains in membership between 2006 to 2011. The remaining provinces all experienced a decline in membership during that period.

Read More: U.S. Credit Union Industry Outlook: 5 Years Back, 20 Years Forward

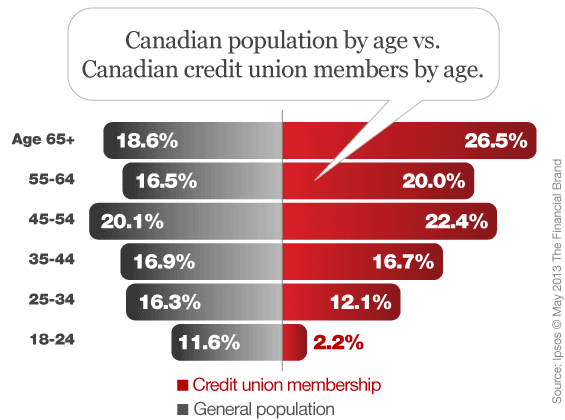

Credit Unions Can’t Survive With Only Older Members

The report found that credit union members tend to be older than the general population. In 2011, 26.5% of credit union members were seniors, compared to 18.6% of Canada’s adult populace.

At the opposite end of the spectrum, census data show that 27.9% of Canadians were 18 to 34 years old in 2011 compared with only 14.3% of credit union members in 2012. More specifically, while 11.6% of the overall population was between 18 and 24 years of age, only 2.2% of credit union members were in this age group.

Surprisingly, a separate study revealed that about two-thirds of Canadian credit union members were women, when the Canadian population is generally evenly split between males and females. Credit union members also have more money and more education than the average Canadian.

In the U.S., the average age of a credit union member is 47 — nearly 10 years older than the median age of the U.S. population. Back in 1989 it was 42.8 and in 2000 it was 44. Today over 27% of the US population is under 20.

Read More: How Much Do Credit Union Marketing Executives Make?

Kiss That Tax Exemption Goodbye

The Canadian government made the surprise announcement in March that a tax deduction extended to credit unions would be phased out over the next five years beginning in 2013.

This caught credit unions completely off guard.

“We were surprised that Budget 2013 targets credit unions in this way,” said Gary Rogers, VP of financial policy with Credit Union Central of Canada, said in a statement.

The deduction has been in place for 40 years. It will decrease by 20% starting in 2013, until it is eliminated in 2017, sticking credit unions with a higher tax bill.

Credit unions across the country expressed outrage at the proposal. Some argue that the government’s decision comes at a critical time in the country’s ongoing economic recovery. And for smaller credit unions the timing couldn’t be worse; the increase in their tax rate comes at the same time when operating margins are being squeezed as regulators are looking for increase capital to be held. Canadian regulators were likely aware of this before making their announcement, so protests probably aren’t going to phase them much if any. Hey, if they think they need the money, what can credit unions do about it?

According to the budget record, the tax break costs the government an estimated $47 million in 2012, although that amount has been declining over the years.

Read More: 5 Things You Should Know About Credit Union Marketing Budgets

Assets Grow, While the Number of Credit Unions Dwindles

From 1992 to 2011, the number of credit unions fell by 726, or at an average annual loss of about 36 credit unions (or roughly 3.6%). System assets on the other hand nearly quadrupled during this period, with an average increase of approximately $5.2 billion per year.

Canadian credit unions’ share of domestic assets fell from 4.8% in 2004 to 4.5% in 2011. Share of the personal loan market dropped from 3.8% to 2.5%. Credit unions lost 1% of the market in both small business and agricultural loans.

| 1992 | 2002 | 2011 | |

|---|---|---|---|

| Number of credit unions | 1,094 | 632 | 368 |

| Number of locations | 1,947 | 1,806 | 1,733 |

| Assets ($MM) | $35,468 | $66,423 | $140,219 |

| Average assets per credit union ($MM) | $32.40 | $105.10 | $381.0 |

| Average members per credit union | 3,680 | 7,281 | 13,947 |

| Top 100 as % of total assets | 62.0% | 70.5% | 84.4% |

| Top 10 as % of Total Assets | 25% | 33% | 45% |

It’s the same story in the U.S.: the big are getting bigger, while small credit unions wither and die. The top 100 U.S. credit unions (ranked by assets) added 1.3 million new members in 2012, accounting for 84.4% of all new members gained by the entire industry. In 2011, the top 100 U.S. credit unions grew by 1.2 million members while the rest of the industry shed a collective 118,287 members. Similarly in 2010, the top 100 credit unions grew by 1.6 million members and the remaining 7,610 lost 286,419 members. Membership gains from the top 100 credit unions are generally offset by the collective membership losses realized by the rest.

In the U.S., Almost all the gains made by credit unions — in terms of assets, members and branches — come from a handful of the industry’s largest institutions. While the top 100 only represent 1.4% of all credit unions, they contribute half of the industry’s asset growth and about 90%+ of the industry’s member growth.

The Financial Brand has forecast that the number of credit unions in the U.S. could drop below 4,000 twenty years from now, if the current rate of decline continues.

Read More: Do Credit Unions Enjoy an Unfair Advantage in Their War with Banks?

Have the Number of Credit Union Branches Peaked?

The number of branch locations collectively operated by Canadian credit unions fell by 214 over this 20 year period, although most of this decline took place in the late 80s and mid 90s. Since then, Canadian credit unions have often acquired branches discarded by the banks. In just two years, credit unions purchased a total of 72 bank branches.

The number of branches operated by all credit unions totaled 20,694 in 2007. By 2011, that number climbed to 21,433, a slight increase of only 739 branches. However in 2012, the number of credit union branches declined for the first time in the industry’s 100+ year history — 27 fewer than the year before.