“We’ve just compressed years of change into weeks” perfectly captures the shift within banking as March turned into April and then May. Mobile and online banking sign-ons rose to an all-time high, banking employees were forced to go remote and many branches closed. Contact centers were flooded with calls as banking customers navigated not only normal banking scenarios, but also the unknowns that the stimulus program, Payroll Protection Program, market uncertainty and first-time technology usage brought.

The industry has long discussed the impact the digital shift would have on banking. How would the role of the branch and contact center evolve as customers’ digital banking behaviors changed? Terms like “digital transformation,” “open banking,” “AI,” and, “personalization” have all been positioned as the silver bullet that will propel the digital shift. But no one could have properly predicted how quickly that change would be forced upon us.

As financial institutions scramble to evaluate their digital experiences, one of the top questions that needs asking is: “Are we creating digital friction and what impact is that having on customer experience?”

What is Digital Friction?

One of the top challenges facing banks and credit unions is the number of channels they need to support. Banking customers have, at a minimum, six ways to interact with financial institutions — branches, contact centers, ATMs/ITMs, website, mobile banking and online banking.

Brands like Amazon and Netflix have trained consumers to expect that we should be able to come and go into any channel and expect a similar experience (while they really only have to support their web and mobile platforms). They have mastered the self-service game as their whole businesses are built on digital self-service. As the shift in digital banking continues to accelerate, there are three questions financial institutions need to ask. Are we…

- Providing self-service support and service options that provide speed and convenience?

- Eliminating speed bumps and accelerating the path to self resolution?

- Delivering this same experience and access to information across all of our channels?

There are hundreds of typical banking inquiries that happen daily covering topics ranging from bill pay transactions to simple FAQs about a routing number to technology (e.g. reset password) to lending options to such high-emotion, immediate needs as fraud.

For the sake of illustration, let’s choose the subject of “overdraft.” Our data shows this has been a top-ten query since the onset of the coronavirus pandemic. Here are three different examples of what digital friction looks like for three banking customers:

- Jeanne starts on the website. The main navigation shows no page for overdraft, so she clicks on the support page. The support page provides some high-level FAQs that don’t address overdraft. It also details the different ways that customers can contact the financial institution. She uses the search bar and finds a routine answer that outlines the overdraft fee schedule, but provides no other context. She is forced to call to get the answer to a relatively simple question.

- Bob starts by logging in to online banking. Online banking provides support, but the support information is only focused on online banking questions (common, how-to technology questions). It, too, outlines the different ways that customers can contact the financial institution. He is forced to go back to the website or call to get any additional support.

- Michelle starts in mobile banking. An avid mobile banking user, she is comfortable with all of the features within mobile banking. However, this time she has a question about overdrafts. Her only option for any non-mobile banking information or support are the different ways that customers can contact the financial institution. She, too, is forced to look on the website or call to get any additional support.

While this specific scenario might seem relatively mundane, it outlines the siloed approach the industry has taken. Financial institutions expect customers to do certain things in certain channels and have not properly considered that for those customers, that channel is their main “branch.”

Yes, customers expect to be able to do banking transactions, but they also expect to be able to get support, service and product information, or at least the right links to where that information lives.

“Are you providing easy-to-find-and-follow information across all of your digital channels, or are you creating digital friction?”

The true impact of digital friction is felt when you compound this one example across the hundreds or thousands of routine scenarios happening every day — especially in the last few months — with questions about technology, online account opening, rates, lending products, and even the good old routing number.

Are you providing easy-to-find-and-follow information across all of your digital channels, or are you creating digital friction? What impact is this having on your customer experience, on your call volumes, technology adoption and conversion rates?

Removing Digital Friction

As the banking industry continues to outline, build and deploy the underlying technology solutions required to make digital transformation a reality, here are four considerations for removing digital friction.

1. Breaking down internal silos by putting the focus on the customer experience. One of the top challenges we hear focuses on internal ownership and the silos it creates. Digital channels are “owned” by different departments — e.g. Marketing owns the website, IT owns mobile banking and Retail Operations owns online banking. There is little to zero collaboration on how the channels can work better together. Until these silos begin to fall and the customer experience is the primary focus, you will never be able to remove the digital friction to deliver a consistent digital experience.

2. Providing navigational beacons to make information easy to find. Delivering a frictionless experience means surrounding your customers with multiple ways to find information across all of your digital channels.

- Navigation. Providing clear and intuitive titles accessible from your website, mobile and online banking.

- Search functionality. Allowing your customers to search for answers not just from your website, but from mobile and online banking channels.

- Banking chatbots. AI powered banking chatbots can be easily deployed across multiple channels and act as navigational beacons that can deliver the right answer at the right time.

- Contextual FAQ widgets. Providing the right supporting content at the right time.

3. Delivering contextual guidance to anticipate the customer’s next step. A frictionless experience also means providing the contextual guidance to anticipate what the customer is looking to do and providing the ability to do so quickly and conveniently. This, along with following the navigational beacons, is how financial institutions can truly deliver a better experience while increasing technology adoption, increasing conversion rates and lowering contact center inquiries. Some specific suggestions to accomplish this:

- Actionable next steps. The majority of financial institutions answer the consumer’s question, but overlook the next step. From basic links, to common actions (e.g. schedule an appointment, apply online, watch a tutorial), remove the friction by anticipating what the true intent is behind the question and serving up the next step clearly.

- Digital how-to tutorials. Driving more technology adoption and usage requires education. Digital how-to tutorials provide not only a great tool for your customers as they are navigating new and existing features, they also provide a great onboarding experience.

- Delivering contextual support. As your customers are in the research, consideration or completion phase, serve up contextual support. As they apply online, serve them contextual FAQs that anticipate common questions that lead to frustration and abandonment.

4. Leveraging mobile and online banking to provide the full branch experience. Delivering a consistent experience and equal access to information across all of your channels (including mobile and online banking) must be a priority. The majority of modern, digital banking platforms allow for additional content, links and chatbots. Take advantage of these features to provide access to information. To start, they can simply link directly back to your website as you build out contextual options that deliver the same access to information across all of your digital channels.

Final Considerations for Removing Digital Friction and Providing the Digital Experience Customers Demand

- Content. Is your content providing good answers and the next steps that accelerate the path to self resolution?

- Artificial intelligence. Is your search and chatbot powered by banking AI that truly understands what the customer is asking for and what their intent is?

- Contextual FAQs. Are you tagging and categorizing your content so that relevant FAQs appear (think back to the overdraft example and the number of questions from that one simple topic).

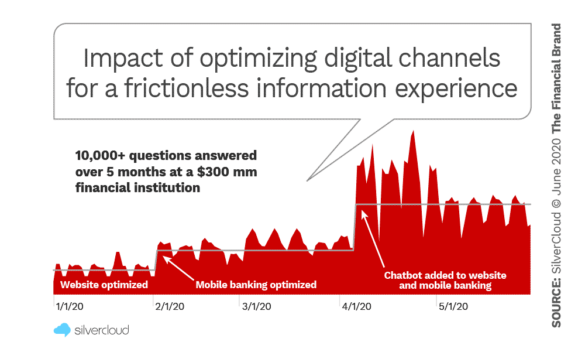

The chart below presents an example of the impact that following the best practices outlined above can have for any financial institution. Specifically, the more options customers are given to easily find information, the more usage increases.

With the massive investments that have already been made in technology to make digital banking transactions a reality, now is the time for financial institutions to evaluate the consequences of digital friction, and to bring in the service and support aspect for a complete 360-degree digital banking experience.